TL;DR

True multi-acquirer routing in 2026 sits with three providers from this list: Stripe, Worldpay, and PayPal Braintree. They split traffic across acquiring banks to lift authorization rates and reduce decline costs. Stripe wins for mid-market merchants between $250K and $5M monthly volume thanks to Adaptive Acceptance. Worldpay wins above $5M where custom interchange-plus and dedicated routing matter. The other providers in this list run single-acquirer stacks and should not be sold to you as multi-acquirer.

How we ranked

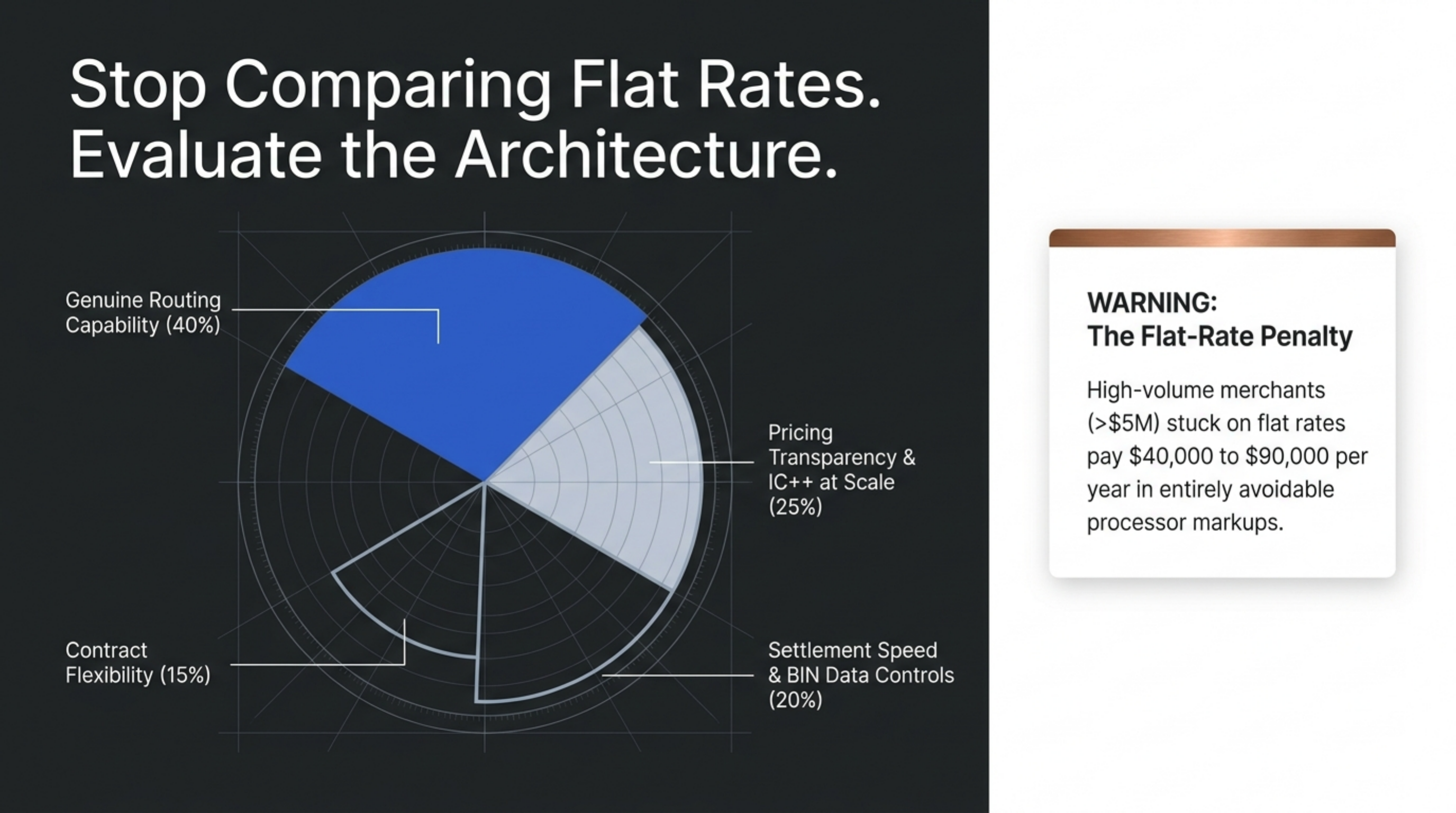

Multi-acquirer comparisons are not flat-rate comparisons. The operator cares about four things: actual acquirer routing capability, pricing transparency at $250K+ monthly volume, contract terms, and approval-rate uplift evidence. We weighted the criteria as follows: genuine multi-acquirer routing (40%), pricing transparency and effective rate disclosed against Visa and Mastercard interchange schedules (25%), contract length and early termination fees (15%), settlement speed (10%), and level 2 and 3 data plus BIN-based routing controls (10%). Providers that resell a single acquirer's BIN as their own are not multi-acquirer regardless of marketing language. We checked each provider's public pricing page and verified card-network rules against Federal Reserve payments studies.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online / 2.7% + $0.05 in-person | Month-to-month | T+2 | $250K to $5M online | Above $1M, move to IC++ contract |

| Worldpay | Custom IC++ | 3 years typical | T+1 | $5M+ enterprise | Long contracts, tiered ETF |

| PayPal Braintree | 2.59% + $0.49 advanced / 3.49% + $0.49 standard | Month-to-month | T+1 | B2C with PayPal demand | Standard rate punishes B2B card-not-present |

| Helcim | IC + 0.40% + $0.08 in-person / IC + 0.50% + $0.25 online | Month-to-month | T+2 | $25K to $250K IC++ buyers | Single acquirer (Elavon), no routing |

| Stax | $99/mo + IC + $0.08 to $0.18 | Month-to-month | T+2 | $50K+ where membership beats markup | Single acquirer, no routing |

| Square | 2.6% + $0.10 in-person / 2.9% + $0.30 online | Month-to-month | T+1 | Under $50K retail and food | Own stack, no routing |

| Clover | Plans $14.95 to $54.95/mo + 2.3% to 2.6% + $0.10 | Varies by reseller | T+1 | SMB POS hardware bundle | Fiserv ISO ETFs and leases |

Stripe

Stripe publishes 2.9% + $0.30 for online cards and 2.7% + $0.05 for in-person on its standard pricing page. The relevant feature here is Adaptive Acceptance, which retries failed authorizations through additional acquiring relationships within seconds of the first decline. For merchants above $1M monthly volume, Stripe will move you to interchange-plus on a custom contract, and the effective markup typically lands between IC + 0.30% and IC + 0.55% depending on card mix.

Contract terms are month-to-month with no early termination fee on standard pricing. Settlement is T+2 by default, T+1 with Instant Payouts at 1.5% per transfer. Best fit: software, marketplaces, and subscription merchants between $250K and $5M monthly volume that benefit from automated retry routing and need direct API access. Avoid Stripe flat rate if you are above $5M monthly volume processing primarily commercial cards. The cost of staying on standard pricing at that scale is roughly $40,000 to $90,000 per year of avoidable markup.

Worldpay

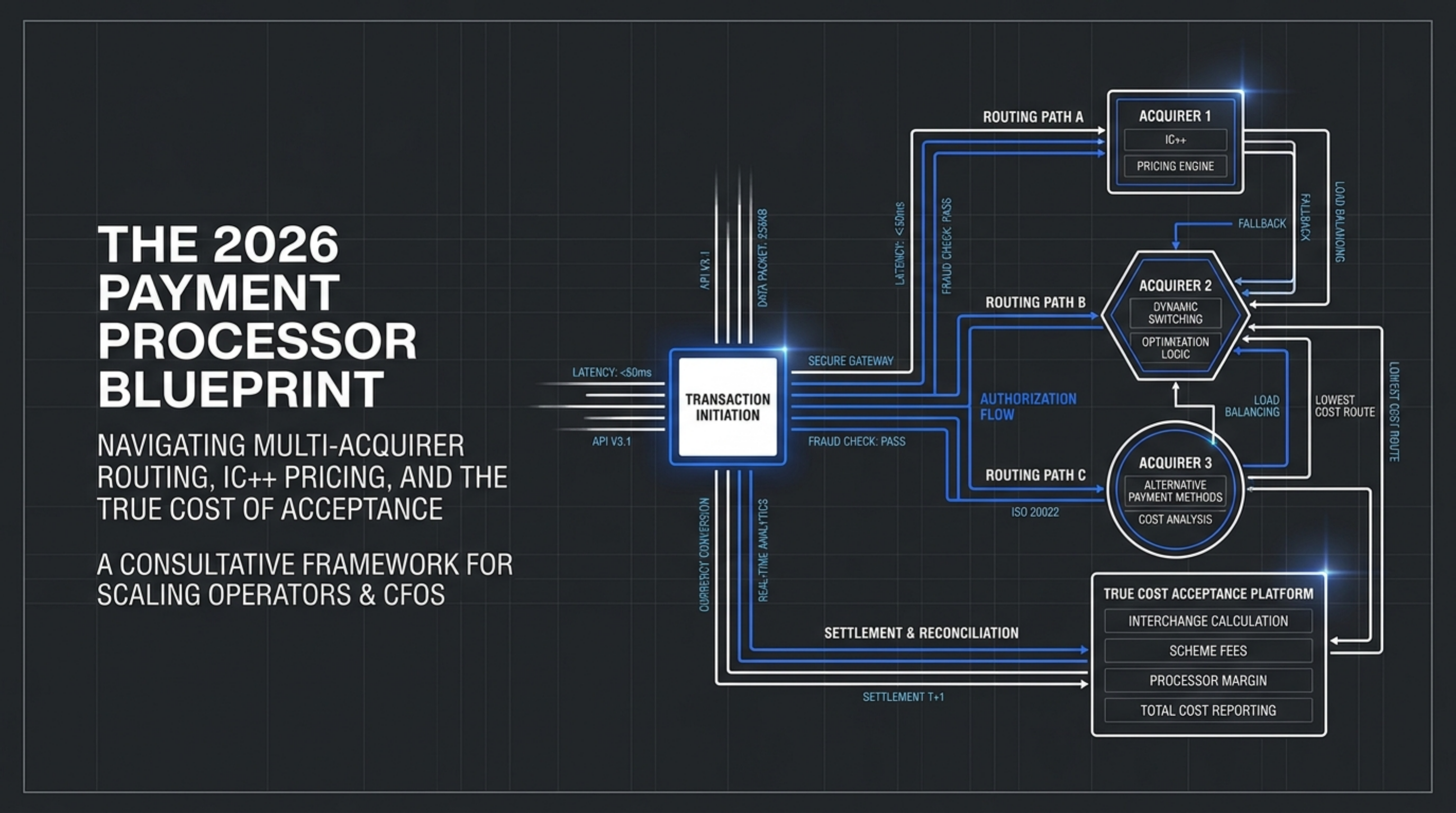

Worldpay does not publish flat-rate pricing. Its enterprise stack runs on interchange-plus quoted on contract, typically with a 3-year initial term and tiered early termination fees. Setup runs 7 to 14 days and includes underwriting, BIN sponsorship setup, and gateway provisioning. The multi-acquirer story here is genuine: Worldpay can route the same merchant through different acquiring BINs across Visa, Mastercard, Amex, and international networks based on issuer geography, card type, and decline reason.

Best fit: $5M+ monthly volume merchants with cross-border traffic, high B2B card-not-present mix, or aggressive auth-rate targets. The Nilson Report rankings put Worldpay among the top U.S. merchant acquirers by purchase transactions, which gives the routing logic real coverage. Avoid Worldpay if you process under $1M monthly. The fixed monthly minimums, statement fees, and PCI fees will swallow any IC++ savings at that scale, and you will spend more time managing the account than running it.

PayPal Braintree

PayPal's business fees page lists Standard credit and debit at 3.49% + $0.49, Advanced credit and debit at 2.59% + $0.49, and in-person at 2.29% + $0.09. The Braintree side of the business supports multi-acquirer routing on enterprise contracts, and the PayPal wallet button on checkout pulls from the customer's PayPal balance through a separate funding flow that does not touch the card networks.

Contract is month-to-month for standard accounts, custom for Braintree enterprise. Settlement is T+1 in most cases. Best fit: consumer-facing brands where the PayPal button drives 10% or more of checkout conversion. The wallet acceptance plus card processing on one merchant of record is the actual edge.

Watch out for the 3.49% + $0.49 standard rate on B2B card-not-present transactions. On a $5,000 invoice that is $175.99 per transaction. Compare against an IC++ provider at IC + 0.40% on a commercial card and you save roughly $100 per transaction.

Helcim

Helcim's published pricing is interchange-plus from the first dollar: IC + 0.40% + $0.08 in-person and IC + 0.50% + $0.25 online, with automatic volume discounts that lower the markup as you scale. No monthly fee, no PCI fee, no statement fee. The underlying acquirer is single-source, not multi-acquirer. There is no cross-acquirer routing.

Best fit: $25K to $250K monthly volume merchants that want transparent IC++ pricing without subscribing to a membership model. Above $250K, the Helcim markup compresses, but you should price-check against Stax membership math at $50K+ where the fixed monthly fee starts to beat the variable markup. Avoid Helcim if multi-acquirer routing or BIN-level optimization is a requirement. It does not exist on this stack regardless of how the sales conversation frames it.

Stax

Stax charges a $99 per month membership plus interchange pass-through and a per-transaction fee of $0.08 in-person or $0.18 online. The math wins at roughly $50K monthly volume on average ticket sizes above $40, where the fixed membership beats a percentage markup. Stax acquired Payment Depot in 2021, so the underlying acquiring is consolidated under one banner regardless of which brand sold you the account.

Contract is month-to-month on standard plans. Settlement is T+2. Best fit: $50K to $500K monthly volume merchants on stable card mix that want predictable monthly cost. Avoid Stax if you process small-ticket retail under $20 average. The per-transaction fee on small tickets erodes the savings the membership is supposed to deliver. Like Helcim, Stax is single-acquirer and does not provide cross-acquirer routing. Marketing copy that suggests otherwise should be challenged in writing during procurement.

Square

Square publishes 2.6% + $0.10 for in-person tap or chip, 2.9% + $0.30 for online, and 3.5% + $0.15 for keyed transactions. Square operates its own proprietary acquiring stack and does not route to outside acquirers. Settlement is T+1 by default and instant for an additional 1.75%.

Best fit: under $50K monthly volume retail and food service operators that want same-day setup, free POS software, and a single vendor for hardware and payments. Above $50K monthly volume you are usually paying 0.40% to 0.70% of net sales more than an IC++ provider would cost, which is $200 to $350 per month per $50K of volume. Avoid Square if you need cross-acquirer routing, level 2 and 3 commercial card optimization, or multi-currency settlement. None of those exist on the Square stack today.

Clover

Clover sells plans from $14.95 to $54.95 per month with processing at 2.3% to 2.6% + $0.10 in-person and 3.5% + $0.10 keyed. Clover hardware and software run on the Fiserv acquiring stack, which is single-acquirer. There is no cross-acquirer routing, and the hardware is locked to whichever Fiserv ISO or bank sold you the terminal.

Best fit: SMB retail and restaurant operators under $50K monthly volume that want a hardware and software bundle from one vendor. Avoid Clover if you anticipate multi-location growth, multi-acquirer routing, or international expansion. The hardware lock-in becomes a switching cost the moment you outgrow the original plan.

Verdict

Pick Stripe for $250K to $5M monthly online volume that wants Adaptive Acceptance routing without a 3-year contract. Pick Worldpay for $5M+ enterprise volume where custom interchange-plus, dedicated acquirer routing, and cross-border BIN sponsorship justify the underwriting time. PayPal Braintree wins only when the PayPal wallet button drives meaningful checkout conversion on the consumer side, and only the Advanced rate is competitive on cards.

Everything else in this comparison is single-acquirer. Helcim and Stax win on transparent IC++ pricing at $25K to $500K monthly volume, but neither provides multi-acquirer routing. Square and Clover are single-vendor stacks built for under $50K monthly volume retail. If a sales rep tells you Helcim, Stax, Square, or Clover is multi-acquirer, ask them to put it in writing in the merchant agreement.