TL;DR

For B2B SaaS in 2026, Stripe wins on the strength of its Billing product, recurring infrastructure, and global card coverage, especially for companies under $1M monthly card volume. Above $250K monthly with a commercial-card-heavy mix, Helcim's interchange-plus pricing usually beats Stripe's flat rate by 0.3 to 0.6 percent of revenue. Worldpay fits enterprise SaaS above $5M monthly with custom contracts. PayPal is the weakest fit for B2B card-not-present and should not sit as a primary processor.

How we ranked

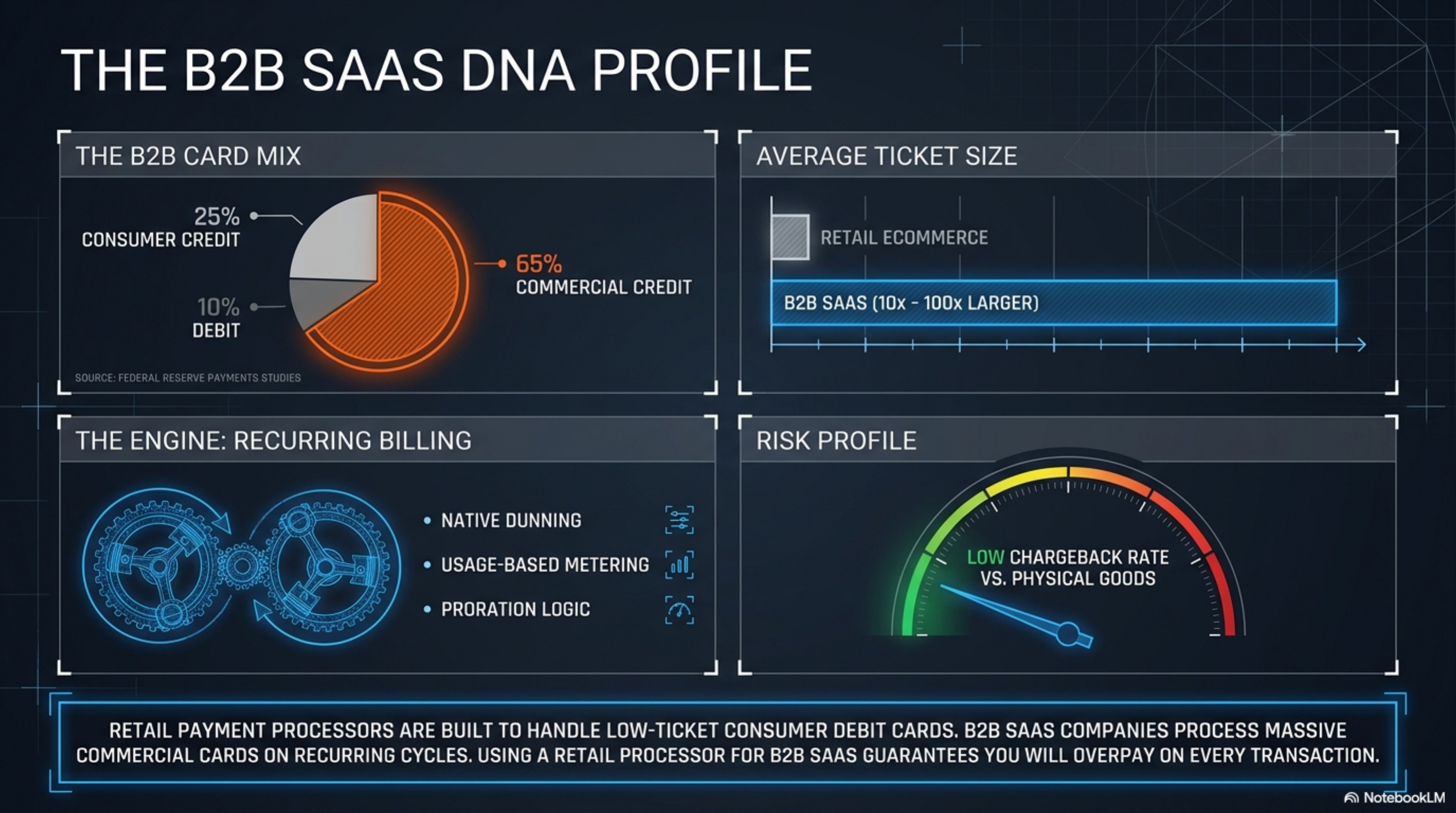

B2B SaaS payments look nothing like retail. Average ticket sizes run 10x to 100x retail, the commercial card mix is heavier, chargebacks are lower, and recurring billing is the whole business. We weighted six criteria.

- Effective rate at $100K and $500K monthly volume. Modeled against a typical SaaS card mix of 65 percent commercial credit, 25 percent consumer credit, and 10 percent debit, drawing on data from the Federal Reserve payments studies.

- Recurring billing infrastructure. Native dunning, smart retry, proration, usage-based metering, account updater.

- Level 2 and Level 3 data passthrough. Commercial cards qualify for lower interchange categories when extra purchase data is sent. See the Visa Interchange schedule and Mastercard Interchange.

- ACH and wire support. Invoices above $5K usually move to ACH for cost reasons.

- Contract length and early termination fee. Month-to-month preferred.

- Settlement speed and reserves. SaaS cash flow can survive T+2; reserves can break a Series A.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online | Month-to-month | T+2 | Early to mid-stage SaaS | Billing add-ons stack at scale |

| Helcim | IC + 0.50% + $0.25 online | Month-to-month | T+2 | $100K to $1M monthly volume | Subscription tooling is basic |

| Stax | $99/mo + IC + $0.18 online | Month-to-month | T+2 | $80K+ steady volume | Loses under $30K monthly |

| Payment Depot | $79-$199/mo + IC + $0.05-$0.15 | Month-to-month | T+2 | $50K+ predictable volume | Add-on fees by tier |

| Worldpay | Custom IC+ (contact sales) | 3-year typical | T+1 | $5M+ monthly enterprise | ETF and minimums on contracts |

| PayPal | 3.49% + $0.49 standard | Month-to-month | T+1 | Secondary checkout only | High keyed and CNP rates |

Stripe

Stripe charges 2.9 percent plus $0.30 on standard online card payments and 2.7 percent plus $0.05 in person, per Stripe's public pricing. International cards add 1.5 percent. Currency conversion adds another 1 percent. Stripe Billing, the recurring infrastructure, adds $0.50 per active subscription on Starter or 0.7 percent of recurring revenue on Scale.

For B2B SaaS under $250K monthly card volume, the all-in effective cost usually lands at 3.1 to 3.5 percent of card revenue once Billing is added. Above $1M monthly, Stripe will quote interchange-plus pricing on request, typically IC + 0.20 to 0.35 percent plus a per-transaction fee.

The case for Stripe is the developer experience: webhooks, idempotency, test mode, prebuilt Checkout, Stripe Tax, Radar for fraud, the Customer Portal, account updater, and Smart Retries. The account updater automatically refreshes expired commercial cards from issuers, which matters for B2B where churn from card expiry is a real revenue leak.

Who it's for: any SaaS company processing under $1M monthly, especially with a global customer base. Who should avoid it: companies above $1M monthly with a commercial-card-heavy mix, where flat-rate pricing leaves 0.3 to 0.6 percent of revenue on the table versus interchange-plus.

Helcim

Helcim publishes interchange-plus pricing on its public pricing page. Online card-not-present pays interchange plus 0.50 percent plus $0.25; in-person pays interchange plus 0.40 percent plus $0.08. The margin compresses automatically as volume grows: at $250K monthly the markup steps down to around 0.30 percent, and above $500K monthly to roughly 0.18 percent.

Level 2 and Level 3 data are passed automatically when the extra fields are supplied at checkout, so commercial cards drop into the lower interchange tiers Visa and Mastercard publish. For a B2B SaaS with a 65 percent commercial card mix, that alone can reduce effective rate by 0.4 to 0.6 percent.

ACH is 0.5 percent capped at $6 per transaction. There is no monthly fee, no PCI fee, no batch fee, no statement fee. The terms of service are month-to-month with no early termination fee.

Who it's for: B2B SaaS between $100K and $1M monthly card volume, with at least a 40 percent commercial card mix. Who should avoid it: companies that need native usage-based metering, complex proration, or a deep revenue recognition export. Helcim's recurring billing is functional but thin compared with Stripe Billing or Chargebee.

Stax

Stax (formerly Fattmerchant) charges a flat subscription of $99 per month and passes interchange straight through, adding $0.08 per in-person transaction and $0.18 per online transaction, per its public pricing page. Higher tiers at $159 and $199 per month layer on additional reporting and ACH features.

The math only works above a breakeven point. For a B2B SaaS at $50K monthly card volume with an average ticket of $400, the subscription model saves roughly $300 to $500 per month against flat rate. Below $30K monthly, the $99 fee usually erases any savings. Above $200K monthly, the model starts to lose to true interchange-plus because Stax does not reduce the per-transaction fee as volume grows.

Stax includes a payment dashboard, virtual terminal, and a billing module that handles basic subscriptions and saved cards. Level 2 and Level 3 data are supported with manual configuration on the higher tier.

Who it's for: steady SaaS card volume between $50K and $200K monthly, with a high average ticket. Who should avoid it: low-ticket SaaS where the $0.18 per-transaction fee compounds, and companies under $30K monthly where the subscription erases the savings.

Payment Depot

Payment Depot operates a membership pricing model: monthly fees of $79, $99, $149, and $199, with interchange passed through and a per-transaction fee of $0.05 to $0.15 depending on tier, per the Payment Depot pricing page. The wholesale-rate idea is similar to Stax but priced more aggressively at the lower membership tiers.

For B2B SaaS with predictable monthly volume between $50K and $300K, Payment Depot typically beats both Stax and Stripe on effective rate by 0.20 to 0.35 percent of card revenue. The savings come from a lower per-transaction fee at the entry tier and a thinner monthly subscription.

Recurring billing is essentially an Authorize.net front-end with saved cards. There is no native dunning, smart retry, or revenue recognition. Companies on Payment Depot usually pair it with a separate billing platform like Chargebee or Maxio.

Who it's for: B2B SaaS with steady $50K to $300K monthly card volume and an existing or planned billing platform. Who should avoid it: teams that want billing and payments in a single stack.

Worldpay

Worldpay is the enterprise option. There is no public flat-rate card. Pricing is interchange-plus on a custom basis, negotiated against monthly volume, average ticket, vertical, and card mix. Typical markups for a $5M-monthly B2B SaaS land between 0.10 and 0.18 percent above interchange, with per-transaction fees of $0.04 to $0.08, in line with the enterprise benchmarks reported by the Nilson Report.

The strengths are settlement infrastructure, dispute handling, dedicated account management, and direct acquirer connections in 40+ countries. Level 2 and Level 3 data passthrough is standard. ACH and wire processing are first-class. Funding is typically T+1.

Who it's for: SaaS companies above $5M monthly with multi-region settlement needs. Who should avoid it: anyone under $1M monthly, where the price advantage will not offset the contract risk or the 7 to 14 day onboarding.

PayPal

PayPal's posted business rates: 3.49 percent plus $0.49 on standard PayPal Checkout, 2.59 percent plus $0.49 on advanced credit and debit card processing, and 2.29 percent plus $0.09 in person, per PayPal's published fee schedule. International transactions add a 1.5 percent fee plus currency conversion.

For B2B SaaS, the math is bad. The 3.49 percent + $0.49 rate sits 0.5 to 0.7 percent above Stripe and 1.0 to 1.5 percent above Helcim on a commercial-card-heavy mix. Level 2 and Level 3 data passthrough is not exposed on the standard product, so commercial card interchange savings are absorbed by PayPal rather than passed to the merchant.

PayPal still has a place as a secondary checkout option for international consumer-facing or prosumer SaaS where buyer trust is the conversion lever. It does not belong as a primary B2B processor.

Verdict

For most B2B SaaS in 2026, Stripe is the default choice up to $1M monthly card volume, on the strength of Billing, Smart Retries, account updater, global card support, and developer tooling. Above $250K monthly with a commercial-card-heavy mix, run a side-by-side quote against Helcim. The interchange-plus economics with Level 2/3 data passthrough usually save 0.3 to 0.6 percent of revenue per year. Above $5M monthly, request a custom Worldpay quote and have legal review the contract before signing. Skip PayPal as a primary processor, skip Stax under $30K monthly, and skip Payment Depot if you do not already have a separate billing platform.