TL;DR

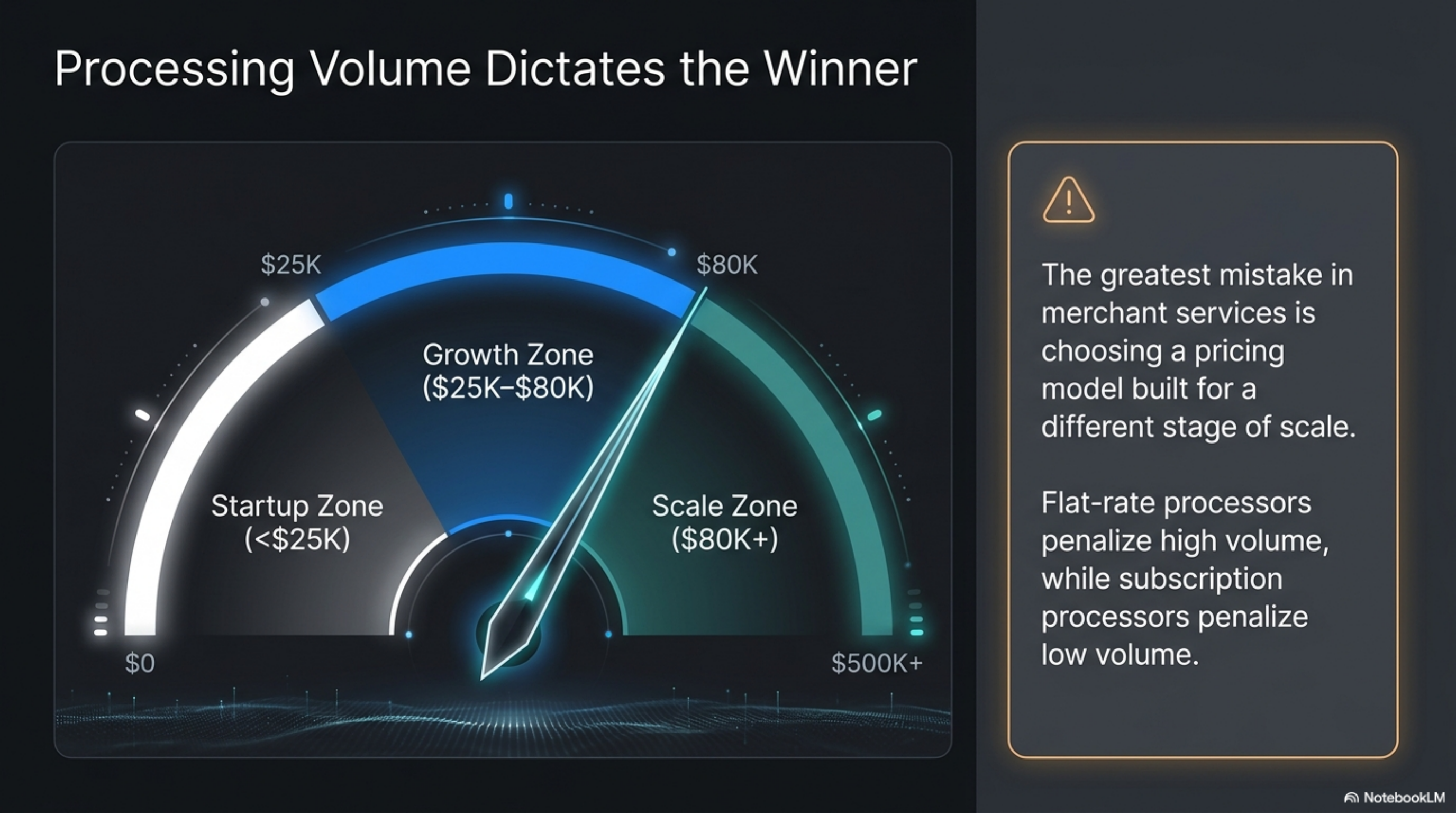

For U.S. merchants processing $25K to $500K per month, Helcim is the best no-contract payment processor in 2026. Interchange-plus pricing, automatic volume discounts, no monthly fee, no early termination clause. Stripe wins for online-only businesses with developer resources. Square wins under $25K per month for retail and food service. Stax and Payment Depot win above $80K monthly volume, where subscription pricing beats per-transaction markup. Avoid Clover units sold through reseller ISOs that bundle multi-year equipment leases.

How we ranked

We graded each processor on six criteria, weighted for an operator running $50K to $500K monthly volume.

- Effective rate at $250K monthly volume on a standard retail card mix (interchange plus assessments plus processor markup), pulled from each processor's published pricing.

- Contract terms. True month-to-month with no early termination fee, versus auto-renew clauses buried in the merchant agreement.

- Equipment and hardware lock-in. Owned terminals score higher than leased units that survive cancellation.

- Funding speed. Standard next-day or two-day ACH versus instant deposit upcharges.

- Level 2 and Level 3 data support for B2B card-not-present volume, which can save 0.50 to 1.00 percent on commercial card transactions per the Visa interchange schedule and Mastercard interchange rates.

- Dispute SLA and chargeback fee, per the processor's terms.

We excluded enterprise processors like Worldpay because public pricing is not posted and standard agreements run two to five years.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online, 2.7% + $0.05 in-person | Month-to-month | 2 days | Online + developer tools | Flat-rate premium above $50K monthly |

| Square | 2.6% + $0.10 in-person, 2.9% + $0.30 online | Month-to-month | Next day | Under $25K retail and food | Instant deposit costs 1.75% |

| Helcim | IC + 0.40% + $0.08 in-person, IC + 0.50% + $0.25 online | Month-to-month | 2 days | $25K to $500K monthly volume | Per-transaction floor on small tickets |

| Stax | $99/mo + IC + $0.08 in-person, $0.18 online | Month-to-month | 1 to 2 days | $80K+ monthly volume | Subscription cost under $50K |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 | Month-to-month | 1 to 2 days | $40K+ monthly volume | POS hardware not included |

| Clover | $14.95 to $54.95/mo + 2.3 to 2.6% + $0.10 in-person | Direct: month-to-month; ISO: 36 to 48 months | Next day | Direct Clover.com purchase | Reseller ISO contracts and equipment leases |

| PayPal | 3.49% + $0.49 standard, 2.29% + $0.09 in-person | Month-to-month | Next day to bank | Low-volume with PayPal-preferring buyers | Standard checkout rate premium |

Stripe

Stripe charges 2.9 percent plus $0.30 online and 2.7 percent plus $0.05 in-person via Stripe Terminal, per Stripe's published pricing. No monthly fee, no contract.

Pricing structure: flat-rate blended. Low-cost debit subsidizes the merchant; rewards cards subsidize Stripe. Markup above interchange-plus runs 0.40 to 0.55 percent at $200K monthly volume on a standard retail mix.

Settlement: two business days standard, dropping with history. Instant payouts cost 1.5 percent.

Hardware: Stripe Terminal readers $59 to $349, owned.

Who it's for: online-first businesses needing a developer API, marketplaces using Stripe Connect, SaaS billing through Stripe Billing.

Who should avoid: in-person retail above $50K monthly where Helcim or Stax produces a 0.30 to 0.50 percent lower effective rate. Skip for B2B corporate cards needing Level 2/3 data, which Stripe supports inconsistently.

Square

Square charges 2.6 percent plus $0.10 in-person, 2.9 percent plus $0.30 online, and 3.5 percent plus $0.15 for keyed card-not-present, per Square's pricing page. Free POS software for retail, restaurants, and appointments on the base tier. No monthly fee, no contract.

Pricing structure: flat-rate blended. Same subsidy dynamics as Stripe. Effective rate runs 2.55 to 2.85 percent on a standard retail mix once tips and category mix shake out.

Settlement: next business day standard. Instant transfer costs 1.75 percent of the transfer amount.

Hardware: magstripe reader free, contactless and chip reader $59, Square Terminal $299, Square Register $799. All owned.

Who it's for: under $25K monthly retail, food trucks, salons, and any business that values turnkey POS over rate optimization. Square's POS, inventory, payroll, and capital stack inside one login is the moat.

Who should avoid: above $50K monthly volume on a card-heavy mix, where flat-rate markup over interchange-plus exceeds $250 per month. Also skip on large-ticket B2B, where the 2.9 percent plus $0.30 keyed rate stacks up against an interchange-plus shop with Level 2 data.

Helcim

Helcim charges interchange plus 0.40 percent plus $0.08 in-person and interchange plus 0.50 percent plus $0.25 online, per Helcim's pricing page. No monthly fee, no PCI fee, no statement fee, no early termination fee. Discounts kick in automatically at $25K, $50K, $100K, and $250K monthly volume tiers.

Pricing structure: interchange-plus pass-through. The merchant pays the actual Visa or Mastercard interchange rate plus Helcim's published markup. Statements show the breakdown line by line, which makes the markup auditable each month.

Settlement: two business days standard. Same-day available for established accounts.

Hardware: Helcim Card Reader $99, sold not leased. Works with the Helcim Smart Terminal and standalone virtual terminal. No proprietary POS lock-in.

Who it's for: any U.S. or Canadian merchant from $25K to $500K monthly volume that wants transparent pricing and no contract. Strong for service businesses, professional services, B2B, and e-commerce on Helcim's own gateway.

Who should avoid: under $10K monthly volume, where the per-transaction floor of $0.08 in-person makes flat-rate Square cheaper on small-ticket sales.

Stax

Stax charges a monthly subscription starting at $99 (Starter), plus interchange plus $0.08 in-person and plus $0.18 online, per Stax's pricing page. No contract on the standard month-to-month plan.

Pricing structure: subscription plus interchange pass-through with no percentage markup above interchange. The merchant pays interchange and assessments, plus a flat per-transaction fee, plus the monthly subscription. This is the closest a small merchant gets to wholesale pricing.

Settlement: one to two business days.

Hardware: terminals from $149 (mobile) to $899 (countertop). Owned outright.

Who it's for: $80K to $500K monthly card volume where the subscription math beats per-transaction markup. At $100K monthly with a standard retail mix, switching from a 0.40 percent markup processor to Stax saves roughly $300 per month after the subscription cost.

Who should avoid: under $50K monthly, where the $99 fixed cost eats most of the markup savings. Also skip if you need 24/7 phone support included in the base plan, since after-hours phone moves to a higher tier.

Payment Depot

Payment Depot charges $79 to $199 per month depending on the plan, plus interchange plus $0.05 to $0.15 per transaction, per Payment Depot's pricing page. Owned by Stax Payments since 2021. Month-to-month membership, cancel anytime.

Pricing structure: subscription plus interchange pass-through, similar to Stax. Lower entry tier ($79) makes the math work at slightly lower volume.

Settlement: one to two business days.

Hardware: works with most existing terminals. New equipment ranges $99 to $799. No lease.

Who it's for: $40K to $200K monthly volume merchants who want wholesale-style pricing with a lower monthly subscription floor than Stax. Strong for established small businesses with steady volume and a simple card mix.

Who should avoid: under $30K monthly, where even the $79 plan exceeds the markup a flat-rate or interchange-plus processor would charge. Also skip if you need omnichannel POS hardware in the box. Payment Depot is a processor first, not a POS company.

Clover

Clover sells POS plans from $14.95 to $54.95 per month plus card processing at 2.3 to 2.6 percent plus $0.10 in-person and 3.5 percent plus $0.10 keyed, per Clover's POS pages. Owned by Fiserv.

Pricing depends on the seller. Direct from Clover.com: month-to-month, no contract, no equipment lease. Through a reseller ISO (how most Clover units reach merchants), typically a 36 to 48 month merchant processing agreement plus a multi-year equipment lease that survives cancellation. Request the lease schedule and merchant agreement before signing; specific lease and ETF amounts vary by ISO.

Settlement: next business day.

Hardware: Clover Go $49, Clover Flex $599, Clover Mini $799, Clover Station Duo $1,799.

Who it's for: small retail and food service buying direct from Clover.com on a true no-contract plan.

Who should avoid: anyone signing through a reseller without reading the contract front to back. Hardware is good; reseller terms often are not.

PayPal

PayPal charges 3.49 percent plus $0.49 for the standard checkout button, 2.59 percent plus $0.49 for advanced card processing, and 2.29 percent plus $0.09 in-person via Zettle, per PayPal's fee schedule. No monthly fee on the base tier, no contract.

Pricing structure: flat-rate blended, with a meaningful premium over Stripe and Square on the standard checkout rate. PayPal monetizes the consumer trust at checkout, not the processing margin.

Settlement: instant to PayPal balance, one to three business days to external bank. Instant transfer to bank costs 1.75 percent.

Hardware: Zettle reader $29, Zettle Terminal $199, owned.

Who it's for: low-volume e-commerce sellers whose customers prefer paying with PayPal balance or Venmo. Strong for cross-border consumer sales and small marketplaces.

Who should avoid: B2B card-not-present at any meaningful volume, where the 3.49 percent plus $0.49 standard rate is roughly 0.60 percent above Stripe and 1.00 percent above interchange-plus from Helcim. Also skip in-person retail above $50K monthly, where Square or a true interchange-plus processor is cheaper.

Verdict

For U.S. merchants doing $25K to $500K per month who want a true no-contract payment processor in 2026, Helcim wins. Interchange-plus pass-through pricing, automatic volume discounts at $25K, $50K, $100K, and $250K, no monthly fee, no early termination fee, no equipment lease. Statements show the actual interchange line by line, so the markup is auditable each month per the published Visa and Mastercard rate schedules.

Above $80K monthly volume on a clean card mix, Stax or Payment Depot can beat Helcim by $100 to $400 per month if you run the subscription math against your statement. Under $25K monthly, Square's free POS plus 2.6 percent plus $0.10 in-person is cheaper and easier than any interchange-plus account. For online-only businesses with a developer team, Stripe remains the default despite the 0.40 to 0.55 percent flat-rate premium, because the API and tooling savings outweigh the rate gap.