TL;DR

Helcim is the strongest fit for most U.S. law firms processing $25K to $500K in monthly card volume. Its interchange-plus pricing runs about 0.40 to 0.70 percent under flat-rate processors on a typical legal card mix, with no contract and no monthly fee. Stripe wins for firms billing through Clio, MyCase, PracticePanther, or a custom client portal because the API support is deeper. Stax fits above $80K monthly volume, where its $99 subscription dilutes to under 0.15 percent.

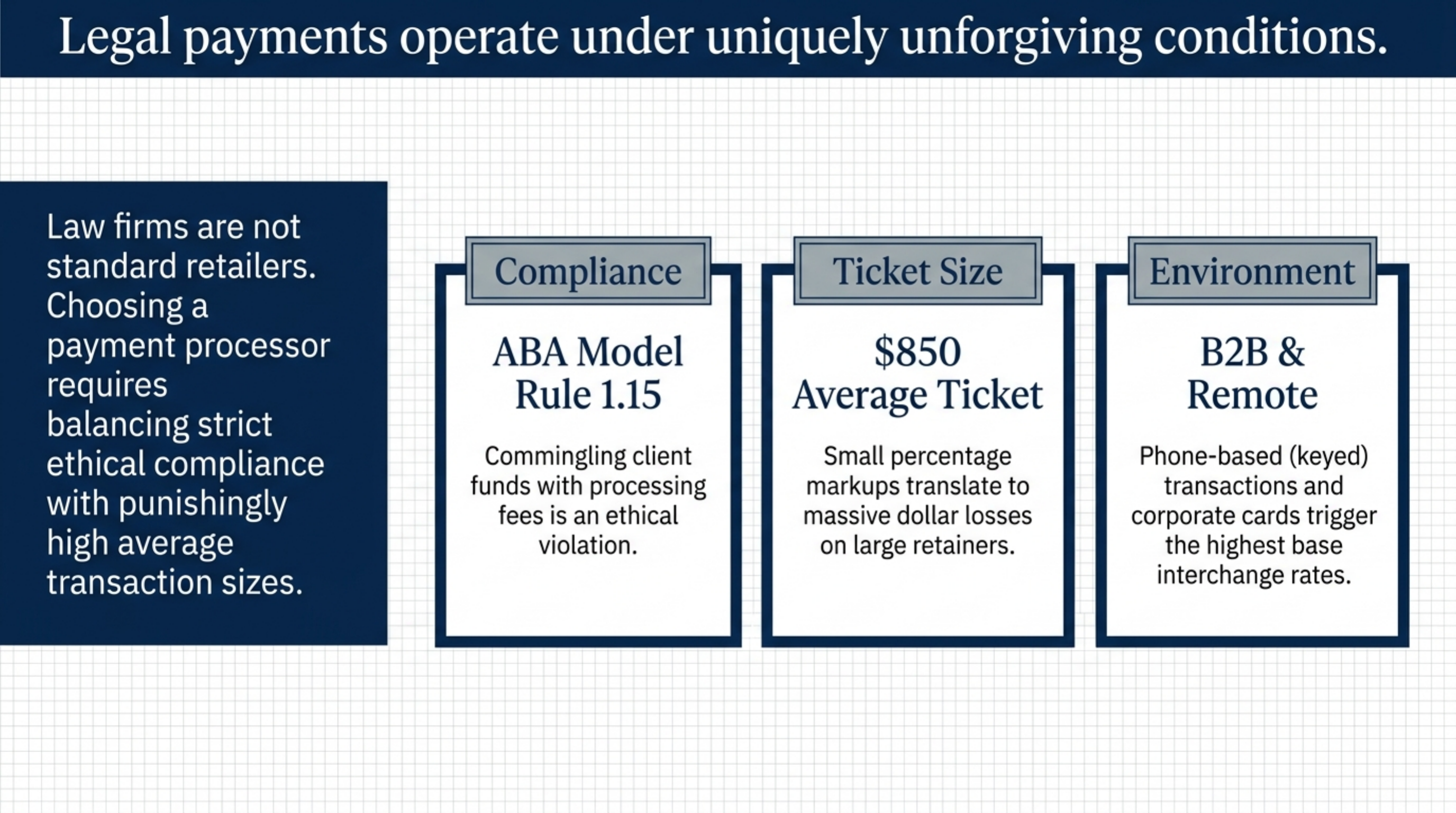

How we ranked

We weighted six criteria against a reference law firm: 40 percent corporate card mix, 50 percent consumer credit, 10 percent debit, average ticket $850, monthly volume from $25K to $400K. Card mix data is consistent with the Federal Reserve Payments Study for professional services.

- Effective rate at $100K and $250K monthly volume. Calculated from posted interchange tables and each provider's published markup.

- Contract terms. Month-to-month preferred. Any termination fee over $250 was penalized.

- IOLTA configurability. Whether the processor can deposit gross transaction amounts to a trust account while pulling fees from an operating account. This is a hard requirement under ABA Model Rule 1.15 and most state bar rules.

- Recurring billing and retainer support. ACH, card on file, automatic invoicing for evergreen retainers.

- Practice management integration. Native plug-ins with Clio, MyCase, PracticePanther, Smokeball.

- Settlement speed. Funds in the operating account inside 2 business days.

Interchange ranges come from Visa and Mastercard published schedules. Provider pricing is current as of June 2026.

A firm doing $250K in monthly card volume on a 70 percent consumer credit mix pays roughly $5,750 on Helcim's interchange-plus rails. The same volume on Stripe's flat 2.9 percent plus $0.30 runs $7,300 to $7,500. The annual difference clears $18,000.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Helcim | IC + 0.50% + $0.25 online; IC + 0.40% + $0.08 in person | None | 2 days | Solo and small firms billing $25K to $500K/mo | No 24/7 phone support |

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in person | None | 2 days | Firms on Clio, MyCase, or custom portals | Flat rate is expensive above $80K/mo |

| Stax | $99/mo + IC + $0.18 online; $0.08 in person | Month-to-month | 2 days | Firms above $80K/mo on premium card mix | Subscription wastes money below $50K/mo |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 per txn | Annual | 2 days | Firms above $50K/mo with steady volume | Membership wastes money in slow months |

| Square | 2.6% + $0.10 in person; 2.9% + $0.30 online; 3.5% + $0.15 keyed | None | 1 day | Solo practitioners under $20K/mo | Account holds; keyed rate punishes phone retainers |

| PayPal | Standard 3.49% + $0.49; Advanced 2.59% + $0.49 | None | 1 day | Consumer-facing firms accepting wallet payments | $0.49 fixed fee hurts small invoices |

Helcim

Helcim's pricing is interchange-plus with no monthly fee and no contract. Online transactions run interchange plus 0.50 percent plus $0.25. In-person runs interchange plus 0.40 percent plus $0.08. The markup steps down automatically as monthly volume crosses published thresholds, with no negotiation required. See Helcim's pricing page.

For a firm doing $150K in card volume on a 70 percent consumer credit mix, the all-in effective rate lands around 2.30 to 2.45 percent. That is roughly 0.45 to 0.60 percent below Stripe's flat 2.9 percent, or about $750 in monthly savings.

Helcim supports recurring billing, card on file, and ACH at $0.50 per transaction. It integrates with Clio through a third-party connector and with QuickBooks natively. ACH support matters for retainers above $1,000, where the percentage delta over card pricing dwarfs the integration trade-offs.

The IOLTA workflow requires opening two Helcim merchant accounts: one tied to the trust DDA receiving gross deposits, one tied to the operating DDA from which fees and chargebacks are drawn. Helcim will not net fees from a trust deposit; you have to configure the routing yourself.

Who it is for: solo and small to midsize firms that bill flat fees and want predictable, transparent costs.

Who should avoid it: firms that need a dedicated account manager or 24/7 phone support.

Stripe

Stripe charges 2.9 percent plus $0.30 for online card payments and 2.7 percent plus $0.05 in person on the default flat-rate plan. ACH is 0.8 percent capped at $5.00. Pricing is published at stripe.com/pricing.

Stripe's edge for law firms is the API. Clio Payments, MyCase Payments, and PracticePanther Payments all run on Stripe Connect rails underneath. If your firm has a custom intake form or a client portal built in-house, Stripe is the path of least resistance.

The cost trade is real. At $150K monthly card volume on a consumer credit heavy mix, Stripe's flat 2.9 percent runs roughly 0.50 percent above true interchange-plus. That is around $750 to $900 a month leaving the operating account.

IOLTA is supported only through Stripe Connect or by configuring two separate Stripe accounts. Stripe will not deposit gross to one bank and net fees from another inside a single account. Most law firms running on Clio Payments or MyCase Payments get this configuration through the practice management vendor, not Stripe directly.

Who it is for: firms with a developer on staff, or firms on a practice management platform built on Stripe.

Who should avoid it: firms above $80K monthly volume with no technical bandwidth and no need for the API.

Stax

Stax charges a $99 monthly subscription, then passes interchange through with no percentage markup. Per-transaction surcharges are $0.08 in person and $0.18 online. Plan details live at staxpayments.com/pricing.

The subscription model favors firms whose card volume is high enough to dilute the $99 fee below the percentage markup a flat-rate processor would charge. The math: $99 divided by $80K of monthly volume is 0.12 percent. Add the $0.18 per-transaction surcharge on a $1,000 average ticket and Stax's effective rate at $80K lands near interchange plus 0.14 percent. That undercuts Helcim by roughly 0.36 percent at that volume.

Below about $50K monthly volume, the math reverses. The $99 fee dilutes to 0.20 percent or higher, and Helcim's lack of a base fee wins.

Stax integrates with QuickBooks and supports recurring billing natively. IOLTA support requires the same two-account setup Helcim uses, because Stax cannot net fees out of a trust deposit any more than Helcim or Stripe can.

Who it is for: established firms with $80K or more in steady monthly card volume, especially those processing high-ticket invoices.

Who should avoid it: solo and small practices with seasonal or unpredictable billing.

Payment Depot

Payment Depot is a membership-based processor owned by Stax. Plans range from $79 to $199 per month, with per-transaction surcharges of $0.05 to $0.15 layered on top of pure interchange. Pricing is at paymentdepot.com/pricing.

The model is identical to Stax: a subscription that replaces the percentage markup. The membership tier you pick should match your transaction count, not your dollar volume. A firm doing 80 card transactions a month on a $1,800 average ticket is better off on the $79 plan than the $199 plan, even though the dollar volume might steer you toward the larger plan on the website.

Payment Depot's U.S.-based phone support is the real differentiator for law firms that do not want a chat-only relationship. Settlement is next business day on most plans.

The catch is the membership term. Payment Depot's standard agreement runs annually with renewal language in the terms. Read the cancellation clause before signing, because a misread can lock you into a second year at a rate that no longer reflects your volume.

Who it is for: firms above $50K monthly volume with predictable card counts and a preference for U.S. phone support.

Who should avoid it: firms with seasonal billing where a slow quarter wastes the membership fee.

Square

Square charges 2.6 percent plus $0.10 in person, 2.9 percent plus $0.30 online, and 3.5 percent plus $0.15 for keyed transactions. No monthly fee on the free plan. Pricing at squareup.com/us/en/pricing.

Square works for solo attorneys who take occasional in-person retainer payments at the courthouse or in a client meeting. The reader is free, settlement is next business day, and there is no contract. For a solo doing under $20K monthly card volume on a $400 average ticket, Square's 2.6 percent in-person rate is competitive because no monthly fee or subscription dilutes the cost.

The keyed rate of 3.5 percent plus $0.15 is the problem. Most law firm card payments are taken over the phone for retainers or invoice settlements, and those land in the keyed bucket. At that rate, a $2,500 retainer costs $87.65 in processing.

Square has a documented history of placing sudden holds on accounts when transaction patterns shift. For trust account funds, that risk is unacceptable. If you bill a $25,000 retainer on a Square account that has historically processed $3,000 invoices, expect the funds to sit in reserve while Square reviews.

Who it is for: solo practitioners under $20K monthly volume with mostly card-present transactions.

Who should avoid it: firms doing card-not-present retainers or any IOLTA funds.

PayPal

PayPal Standard charges 3.49 percent plus $0.49 for PayPal wallet transactions. The Advanced card processing rate is 2.59 percent plus $0.49 for direct card payments. In-person is 2.29 percent plus $0.09. See PayPal's business fees.

The $0.49 fixed fee is the issue for legal billing. On a $1,500 invoice, $0.49 is negligible. On a $75 filing-fee reimbursement, $0.49 plus 2.59 percent is 3.24 percent effective. Across an invoice ledger heavy with mixed small charges, the per-transaction fee adds 0.30 to 0.50 percent above what a $0.10 per-transaction processor would charge.

PayPal's strength is consumer trust. A meaningful share of consumer-facing solo and small firm clients prefer PayPal because they already have a wallet balance. For estate planning, family law, and immigration practices serving retail clients, accepting PayPal alongside a primary card processor is reasonable.

PayPal does not offer a native IOLTA configuration, and its dispute process is structured around consumer protection rather than B2B contract enforcement. For trust account billing, route through a primary processor and leave PayPal as a backup channel.

Who it is for: consumer-facing firms that want a second payment option for clients who request it.

Who should avoid it: B2B legal practices and firms billing large flat fees, where the fixed fee disappears but the dispute exposure stays.

Verdict

For a typical U.S. law firm processing $25K to $500K in monthly card volume, Helcim wins on cost and contract terms. Its interchange-plus markup saves 0.40 to 0.70 percent over flat-rate processors on a typical legal card mix, with no monthly fee and no termination clause.

Stripe wins for firms whose billing already runs through Clio, MyCase, PracticePanther, or a custom portal. The flat rate costs more, but the platform integration cost would consume the savings elsewhere.

Stax wins above $80K monthly volume on a high-ticket card mix, where its $99 subscription dilutes to under 0.15 percent of volume.

Whichever processor you pick, the IOLTA configuration matters more than the headline rate. Open two merchant accounts, route fees to the operating side, and confirm the setup in writing with your state bar's ethics opinion before sending the first invoice.