TL;DR

For U.S. merchants processing $25K to $5M monthly, Stripe Radar leads AI fraud detection in 2026 on training data scale and per-screen pricing transparency. Worldpay FraudSight wins above $2M monthly card-not-present, where dedicated risk analysts and FIS-network training matter. PayPal Fraud Protection Advanced fits marketplaces with concentrated chargeback exposure on PayPal-funded volume. Square and Clover suit in-person retail. Helcim, Stax, and Payment Depot rely on gateway rules and 3DS rather than merchant-tunable machine learning.

How we ranked

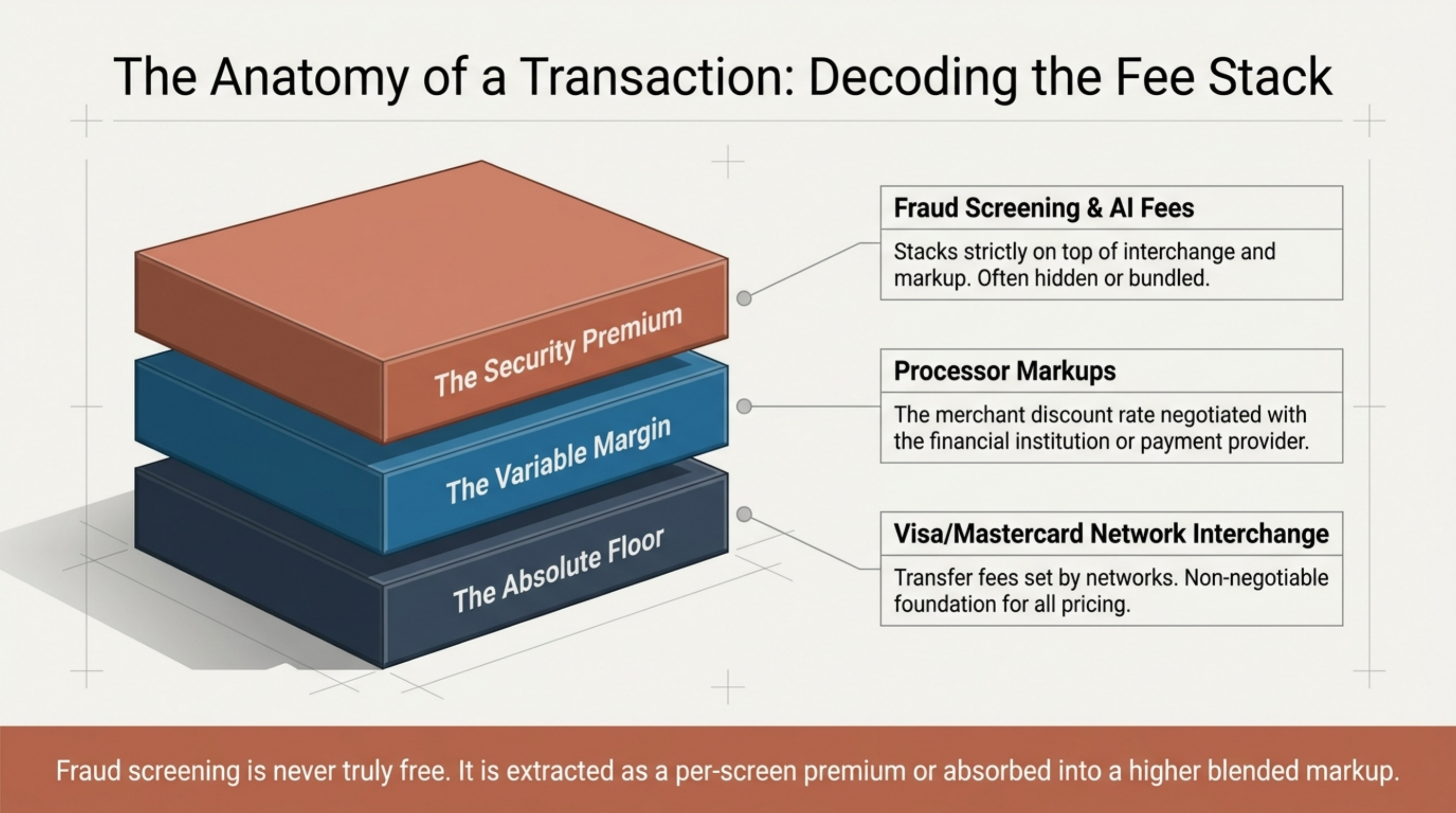

We weighed five criteria, each scored against published documentation. First, per-transaction screening cost: free, bundled, or per-screen. Second, training data scale: how many transactions the model has seen, drawn from processor disclosures. Third, rule customization: whether a merchant can write conditions, set thresholds, and review flagged orders. Fourth, chargeback handling: explicit liability shift on covered disputes versus general dispute support. Fifth, integration depth: native checkout, hosted fields, 3DS handoff, and refund automation. We used Visa and Mastercard interchange schedules as the cost floor since fraud fees stack on top of network rates, per the Visa Interchange Reimbursement Fees and Mastercard Interchange schedules. Federal Reserve payments data, available at federalreserve.gov, was used to size the card-not-present share of U.S. merchant volume.

At a glance

Pricing is taken from each provider's public pricing page or product page as of June 2026. Custom-priced products show the published list price or contact-sales note.

| Provider | Fraud tool | Pricing | Tunable rules | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | Radar / Radar for Fraud Teams | Free / $0.07 per screen | Yes, with backtest | $25K to $2M CNP | Stripe Payments lock-in |

| Worldpay | FraudSight | Custom, contact sales | Yes plus managed review | $2M+ CNP | 7 to 14 day setup |

| PayPal | Fraud Protection Advanced | Add-on per transaction | Yes | Marketplaces, digital goods | 3.49% + $0.49 standard rate |

| Square | Built-in screening | Bundled in rate | Limited | Retail, food service | Outgrown above $200K CNP |

| Clover | Built-in screening | Bundled in plan | Limited | Single-location retail | Hardware lock-in |

| Helcim | Gateway rules | Bundled in IC+ rate | Yes, basic | $100K to $1M moderate fraud | No proprietary ML model |

| Stax / Payment Depot | Gateway rules | Bundled in membership | Yes, gateway-level | Stable B2B and services | No dedicated fraud tier |

Stripe Radar

Stripe bundles Radar into its 2.9 percent plus $0.30 online card rate at no extra fee. Radar for Fraud Teams adds $0.07 per screened transaction on top of standard processing, per the Stripe pricing page. The model is trained on transactions across the Stripe network, which gives the highest training data scale among the providers compared here. Merchants get device fingerprinting, custom rule chains, manual review queues, and Stripe Chargeback Protection at 0.4 percent of the transaction on eligible card-not-present sales.

Custom rules can block, allow, or send to review using order amount, card BIN, device, IP, email age, and prior dispute history. Operators can backtest a rule against the previous 90 days before deployment, which limits false positives at launch.

Stripe Radar fits any merchant already on Stripe Payments who processes more than $25K monthly card-not-present. It is the most direct path for SaaS, e-commerce, and platform marketplaces. It does not fit merchants on legacy MIDs with a different acquirer.

Worldpay FraudSight

Worldpay sells FraudSight as a separate product layered on its acquiring service. Pricing is custom and tied to monthly volume since Worldpay does not publish a flat rate, per its public site. The model is trained on FIS network volume and integrates with Worldpay's gateway plus third-party gateways through API.

FraudSight scores each transaction in real time and supports rule chaining, device intelligence, and behavioral biometrics. Merchants can buy a managed services option where Worldpay risk analysts review flagged orders, useful for teams without a dedicated fraud headcount.

The fit is enterprise card-not-present above $2M monthly. Below $500K monthly, Worldpay is generally not worth the contract complexity. The Nilson Report consistently ranks Worldpay among the top U.S. acquirers by purchase volume, which gives the FraudSight model wide exposure to U.S. card-not-present patterns.

PayPal Fraud Protection

PayPal offers Fraud Protection Advanced as an add-on to Standard or Advanced checkout. PayPal also includes Seller Protection on eligible PayPal-funded transactions, which shifts chargeback liability for covered cases on items shipped with valid tracking, per the PayPal business fees page. Standard PayPal checkout starts at 3.49 percent plus $0.49 for digital wallet acceptance.

Fraud Protection Advanced layers a rules engine on PayPal Checkout. Merchants can score transactions, flag patterns by velocity or BIN, and route high-risk orders to manual review. Pricing is published per transaction on top of standard processing.

PayPal fits marketplaces and digital goods merchants with concentrated chargeback exposure on PayPal-funded volume. The trade-off is total cost. At $300K monthly, the 3.49 percent plus $0.49 standard rate runs well above interchange-plus options, so PayPal works best as a checkout option alongside another acquirer, not as the sole processor. Merchants that need card-present coverage should pair it with a separate POS.

Square

Square bundles fraud screening into its standard processing rates. In-person card is 2.6 percent plus $0.10, online is 2.9 percent plus $0.30, and keyed is 3.5 percent plus $0.15, per the Square pricing page. Square uses internal rules and machine learning across its merchant network to flag card-not-present transactions. Disputes are managed inside the Square dashboard with templated evidence submission.

Square does not publish a per-screen fee since screening is part of the underlying rate. There is no separate fraud SKU to enable. Rule customization is limited compared with Stripe Radar for Fraud Teams: merchants can adjust some thresholds inside the dashboard but cannot write the same depth of custom rule chains.

Square fits in-person retail, food service, and small online sellers. Its model is trained on small-business volume, which differs from Stripe's e-commerce and SaaS skew. Merchants with card-not-present volume above $200K monthly will outgrow Square's blended rate and should look at interchange-plus paired with a dedicated fraud tool. For pop-up retail and single-location food, the bundled approach saves the cost of a separate subscription.

Clover

Clover, owned by Fiserv, bundles fraud screening into its plan-based POS. Plans run $14.95 to $54.95 per month with card-present rates of 2.3 to 2.6 percent plus $0.10 and keyed at 3.5 percent plus $0.10, per Clover's published pricing. Fraud screening for card-present transactions is rule-based with EMV chip and PIN as the primary defense and the related liability shift on covered chargebacks.

For Clover Online, fraud screening sits on the Fiserv gateway. Clover does not break out a separate fraud product or per-screen fee. Hardware lock-in is the operational constraint: Clover terminals are bound to the merchant agreement and resale value is limited because of restrictions on reflashing the devices.

Clover fits merchants who want one vendor for POS, payments, and light fraud screening for in-person volume up to roughly $500K monthly. Card-not-present heavy merchants and platforms should look elsewhere. Clover's fraud feature set is positioned for retail and food service operators who are not running a separate risk function.

Helcim

Helcim uses interchange-plus pricing at IC plus 0.50 percent plus $0.25 online and IC plus 0.40 percent plus $0.08 in-person, per its pricing page. Fraud screening relies on standard AVS, CVV, 3DS 2.x routing, and Helcim's gateway rules. Helcim does not publish a dedicated AI fraud product, and there is no per-screen fee.

Merchants can configure velocity rules, IP blocks, and country restrictions inside the Helcim dashboard. Manual review queues exist for flagged transactions. For card-present volume, the standard EMV liability shift applies. Automatic volume discounts apply at higher tiers, which keeps the effective rate predictable.

Helcim fits merchants who want interchange-plus pricing with built-in screening for predictable card mixes. At $100K to $1M monthly, the absence of a per-screen fee can save 0.10 to 0.20 percent versus stacking Radar for Fraud Teams on top of an interchange-plus quote elsewhere. The trade-off is sophistication: Helcim's rules engine is not the same as a network-trained ML model. For high-fraud verticals such as digital goods or travel, that gap matters.

Stax and Payment Depot

Stax charges $99 per month plus interchange plus $0.08 in-person and $0.18 online, per staxpayments.com. Payment Depot runs a similar $79 to $199 per month wholesale model with $0.05 to $0.15 per transaction, per paymentdepot.com. Neither markets a proprietary AI fraud product.

Both rely on the underlying gateway tools for fraud screening: AVS, CVV, 3DS, BIN routing, and standard velocity rules. Merchants get standard dispute support but no per-screen ML scoring and no liability shift product. Manual review depends on the gateway, often Authorize.net or NMI, and rules are configured at the gateway level. Membership savings are the headline; fraud sophistication is not.

The membership models target $50K to $500K monthly merchants who want low effective rates on stable card mixes. They fit established B2B and service businesses where fraud risk is moderate and a paid fraud subscription would erode the membership savings. They do not fit high-fraud card-not-present verticals where a tunable ML model earns its keep.

Verdict

Stripe Radar wins on AI fraud detection for the $25K to $5M merchant tier in 2026, driven by per-screen pricing transparency, the largest training data set in the comparison, and merchant-tunable rules with 90-day backtesting. Card-not-present merchants from $25K to $2M monthly get the broadest coverage at predictable cost. Worldpay FraudSight takes the enterprise card-not-present pick above $2M monthly, where managed risk review and FIS-network training matter. PayPal Fraud Protection Advanced is the niche pick for marketplaces with concentrated chargeback exposure on PayPal-funded volume. Square fits in-person retail under $200K monthly. Clover fits merchants who want a bundled POS with light screening. Helcim, Stax, and Payment Depot fit merchants whose fraud profile is moderate enough that gateway rules suffice. Match the fraud tool to your card mix, not to the loudest marketing.