TL;DR

For merchants between $25K and $75K monthly volume, Helcim's interchange-plus pricing with no monthly fee delivers the lowest effective rate without a contract. Above $100K monthly, Payment Depot's wholesale membership pulls ahead by stripping the percentage markup. Stax fits the middle when 24/7 support matters. Square wins for ticket-based retail under $20K monthly, PayPal for in-person micro-merchants needing brand trust. Stripe and Clover charge more per swipe in exchange for software bundling. The runner-up case: high-ticket B2B should price Stax against Helcim head to head.

How we ranked

We weighed six criteria across U.S. processors that publish pricing and serve merchants from $25K to $5M monthly volume.

- Effective rate at $250K monthly volume, computed against a typical retail card mix using the published Visa interchange schedule and Mastercard interchange.

- Contract length and early termination fee.

- Settlement speed in business days from batch to bank.

- Hardware lock-in and proprietary terminal cost.

- Level 2 and Level 3 data support for B2B card-not-present.

- Dispute response SLA and chargeback handling fee.

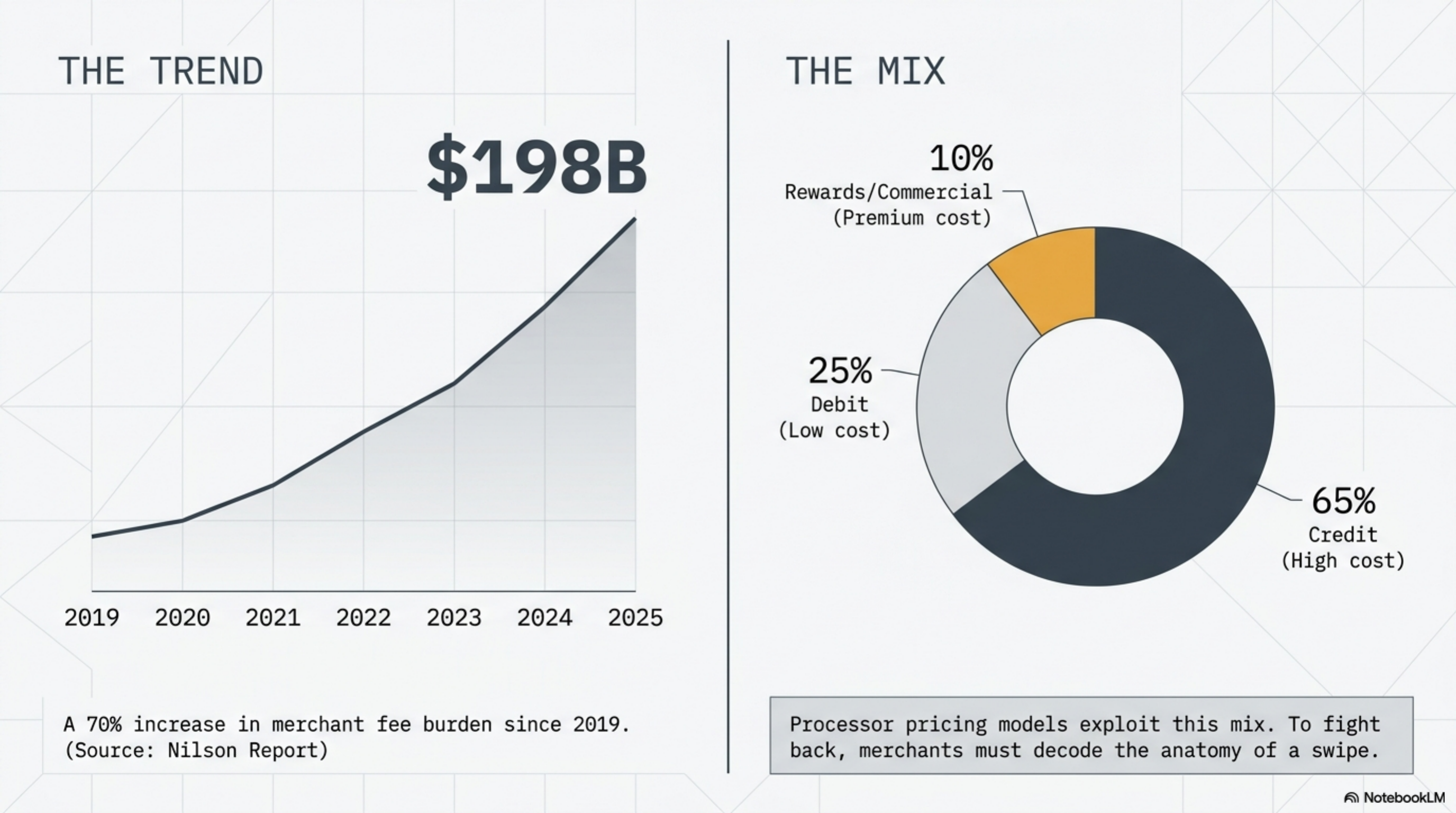

We excluded processors that quote only on request without publishing rates publicly, which is why Worldpay is not ranked. We pulled headline rates from each provider's public pricing page as of June 2026. Volume bands assume a card mix of 65 percent credit, 25 percent debit, and 10 percent rewards or commercial cards, in line with the Federal Reserve Payments Study averages.

At a glance

Headline rates from each processor's public pricing page, ordered by typical effective rate at $250K monthly retail volume.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Helcim | IC + 0.40% + $0.08 in-person | None | T+2 | $25K to $250K, B2B | Business-hours support only |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 | Month-to-month | T+2 | $100K to $500K retail | M to F U.S. support hours |

| Stax | $99/mo + IC + $0.08 to $0.18 | Annual | T+2 | $50K to $500K, high ticket | ETF on annual plan |

| Square | 2.6% + $0.10 in-person | None | T+1 free, same-day +1.75% | Under $20K retail and food | Hardware locked, reserve risk |

| PayPal | 2.29% + $0.09 in-person | None | T+1 | Micro-merchants, pop-ups | 3.49% standard online rate |

| Stripe | 2.9% + $0.30 online | None | T+2 | SaaS, platforms, under $40K | Premium above $100K volume |

| Clover | $14.95 to $54.95/mo + 2.3 to 2.6% + $0.10 | Varies by acquirer | T+1 | Turnkey POS retail | Hardware locked to acquirer |

Helcim

Helcim publishes interchange-plus rates with no monthly fee, no setup fee, and no early termination clause. Online runs interchange plus 0.50 percent plus $0.25. In-person runs interchange plus 0.40 percent plus $0.08. The markup steps down automatically at published volume thresholds, so a $500K monthly retail merchant pays a lower percent markup than a $50K merchant on the same plan.

Hardware: a Helcim Card Reader costs $109 with no proprietary lock-in. The gateway is included for online transactions, and Helcim's API surface supports Level 2 and Level 3 data for B2B commercial cards.

Who it's for: merchants under $250K monthly volume who want IC+ pricing without negotiating a contract, plus B2B merchants paying high commercial card interchange who need Level 3 data to qualify down to lower rates.

Who should avoid: high-ticket dispute-heavy businesses where business-hours chargeback support may not match a 24/7 account manager at a larger processor.

Payment Depot

Payment Depot bundles wholesale IC+ pricing into a monthly membership ranging from $79 to $199 per month, with per-transaction fees of $0.05 to $0.15 depending on plan and card type. Above the membership fee, merchants pay raw interchange with no percentage markup. Contracts vary by plan and are typically month-to-month above the basic tier.

Hardware: works with several open POS systems and standalone terminals from $99 to $899. No proprietary lock-in.

Who it's for: high-volume retail and restaurant merchants in the $100K to $500K monthly range who want the lowest possible effective rate without negotiating a custom contract. A $200K monthly merchant on the $79 plan typically lands below 2.1 percent effective on a typical card mix, which beats every flat-rate option in this comparison.

Who should avoid: low-volume merchants where the fixed membership cost overwhelms the wholesale savings, and businesses needing weekend support since Payment Depot operates U.S. business hours only.

Stax

Stax charges a flat $99 per month membership on top of interchange, with per-transaction fees of $0.08 in-person and $0.18 online. There is no percentage markup above interchange on the standard plan. Annual contracts apply and an early termination fee can run several hundred dollars depending on plan tier.

Hardware: Stax sells card readers and integrates with a small set of third-party POS systems. Terminal cost runs $375 to $1,200 depending on form factor.

Who it's for: merchants above $50K monthly volume where the $99 monthly fee is amortized into a meaningful percent savings versus flat-rate processors. A merchant doing $80K monthly at a 2.5 percent average interchange would pay roughly $99 plus 1.95 percent in effective fees on Stax versus 2.6 percent or higher on Square.

Who should avoid: seasonal merchants and any business below $30K monthly volume, where the membership fee eats the savings during slow months.

Square

Square charges 2.6 percent plus $0.10 in-person, 2.9 percent plus $0.30 online, and 3.5 percent plus $0.15 for keyed transactions. The standard POS software is free. Square offers same-day settlement for an additional 1.75 percent fee or next-day at no extra cost.

Hardware: Square Reader at $49, Square Stand at $149, Square Register at $799. Hardware is locked to Square's processing network, so leaving Square means buying new equipment.

Who it's for: small retail, food service, and mobile merchants under $20K monthly volume who value the bundled free POS and Square Online integration. The bundled stack typically saves $100 to $300 per month versus integrating a third-party POS with an IC+ processor.

Who should avoid: high-volume retail above $40K monthly, where flat-rate pricing pulls 0.30 to 0.50 percent above an IC+ effective rate, and any merchant with seasonal volume spikes that can trigger Square's reserve clauses.

PayPal

PayPal publishes three tiers: Standard at 3.49 percent plus $0.49, Advanced Card at 2.59 percent plus $0.49, and in-person at 2.29 percent plus $0.09. The 2.29 percent in-person rate is the lowest public flat rate for card-present transactions in this comparison, undercutting Square by 0.31 percent on the percentage component.

Hardware: PayPal Zettle reader at $29, with no contract.

Who it's for: micro-merchants and pop-up retail where the low in-person rate matters and the PayPal branded checkout drives marginal conversion lift on the online store. The Nilson Report tracks PayPal as a top-five U.S. card-not-present brand by volume.

Who should avoid: B2B card-not-present merchants. The 3.49 percent Standard rate is the worst public flat rate among the seven processors here, and PayPal does not pass through Level 2 or Level 3 data discounts on commercial cards.

Stripe

Stripe publishes flat-rate pricing at 2.9 percent plus $0.30 online and 2.7 percent plus $0.05 in-person, with no monthly fee on the standard plan. Volume-based discounts exist but are negotiated above $80K monthly through Stripe's sales team. Settlement runs T+2 by default, faster on Instant Payouts for an additional 1.5 percent fee.

Hardware: the Stripe Reader M2 runs $59 and the Stripe Reader S700 runs $349. Hardware is unlocked, no contract.

Who it's for: SaaS and platform companies with developer resources to build on Stripe's API, marketplaces using Connect, and merchants under $40K monthly where the flat rate is competitive against IC+ once monthly fees are accounted for.

Who should avoid: high-volume in-person retail above $100K monthly. At that volume the 2.7 percent flat-rate markup costs 0.40 to 0.55 percent above an IC+ alternative, which compounds to five-figure annual cost.

Clover

Clover sells monthly software plans from $14.95 to $54.95 stacked on transaction fees of 2.3 to 2.6 percent plus $0.10 in-person and 3.5 percent plus $0.10 for keyed. Plan and rate depend on the Clover acquirer reselling the system, which can be Fiserv, Bank of America, or a regional ISO. Pricing varies by reseller.

Hardware: proprietary. Clover Mini runs $799, Clover Station Solo $1,699, and Clover Flex $599.

Who it's for: small retail and restaurants who want a turnkey POS with table service, inventory, and reporting bundled, and who do not want to manage software and processing separately.

Who should avoid: any merchant with leverage to negotiate IC+, since the same Clover hardware can be paired with multiple acquirers at very different rates. Always compare your Clover quote against an independent IC+ benchmark before signing.

Verdict

For low-fee processing across $25K to $5M monthly volume, Helcim wins at the low end and Payment Depot wins at the high end. Helcim's no-monthly-fee IC+ structure makes it the lowest-cost option for merchants between $25K and $75K monthly volume, where a $79 membership on Payment Depot is hard to amortize. Above $100K monthly, Payment Depot's wholesale rates plus a flat membership beat Helcim's percentage markup. Stax sits in between for merchants who prefer 24/7 support over Helcim's business-hours model. Stripe and Square remain the right answer only for software-bundled use cases under $40K monthly, where the convenience of a unified stack outweighs the percentage premium.