TL;DR

For subscription products in 2026, Stripe is the default pick. Its 2.9 percent plus 30 cents base rate, Stripe Billing at a 0.5 percent add-on, and built-in account updater coverage make it the cleanest stack for SaaS, digital media, and DTC box brands. Helcim wins for U.S. and Canadian merchants between $50K and $250K monthly on interchange-plus pricing with no Billing surcharge. Stax wins above $80K monthly when a flat $99 membership beats a percentage markup. Square, PayPal, and Worldpay each fit narrower cases.

How we ranked

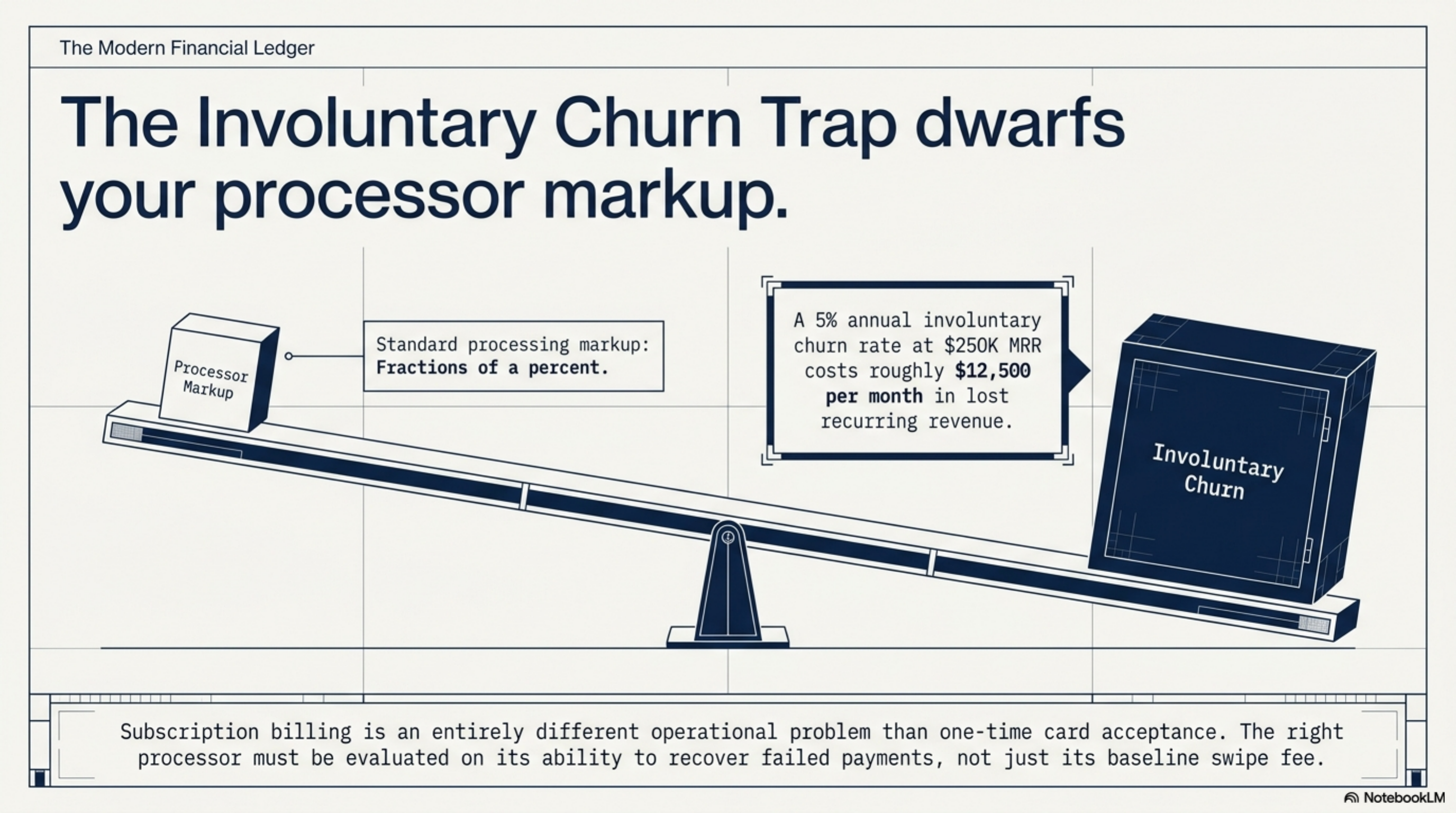

Subscription billing is a different problem than one-time card acceptance. A 5 percent annual involuntary churn rate at $250K MRR costs roughly $12,500 per month in lost recurring revenue, often larger than the processor markup itself. We weighted accordingly.

The six criteria:

- Effective rate at $250K monthly volume. All-in cost on card-not-present recurring transactions, including any Billing surcharge.

- Account updater coverage. Whether Visa Account Updater and Mastercard Automatic Billing Updater run automatically on cards on file.

- Dunning and retry logic. Smart retry windows, machine-learned retry timing, customer payment update flows.

- Contract length and ETF. Month-to-month wins. Multi-year deals with early termination fees lose.

- Settlement speed. T+2 or faster.

- 3DS and SCA support. Required for European card volume and for chargeback liability shift on U.S. issuers that opt in.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 plus 0.5% Billing | Month to month | T+2 | SaaS, DTC, global | Billing surcharge stacks on base |

| Helcim | IC + 0.50% + $0.25 online | Month to month | T+2 | $50K to $250K U.S. monthly | U.S. and Canada only |

| Stax | $99/mo + IC + $0.18 online | Month to month | T+2 | $80K+ monthly volume | Membership wasted below $80K |

| Square | 2.9% + $0.30 online | None | T+1 | Sub-$25K creators | Reserves on dispute spikes |

| PayPal | 3.49% + $0.49 standard | None | T+1 | Consumer trust at checkout | High per-transaction floor |

| Worldpay | Custom IC-plus | 3-year typical | T+1 | $1M+ monthly enterprise | ETF and 7 to 14 day onboarding |

Stripe

Stripe is the default subscription processor for product teams that ship code. Base card processing runs 2.9 percent plus 30 cents on U.S. cards, per Stripe's public pricing page. Stripe Billing, the recurring layer, adds 0.5 percent on the Starter plan or 0.8 percent on Scale, per the Billing pricing page. On $250K monthly subscription volume that adds $1,250 to $2,000 per month on top of base processing.

What the surcharge buys: smart retries, churn prevention, hosted invoice and checkout pages, proration logic, usage-based metering, Tax for sales tax compliance, and automatic enrollment in Visa Account Updater and Mastercard Automatic Billing Updater. Settlement is T+2 standard, faster on Stripe Instant Payouts at 1.5 percent.

Who it is for: SaaS and DTC subscription brands billing globally, or any team where engineering owns the billing stack.

Who should avoid it: U.S.-only merchants above $100K monthly who do not need Billing's product features. The Billing surcharge plus flat-rate base usually costs 0.6 to 1.0 percent more than Helcim or Stax at the same volume.

Helcim

Helcim runs interchange-plus pricing with no monthly fee and no Billing surcharge for recurring transactions. The online rate is interchange plus 0.50 percent plus 25 cents, per Helcim's published pricing. Volume discounts apply automatically as monthly processing grows, with the markup dropping further at the top tier.

Recurring Billing is included in the account at no extra subscription fee. The platform supports card vault, smart retries, customer-facing payment update pages, and one-click invoice payments. ACH is available at 0.5 percent capped at $6 per transaction, which often beats card economics on B2B subscription invoices above $400.

Who it is for: U.S. and Canadian subscription merchants doing $50K to $250K monthly. The effective rate typically runs 0.4 to 0.6 percent below Stripe with Billing at that volume.

Who should avoid it: Merchants with material non-U.S. and non-Canada card volume, or teams that need pre-built integrations with Salesforce, Recurly, or NetSuite. Helcim's developer ecosystem is thinner than Stripe's.

Stax

Stax charges a flat $99 to $199 per month plus interchange and a fixed per-transaction fee of 18 cents online, per Stax's pricing page. There is no percentage markup. Recurring billing, invoicing, and card vaulting are included.

The math works above roughly $80K monthly recurring volume. Below that, the membership is a tax. Above it, every additional dollar of volume costs only published interchange plus 18 cents, which compounds at $500K monthly: roughly 0.3 to 0.5 percent below Helcim and 0.7 to 1.0 percent below Stripe with Billing.

Who it is for: $80K+ monthly subscription merchants with predictable volume.

Who should avoid it: Sub-$50K monthly or seasonal merchants. The membership eats the savings.

Square

Square's online rate is 2.9 percent plus 30 cents, per Square's pricing page. Square Subscriptions, the recurring billing product, is included at no additional percentage surcharge on the free tier. T+1 settlement is the default. Square Instant Transfer pulls funds to a debit card for 1.75 percent.

The catch is account stability. Square uses an underwriting model built for low-risk retail, and subscription products with chargeback rates above 0.65 percent often trigger reserves or holds. Square's seller terms permit holds of up to 30 percent of incoming volume for up to 120 days on accounts flagged for risk.

Who it is for: Sub-$25K monthly subscription merchants, content creators, fitness studios using the Square ecosystem for in-person plus recurring.

Who should avoid it: High-ticket subscription boxes, B2B SaaS with custom invoicing needs, or any brand with elevated chargeback exposure. Holds at Square move from theoretical to operational quickly.

PayPal

PayPal's standard card rate is 3.49 percent plus 49 cents on PayPal-branded checkout, per the business fees page. The Advanced Credit and Debit Card rate is 2.59 percent plus 49 cents. Recurring Payments and Subscriptions APIs are included.

PayPal earns its spot on this list for one reason: brand recognition at checkout drives conversion. Nilson Report tracking on alternative payment methods shows wallet-branded buttons consistently lift DTC checkout conversion in the low single digits. For subscription brands where the marketing cost to acquire a customer runs $50 to $200, even a 1 to 2 percent conversion lift can outweigh the higher per-transaction rate.

Who it is for: DTC subscription brands offering PayPal as a secondary checkout option alongside Stripe or Helcim for direct card processing.

Who should avoid it: B2B subscription merchants with $5K+ average invoice sizes. The 49-cent floor is cheap; the 3.49 percent base on standard PayPal is the most expensive headline rate in this comparison.

Worldpay

Worldpay does not publish pricing. Plans are custom interchange-plus deals quoted by an account executive, with markup that depends on volume, vertical risk, and contract length. Worldpay's enterprise model is built for $1M+ monthly merchants with technical integration teams.

The platform supports recurring billing, tokenization, account updater, level 2 and level 3 data submission for B2B subscriptions, and global acquiring across more than 140 currencies. Settlement is typically T+1 on U.S. card volume. Contracts often run three years with early termination fees in the $295 to $495 range.

Who it is for: Enterprise subscription merchants above $1M monthly with dedicated payments engineering. Negotiated interchange-plus markup at scale can land at 0.10 to 0.25 percent, beating every other option on this list.

Who should avoid it: Anyone below $500K monthly. Onboarding takes 7 to 14 days, the ETF is real, and negotiated markup at lower volume is usually worse than Helcim's published rate.

Verdict

Stripe wins as the 2026 default for subscription products because it solves the engineering and reconciliation problems most merchants underestimate at the start: account updater enrollment, smart retries, proration, tax, and global card acceptance. The Billing surcharge is the price of not building these systems in-house.

Helcim is the pick for U.S. and Canadian merchants between $50K and $250K monthly who do not need Billing's product features. The interchange-plus pricing wins on cost. Stax takes the pick above $80K monthly when membership economics beat percentage markup. Worldpay enters the conversation above $1M monthly with dedicated payments engineering. PayPal is a checkout option, not a primary processor. Square is a low-volume answer for creators already inside its ecosystem. Run a statement comparison at six months in; the right answer at $40K monthly is rarely the right answer at $400K. Interchange data from the Federal Reserve payments studies, Visa, and Mastercard should drive the rerun, not vendor sales pitches.