TL;DR

Square wins on fast funding for in-person merchants under $200K monthly. Same-day deposits are free if batched before 5pm Pacific, and instant transfers run 1.75 percent per push. Stripe Instant Payouts at 1.5 percent (minimum $0.50) fit online-only operators above $100K monthly. PayPal instant transfer caps at $25 per push, which favors larger batches. Helcim is the runner-up where the effective rate matters more than speed above $50K monthly volume.

How we ranked

We scored each processor on six explicit criteria. Standard funding speed measured the rolling cycle a merchant gets with no extra fee, scored as T+0 (same day), T+1, or T+2. Instant option captured whether the processor pushes funds to a debit card or bank within minutes. Instant transfer fee covered the per-push percent or dollar charge. Effective rate at $100K monthly volume was estimated from each provider's published pricing applied to a mid-tier card mix of roughly 60 percent credit, 40 percent debit. Contract length and early termination fee weighted month-to-month above multi-year. Hardware lock-in penalized processors whose terminals only run on their network, since switching means scrapping the device.

At a glance

| Provider | Standard funding | Instant option | Instant fee | Best for | Watch out for |

|---|---|---|---|---|---|

| Square | T+0 if before 5pm PT | Yes (debit) | 1.75 percent | In-person retail under $200K/mo | Account holds can freeze deposits |

| Stripe | T+2 rolling | Yes (debit) | 1.5 percent, $0.50 min | Online platforms $100K+/mo | First payout takes 7 to 14 days |

| PayPal | T+1 | Yes (debit/bank) | 1.75 percent, $25 cap | Instant pushes above $1,450 | 3.49 percent standard online rate |

| Clover | T+1 | Rapid Deposit | Acquirer-specific | Restaurants on Clover hardware | Hardware lock-in |

| Helcim | T+1 | None | n/a | $50K+/mo lowest effective rate | No instant push option |

Square

Square publishes a flat 2.6 percent plus $0.10 for tapped, dipped, or swiped card-present transactions and 2.9 percent plus $0.30 for online checkout (Square pricing). Standard deposits arrive next business day at no fee. Same-day batching is free if the day's transactions close before 5pm Pacific Time on a business day. Instant Transfer pushes funds to a linked debit card within minutes for 1.75 percent per transfer, with no per-transfer minimum.

Square's funding pipeline is the cleanest in this comparison set for one reason: there is no separate underwriting cycle for the same-day cutoff. Once the account is active, the 5pm batch reaches your bank that night. The trade is that Square reserves the right to hold deposits when fraud triggers fire, and public reports describe 30 to 90 day holds with limited recourse beyond email support.

For an operator running $80K to $200K monthly in retail or quick-service food, Square's combination of zero monthly fee, instant transfer, and same-day batch is hard to beat. Above $250K monthly the 2.6 percent flat rate starts losing to interchange-plus by 0.30 to 0.45 percent, depending on card mix.

Stripe

Stripe charges 2.9 percent plus $0.30 for online card payments and 2.7 percent plus $0.05 for in-person (Stripe pricing). Standard payouts run on a T+2 rolling schedule once the account is past its first payout. Stripe holds the first payout 7 to 14 days while underwriting completes. Instant Payouts push eligible Visa and Mastercard debit balances to a linked debit card within 30 minutes for 1.5 percent, with a $0.50 minimum per payout.

Two constraints matter. First, Instant Payouts only work for funds settled from eligible debit cards. A merchant whose card mix is mostly credit cannot push the credit portion of a batch. Second, at $100K monthly volume the instant push fee at 1.5 percent runs about $1,500 per $100K pushed. That cost makes sense for ops teams covering payroll or supplier payments that would otherwise wait two business days. It does not make sense as the default for every payout cycle.

PayPal

PayPal charges 3.49 percent plus $0.49 for standard online card processing, 2.59 percent plus $0.49 for Advanced Card Processing, and 2.29 percent plus $0.09 for in-person tapped cards (PayPal business fees). Standard transfers from a PayPal balance to a linked U.S. bank arrive next business day at no fee. Instant transfer pushes balances to a linked debit card or bank within minutes for 1.75 percent, capped at $25 per transfer.

The 1.75 percent fee with a $25 cap makes PayPal the cheapest instant option in this comparison for any single push above roughly $1,450. Below that threshold, Stripe Instant Payouts at 1.5 percent come out cheaper. The trade is the standard rate. PayPal's 3.49 percent plus $0.49 standard online rate runs 0.55 to 0.80 percent above Stripe for the same card mix. An operator who already runs PayPal as a checkout button can use the instant push for cash flow. Routing fresh card volume through PayPal just to chase the cap is overpaying on the front end.

Clover

Clover bundles hardware and software with monthly plans from $14.95 to $54.95 and per-transaction rates of 2.3 to 2.6 percent plus $0.10 for in-person, 3.5 percent plus $0.10 for keyed (Clover pricing). Standard deposits run next business day. Clover Rapid Deposit pushes funds to a linked bank account within minutes for a per-transfer fee that varies by acquirer. Many Clover merchants are signed under a Fiserv, Bank of America Merchant Services, or Wells Fargo Merchant Services back end, and the Rapid Deposit fee is set by that acquirer rather than Clover itself.

That distinction matters. Two Clover merchants on the same hardware can pay different Rapid Deposit fees depending on which acquirer holds the merchant ID. Operators should ask for the specific Rapid Deposit fee schedule in writing before signing. Clover hardware is locked to the Clover network. A Station Duo, Mini, or Flex bought through one acquirer cannot move to a different processor without re-keying or replacing the unit.

For a single-location restaurant that wants a same-day deposit option without managing the back end, Clover works. For a multi-location operator who may switch processors, the hardware lock-in cost can clear $3,000 per location at refresh time.

Helcim

Helcim runs interchange-plus pricing with no monthly fee. Card-present transactions cost interchange plus 0.40 percent plus $0.08, and card-not-present cost interchange plus 0.50 percent plus $0.25 (Helcim pricing). Standard deposits arrive next business day at no fee. Helcim does not currently offer an instant transfer or same-day push.

Helcim earns a spot in this comparison because next-day funding at no fee is faster than most interchange-plus competitors that batch on a T+2 cycle. For an operator at $100K monthly volume with a mid-tier card mix, the effective rate on Helcim runs roughly 2.30 to 2.50 percent against Square's 2.60 to 2.70 percent flat. That gap is $100 to $300 saved per $100K processed, which over a year compounds well beyond what an occasional instant push would cost on Square or Stripe.

The trade is real. If your business depends on receiving funds within hours, Helcim cannot do that. If your cash cycle tolerates next business day, Helcim is the lower-cost option above $50K monthly and gets more competitive as volume rises through Helcim's automatic interchange-plus markup reductions.

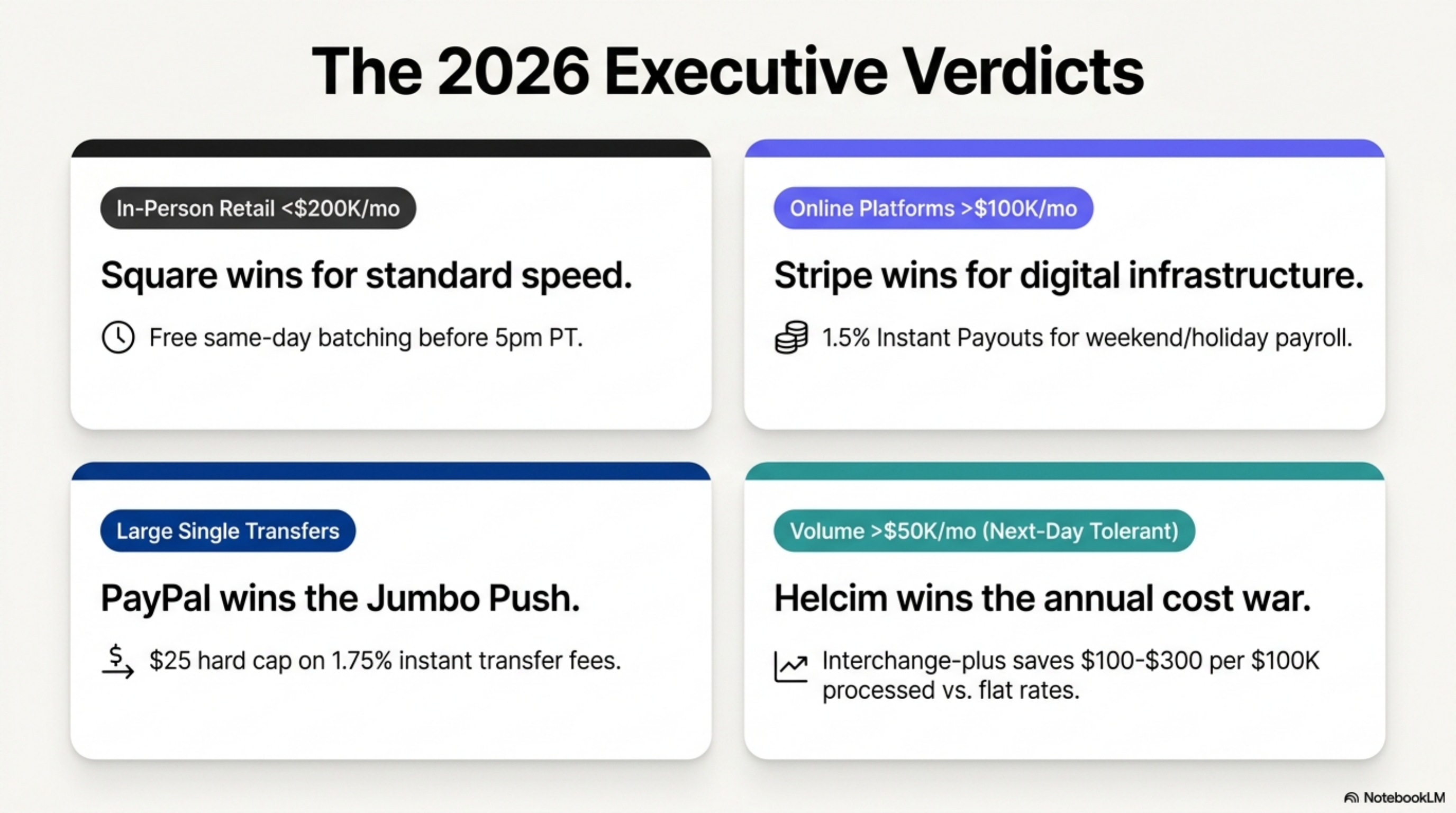

Verdict

For in-person operators under $200K monthly who want a same-day deposit by default and an instant push option for emergencies, Square wins. Zero monthly fee, free same-day batch before 5pm Pacific, and 1.75 percent instant transfer covers most cash-flow scenarios without contract risk. For online-only or platform merchants above $100K monthly, Stripe Instant Payouts at 1.5 percent (minimum $0.50) is the cleaner fit, particularly where the team needs payouts on weekends or holidays.

PayPal wins narrowly for one specific case: pushing a single balance above $1,450 to bank in minutes, where the $25 cap makes it the cheapest instant option in this set. Above $50K monthly volume with no instant requirement, Helcim's interchange-plus pricing at next-day funding beats every flat-rate option in this comparison on annual cost. Federal Reserve payments data shows same-day ACH volume grew sharply through 2024 and 2025 (Federal Reserve Payments Studies), and most acquirers have followed by offering some form of instant push at a per-transfer fee. Interchange schedules from Visa and Mastercard remain the baseline cost behind every rate shown above.