TL;DR

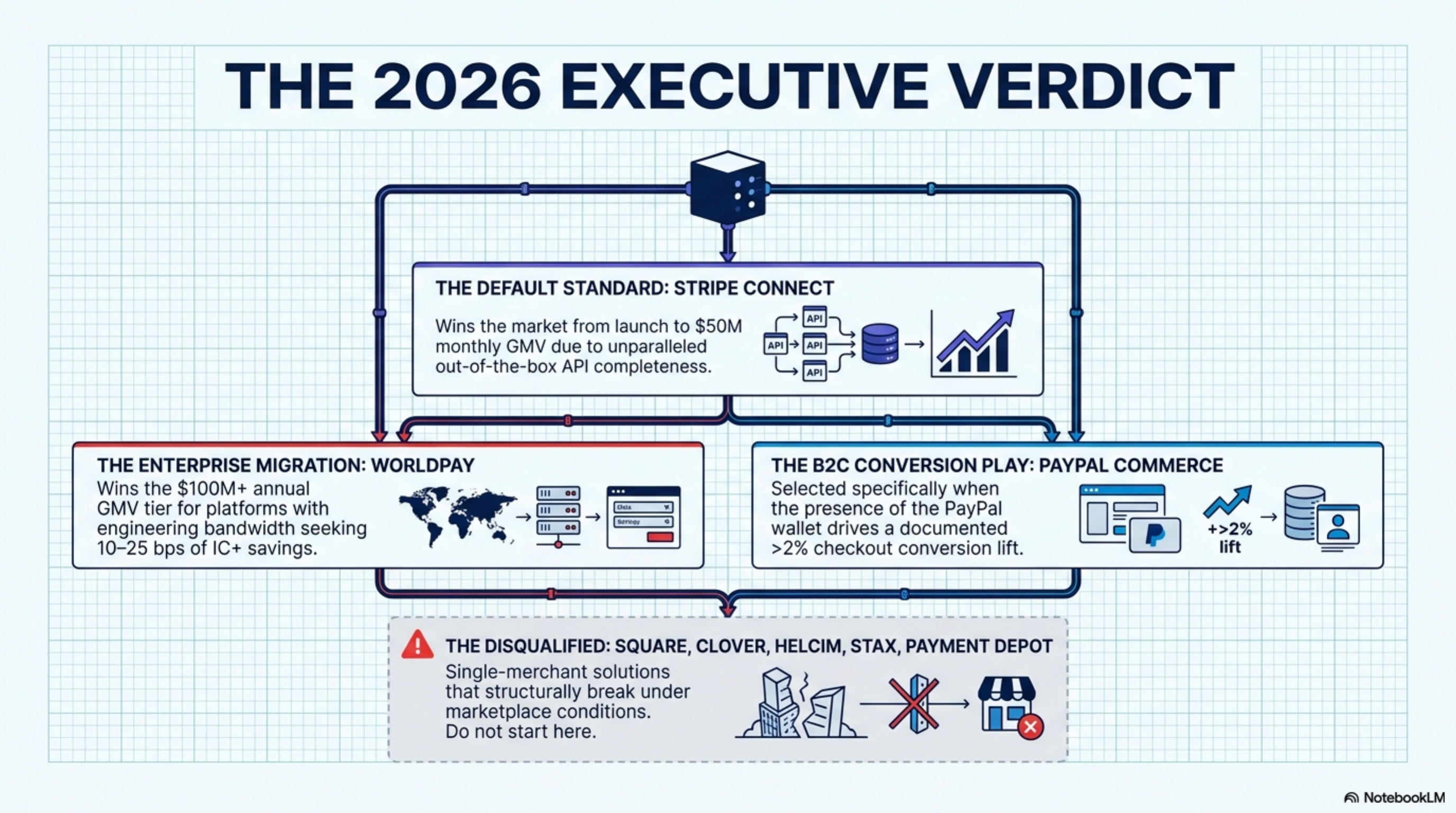

Stripe Connect is the default answer for marketplaces in 2026. It ships split payments, sub-merchant KYC, payouts in 135-plus currencies, and 1099-K filing in one API. PayPal Commerce Platform is the runner-up when buyer-side wallet conversion outweighs seller payout breadth. Worldpay fits enterprise marketplaces above $100M annual GMV with custom engineering. Square, Clover, Helcim, Stax, and Payment Depot are not built for the payment-facilitator model and should not be the first call for a true marketplace.

How we ranked

Marketplaces have a different fee math than single-merchant SaaS. The facilitator pays interchange on the buyer side, then pays out to sellers minus a commission. Six things drive total cost and risk:

- Split-payment and facilitator support. Can the processor route one buyer charge to many sellers in a single API call?

- Sub-merchant onboarding. KYC, OFAC screening, and beneficial ownership collection per Visa's payment facilitator program rules.

- Payout flexibility. Schedules, methods (ACH, instant, push-to-card), currency coverage, and 1099-K generation.

- Effective rate at $250K monthly GMV. Modeled on a card mix of 70 percent consumer credit, 20 percent debit, 10 percent rewards.

- Contract length and termination fees. Marketplaces grow or fail fast; multi-year deals with high ETFs are disqualifying.

- Risk and chargeback liability. Marketplaces inherit chargebacks from sellers and need a sub-merchant risk dashboard out of the box.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe Connect | 2.9% + $0.30 online, plus Connect fees from 0.25% + $0.25 per payout | Month-to-month | T+2 | Marketplaces $25K to $50M monthly GMV | Connect Custom adds 0.4% on volume |

| PayPal Commerce | 2.59% to 3.49% + $0.49 | Month-to-month | T+1 | B2C marketplaces with strong wallet conversion | Holds and reserves on new sellers |

| Worldpay | IC++ custom (Payrix for PayFac) | 3 years typical | T+1 | $100M+ GMV enterprise marketplaces | 7 to 14 day onboarding, ETF clauses |

| Helcim | IC + 0.50% + $0.25 online | Month-to-month | T+2 | Single-merchant SaaS, not marketplaces | No native sub-merchant API |

| Square | 2.9% + $0.30 online, 2.6% + $0.10 in-person | Month-to-month | T+1 | Small sellers using Square POS | Holds funds aggressively on facilitator-like flows |

| Stax | $99/mo + IC + $0.18 online | Month-to-month | T+2 | $50K+ direct merchants | No facilitator features |

| Payment Depot | $79 to $199/mo + IC | Month-to-month | T+2 | Direct merchants at $40K+ | No marketplace tooling |

| Clover | $14.95 to $54.95/mo + 2.3% to 2.6% + $0.10 in-person | Plan or hardware lease | T+1 | Brick-and-mortar SMB | Hardware lock-in, no facilitator API |

Stripe Connect

Stripe Connect is the only product on this list that was built from day one for marketplaces. Three modes (Standard, Express, Custom) let you choose how much of the seller experience you own. Express and Custom include hosted KYC, OFAC screening, beneficial ownership collection, and 1099-K filing for U.S. sellers above the IRS threshold. Payouts run in 135-plus currencies with same-day, next-day, or scheduled settlement.

Pricing on the buyer side starts at 2.9 percent + $0.30 online and 2.7 percent + $0.05 in-person per Stripe's published rates. Connect adds $2 per active connected account on Express plus 0.25 percent + $0.25 per payout, or a 0.4 percent volume fee plus per-payout charges on Custom.

Who it's for: any marketplace from launch to $50M monthly GMV. Who should skip it: pure B2B marketplaces above $100M annual volume where Worldpay's level 2/3 data support yields a cheaper interchange table.

PayPal Commerce Platform

PayPal Commerce Platform (built on the Braintree stack with Hyperwallet for payouts) is the only credible alternative to Stripe Connect for U.S. marketplaces. The pitch is buyer-side: PayPal Checkout is present on a meaningful share of U.S. consumer carts per the Nilson Report wallet share data, and B2C marketplaces in apparel, collectibles, and digital goods often see a conversion lift when the PayPal button is visible.

Pricing per PayPal's published rates runs 3.49 percent + $0.49 on standard credit and debit, 2.59 percent + $0.49 on Advanced Card, and 2.29 percent + $0.09 in-person. Hyperwallet payouts to sellers range from $0 to a few dollars per payout depending on method and country.

Who it's for: B2C marketplaces where the PayPal wallet at checkout drives a documented conversion lift of 2 percent or more. Who should skip it: B2B marketplaces and high-ticket categories.

Worldpay

Worldpay (now part of FIS, with a recent GTCR spinout) sells custom interchange-plus deals on its enterprise platform. There is no public flat rate; deals are quoted per merchant. For marketplaces, Worldpay's Payrix product provides payment-facilitator infrastructure including sub-merchant boarding APIs, split funding, and risk dashboards.

The catch: Worldpay onboarding takes 7 to 14 days, contracts are typically 3 years, and termination fees can run into five figures. The math only works for marketplaces above roughly $100M annual GMV, where 10 to 25 basis points of interchange-plus savings versus Stripe Connect cover the engineering cost of building seller-facing onboarding flows yourself.

Who it's for: marketplaces above $100M annual GMV with engineering bandwidth. Who should skip it: anyone under $100M, or any team that needs to ship in under 60 days.

Helcim

Helcim runs true interchange-plus pricing with no monthly fee and automatic volume discounts that begin at $25K monthly per its published rate card. Online transactions cost interchange plus 0.50 percent + $0.25 and in-person costs interchange plus 0.40 percent + $0.08.

For a single-merchant SaaS or direct-to-consumer e-commerce business, Helcim is one of the cleanest deals in the market. For marketplaces, the product is the wrong fit. Helcim does not offer a payment-facilitator API, sub-merchant onboarding flows, or split payments to multiple sellers. You can technically use Helcim under a master merchant account with manual payouts, but that pattern violates Visa and Mastercard rules for any seller above $1M annual volume per the Mastercard Payment Facilitator rules.

Who it's for: direct merchants from $25K to $1M monthly volume. Who should skip it: any business that needs to onboard third-party sellers and pay them a share of buyer charges.

Square

Square charges 2.6 percent + $0.10 in-person, 2.9 percent + $0.30 online, and 3.5 percent + $0.15 keyed per its public pricing page. The product is built for single-merchant retail and food service, with a free POS, free invoicing, and same-day deposits on paid plans.

Square does not run a payment-facilitator program in the way Stripe Connect does. Limited marketplace functionality exists through the Square API, but onboarding and payout to third-party sellers is not a first-class feature. Risk teams at Square hold funds aggressively when transaction patterns look facilitator-like, and account closures on flagged marketplace flows are a common pattern in operator forums.

Who it's for: brick-and-mortar retail, food service, and service businesses with one EIN. Who should skip it: any marketplace, multi-seller platform, or aggregator. Use Stripe Connect or PayPal Commerce instead.

Clover

Clover is a POS platform sold through Fiserv and a network of ISO resellers. Plans run $14.95 to $54.95 per month plus 2.3 to 2.6 percent + $0.10 in-person and 3.5 percent + $0.10 keyed per its public hardware pages. Effective rates vary widely because most Clover accounts are sold by ISOs who add their own markup on top of Fiserv's wholesale schedule.

Clover has no native facilitator API, no sub-merchant boarding flow, and hardware lock-in that makes switching processors painful even for direct merchants. The product is built for the corner store and the single-location restaurant.

Who it's for: brick-and-mortar SMB that wants a POS terminal and does not need payment platform flexibility. Who should skip it: every marketplace.

Stax

Stax (formerly Fattmerchant) sells subscription pricing at $99 per month plus interchange and per-transaction fees of $0.08 in-person and $0.18 online per its published pricing. For direct merchants above $50K monthly volume, the math beats flat-rate processors by 30 to 60 basis points.

Stax is not a payment facilitator. There is no sub-merchant API, no hosted seller onboarding, and no split-payment routing. The 24/7 phone and chat support is good for direct merchants but does not change the missing marketplace tooling.

Who it's for: direct merchants at $50K and above with steady volume. Who should skip it: marketplaces, low-volume merchants under $20K monthly (the $99 subscription kills the math), and anyone who needs facilitator-style infrastructure.

Payment Depot

Payment Depot, owned by Stax, sells wholesale interchange access for $79 to $199 per month plus interchange and $0.05 to $0.15 per transaction per its published rates. It is the cheapest published interchange-plus tier on this list for direct merchants.

Like Stax, Payment Depot is not a facilitator. There is no marketplace product. The membership model rewards predictable transaction volume; it does not solve sub-merchant onboarding, payouts, or 1099-K filing.

Who it's for: direct merchants at $40K to $500K monthly volume who want the lowest published interchange-plus rates. Who should skip it: marketplaces and any business that needs to pay third parties from card revenue.

Verdict

Stripe Connect wins for marketplaces from $25K to $50M monthly GMV. The combination of split-payment routing, sub-merchant onboarding with hosted KYC, payouts in 135-plus currencies, and 1099-K filing is the actual job description for any marketplace, and Stripe ships it as one API with month-to-month pricing. Above $100M annual GMV, the math changes: a custom Worldpay Payrix deal can shave 10 to 25 basis points versus Connect, but only if you have engineering bandwidth to build the seller experience yourself and you can tolerate a 7 to 14 day onboarding.

PayPal Commerce Platform is the right pick when your buyers convert measurably better with the PayPal wallet at checkout, which is most common in B2C apparel, collectibles, and digital goods. Square, Clover, Helcim, Stax, and Payment Depot are not marketplace products per the Federal Reserve's payments classifications. Do not start there.