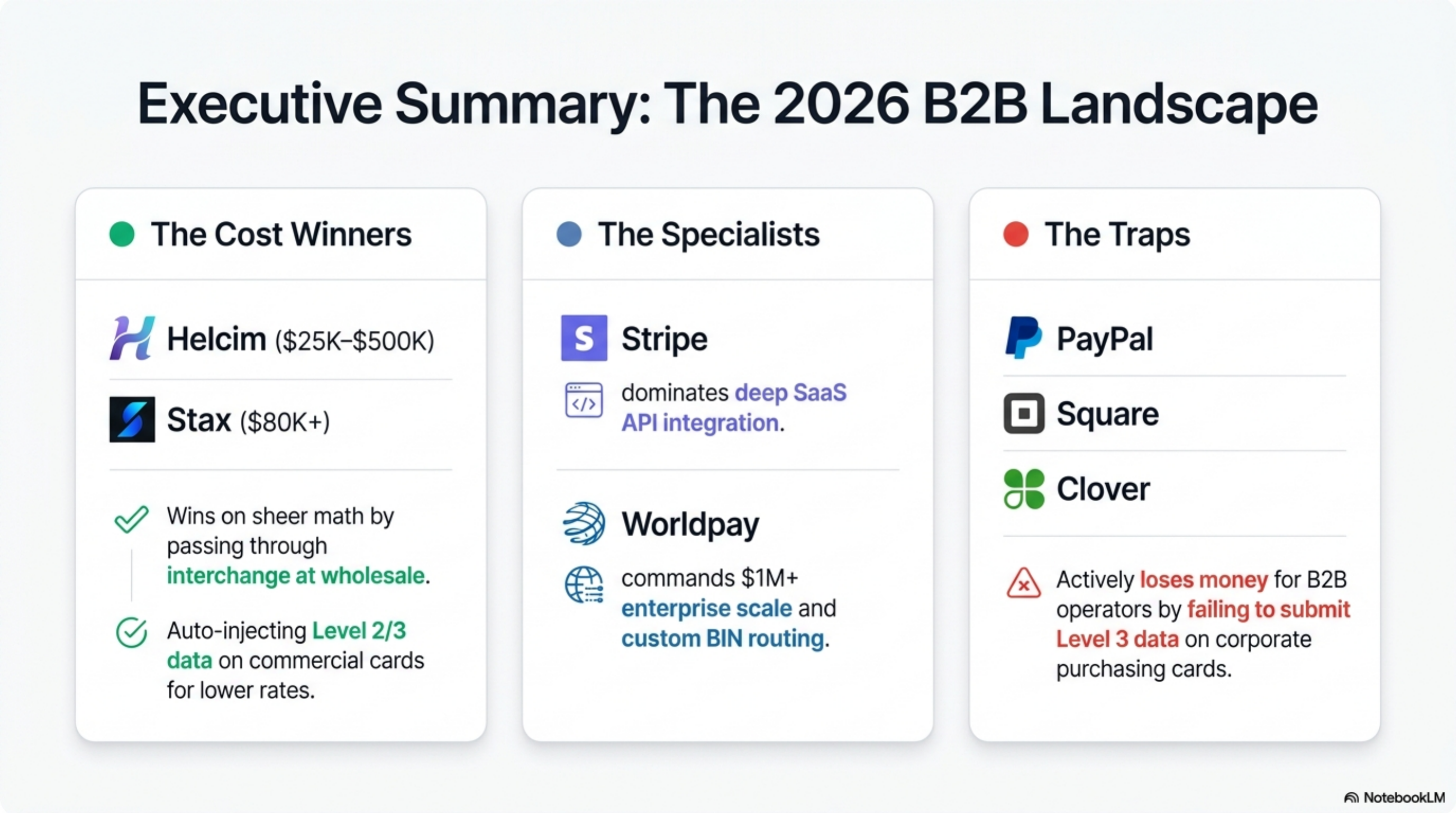

TL;DR

For B2B card acceptance from $25K to $5M monthly volume, Helcim and Stax win on cost because both pass interchange through and submit Level 2 and Level 3 data on commercial cards, which can shave 70 to 100 basis points off the qualifying interchange rate. Stripe wins on API depth for SaaS billing. Worldpay wins on six-figure tickets with custom routing. Square, PayPal, and Clover do not submit Level 3 data and lose money for any B2B operator running corporate or purchasing cards.

How we ranked

B2B card acceptance is not the same problem as B2C. Average tickets run higher, corporate and purchasing cards make up a bigger share of the mix, and the interchange penalty for missing line-item data is steep. We weighted six criteria:

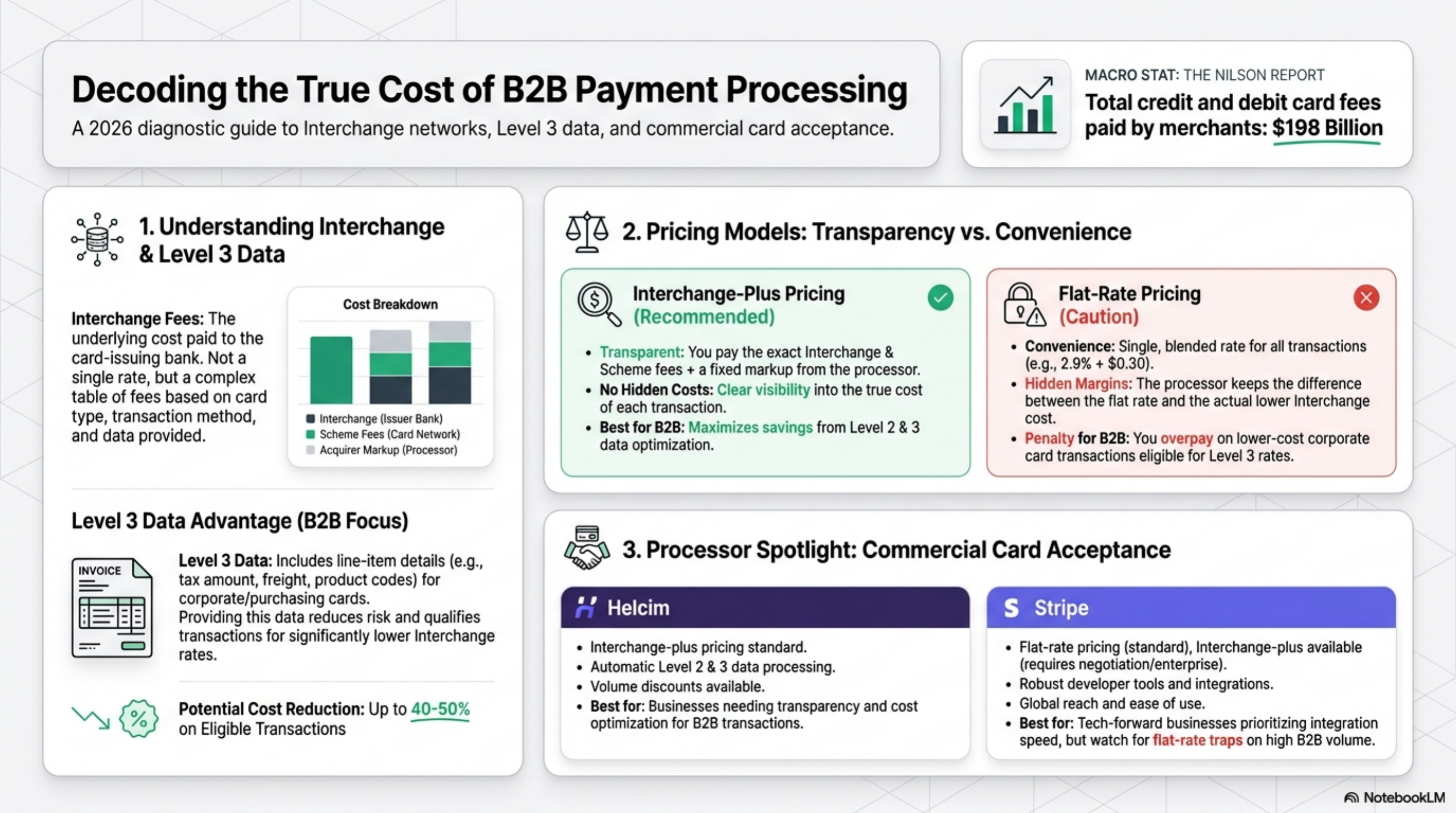

- Pricing model. Interchange-plus required. Flat-rate processors hide the markup and overcharge on premium commercial cards.

- Level 2 and Level 3 data. Automatic submission on supported commercial BINs is mandatory. Manual upload disqualifies.

- Commercial card rates. What the processor charges above interchange on Visa Business, Mastercard Corporate, and Amex OptBlue.

- Invoicing and ACH. Hosted invoice pages, recurring billing, ACH at 0.5 to 1 percent or capped.

- Contract terms. Month-to-month preferred. An ETF above $295 is a disqualifier.

- Settlement. Funding inside 2 business days on standard rails.

Commercial card interchange numbers come from published Visa interchange schedules and Mastercard interchange tables. Provider pricing comes from each company's public pricing page.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Helcim | IC + 0.40 to 0.50% + $0.08 to $0.25 | Month-to-month | 2 business days | $25K to $500K B2B volume | No same-day funding |

| Stax | $99/mo + IC + $0.08 to $0.18 | Month-to-month after initial term | 1 to 2 days | $80K+ B2B with steady mix | Subscription only pays off above ~$80K |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 | Month-to-month | 1 to 2 days | $50K to $250K B2B | Confirm L2/L3 routing on your plan |

| Stripe | 2.9% + $0.30 online standard | None | 2 days | SaaS, recurring B2B billing | Flat-rate markup at scale |

| Worldpay | IC-plus, custom (contact sales) | 1 to 3 year | 1 day | $1M+ B2B with large tickets | Long onboarding, custom contract terms |

| PayPal | 2.59% to 3.49% + $0.49 | None | 1 day | Sub-$25K invoicing | No L2/L3, expensive on commercial cards |

Helcim

Helcim publishes interchange-plus rates with no monthly fee and applies automatic volume discounts as merchants cross tiers. Card-not-present pricing is interchange plus 0.50 percent plus $0.25; in-person is interchange plus 0.40 percent plus $0.08, per Helcim's pricing page. The markup compresses at higher volume, which matters for B2B operators above $100K monthly.

The B2B-relevant feature is automatic Level 2 and Level 3 data submission on commercial card BINs. On a $5,000 Visa Corporate ticket, qualifying for L3 can drop interchange from roughly 2.65 percent to 1.90 percent, depending on category and ticket size, per Visa's published commercial interchange schedule.

Contracts are month-to-month with no ETF. Settlement runs 2 business days. Helcim's hosted invoice and recurring billing tools handle AR for teams that do not want a separate billing platform.

Who it's for: B2B sellers from $25K to $500K monthly with a mix of consumer and commercial cards.

Who should avoid it: operators above $1M monthly that need BIN-level routing or named account management.

Stax

Stax sells subscription pricing: a flat monthly fee plus interchange plus a per-transaction cost, with zero percentage markup. Per Stax's pricing page, the membership starts at $99 per month, with per-transaction costs of $0.08 in-person and $0.18 card-not-present on top of interchange.

The math only works above a break-even point. At $80K monthly volume on a typical B2B mix, the subscription replaces 30 to 50 basis points of percentage markup that an interchange-plus processor would charge, which usually beats the $1,188 annual fee. Below $50K, the subscription does not earn back the spread.

Stax submits Level 2 and Level 3 data on supported corporate and purchasing card BINs. On a $1,000 average ticket with 40 percent commercial card volume, L3 routing typically saves 40 to 60 basis points of blended interchange, per the Mastercard commercial interchange rate tables.

Contracts are month-to-month after the initial term. Settlement runs 1 to 2 business days.

Who it's for: B2B operators $80K monthly and up with stable volume.

Who should avoid it: seasonal businesses or merchants under $50K monthly, where the membership fee outruns the savings.

Payment Depot

Payment Depot uses the same wholesale membership model as Stax. Plans range from $79 to $199 per month with per-transaction fees of $0.05 to $0.15 on top of interchange, per Payment Depot's public pricing. Higher tiers earn lower per-transaction fees, so the right plan depends on transaction count, not just volume.

Level 2 and Level 3 data submission is supported on commercial cards, though routing automation depends on the gateway. Operators should confirm before signing that their gateway submits the line-item fields required for L3 qualification. Interchange savings on a $2,500 Visa Business ticket can run 75 to 100 basis points when L3 fires correctly.

Contracts are month-to-month with no early termination fee on most plans. Settlement is 1 to 2 business days. Phone support is U.S.-based, Monday through Friday.

Who it's for: B2B merchants $50K to $250K monthly looking for transparent wholesale pricing without a long contract.

Who should avoid it: operators needing 24/7 support or same-day funding.

Stripe

Stripe lists 2.9 percent plus $0.30 for online card transactions and 2.7 percent plus $0.05 for in-person on the standard plan, per its pricing page. Stripe added Level 2 and Level 3 data support for commercial cards in its API; merchants must pass the required fields in the PaymentIntent or InvoiceItem for the transaction to qualify.

The flat-rate model is the friction. On a B2B mix heavy in commercial cards, 2.9 percent already exceeds interchange plus 0.40 percent that Helcim or Stax would charge. At $250K monthly volume, the gap runs 50 to 80 basis points, which is $1,250 to $2,000 per month or $15K to $24K per year.

Stripe offsets that with the strongest B2B tooling on this list: subscription billing, dunning, tax automation via Stripe Tax, hosted invoicing with ACH, multi-currency settlement, and a developer ecosystem no competitor matches. For a SaaS company billing 5,000 small ARR contracts per month, the engineering savings outweigh the markup.

Contracts are month-to-month.

Who it's for: SaaS, marketplaces, and B2B software where billing complexity drives the choice.

Who should avoid it: B2B merchants with stable volume above $150K monthly that take cards via terminal or a basic invoice flow.

Worldpay

Worldpay is the enterprise option. There is no public flat rate; pricing is interchange-plus and negotiated per merchant, per its public site. According to the Nilson Report, Worldpay ranks among the top U.S. merchant acquirers by purchase volume and routinely processes seven-figure single tickets.

For B2B operators above $1M monthly, Worldpay's strengths are custom interchange-plus markups in the 5 to 15 basis point range, full L2 and L3 automation, BIN-level routing to optimize commercial card cost, and a dedicated account manager who handles chargeback escalations. Settlement can run T+1 on negotiated agreements.

The tradeoffs are contract length and onboarding friction. Standard agreements run 1 to 3 years with early termination fees that can reach four figures. Underwriting takes 7 to 14 days. Pricing is opaque without an active sales conversation.

Who it's for: B2B merchants above $1M monthly with large tickets and commercial-card-heavy mix.

Who should avoid it: anyone under $250K monthly. The contract overhead is not worth it.

PayPal

PayPal is on this list as a counter-example. The PayPal Business standard card rate is 3.49 percent plus $0.49 for keyed and PayPal Checkout transactions; the Advanced Credit and Debit Card rate is 2.59 percent plus $0.49, per the PayPal fee schedule.

For B2B, the math gets worse. PayPal does not submit Level 2 or Level 3 data on commercial card transactions through standard PayPal Business or PayPal Checkout. Every Visa Business, Mastercard Corporate, or Amex commercial card runs at the standard non-qualified interchange tier, which adds 70 to 100 basis points of cost the merchant cannot recover. On $250K B2B monthly volume with 40 percent commercial card mix, that is roughly $700 to $1,000 per month in interchange overpayment on top of PayPal's 2.59 to 3.49 percent markup.

The one B2B use case where PayPal still earns its place: invoicing for low-volume operators who want consumer trust at checkout and do not run enough commercial card volume to justify a B2B-grade processor.

Who it's for: under $25K monthly B2B with mostly consumer-card buyers.

Who should avoid it: anyone running a meaningful share of commercial cards.

Verdict

For B2B merchants in the $25K to $500K monthly volume range, Helcim is the default choice. Interchange-plus pricing, automatic Level 2 and Level 3 data on commercial cards, no monthly fee, and month-to-month contracts add up to the lowest effective rate without long-term lock-in. The savings versus a flat-rate processor like Stripe or PayPal can clear $20K per year at $250K monthly volume, per published Visa commercial interchange tables and each processor's posted rates.

Above $80K with stable volume and a commercial-card-heavy mix, Stax's subscription model wins by stripping percentage markup entirely. Above $1M monthly with large tickets, Worldpay's custom pricing and BIN routing pay back the contract overhead. Stripe wins only when developer time and billing complexity outweigh the markup. PayPal, Square, and Clover are not B2B tools and should not anchor a B2B card acceptance strategy.