TL;DR

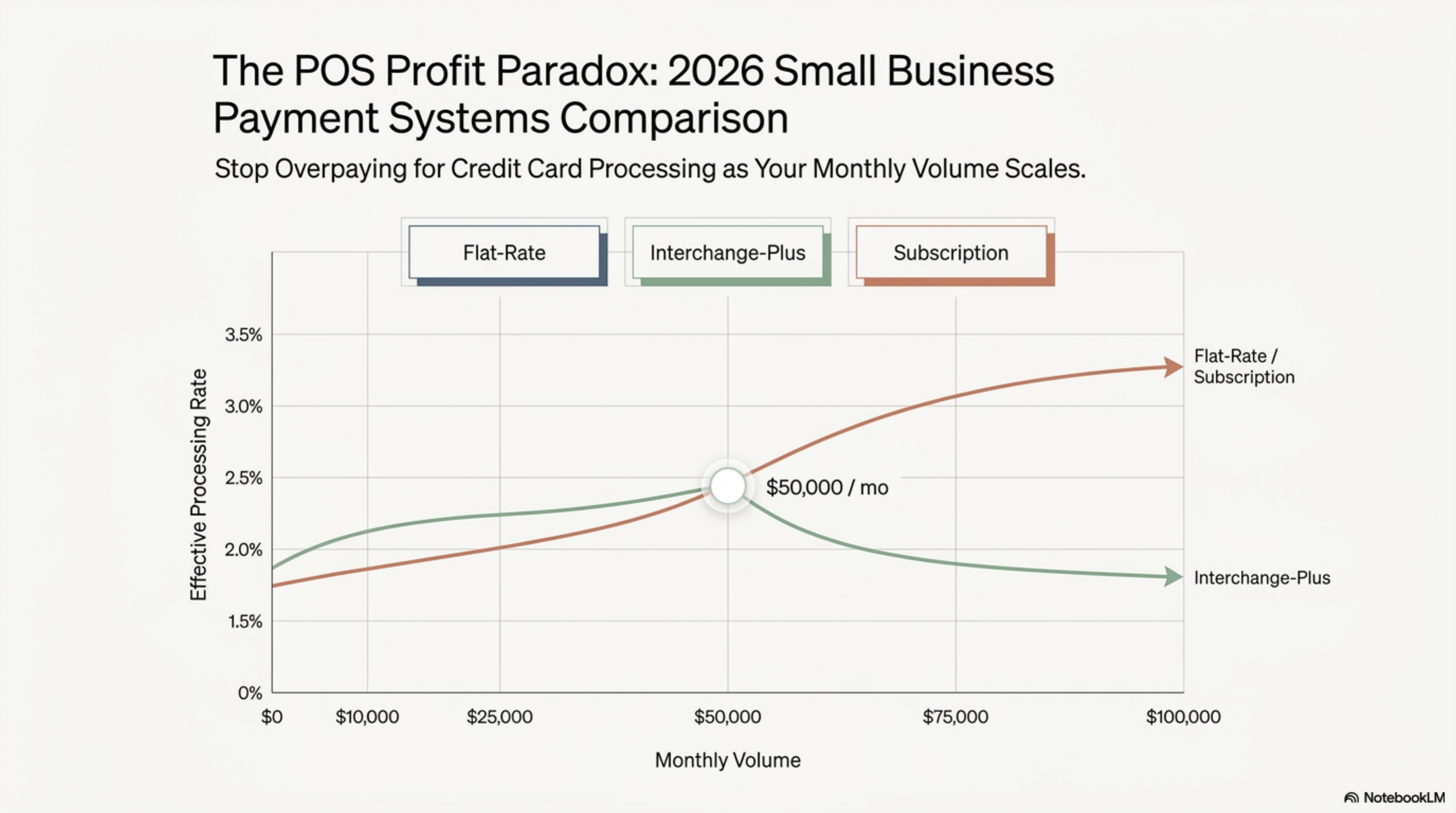

For most U.S. small businesses processing under $50K monthly card volume, Square wins on free software, transparent flat-rate pricing (2.6% + $0.10 in-person, per Square's pricing page), and same-day setup. Once monthly card volume crosses $50K, Helcim's interchange-plus model (IC + 0.40% + $0.08 in-person) saves more, and Stax's $99 subscription beats both above $80K. Clover wins for restaurants needing tableside hardware. Stripe remains the default for online-first businesses.

How we ranked

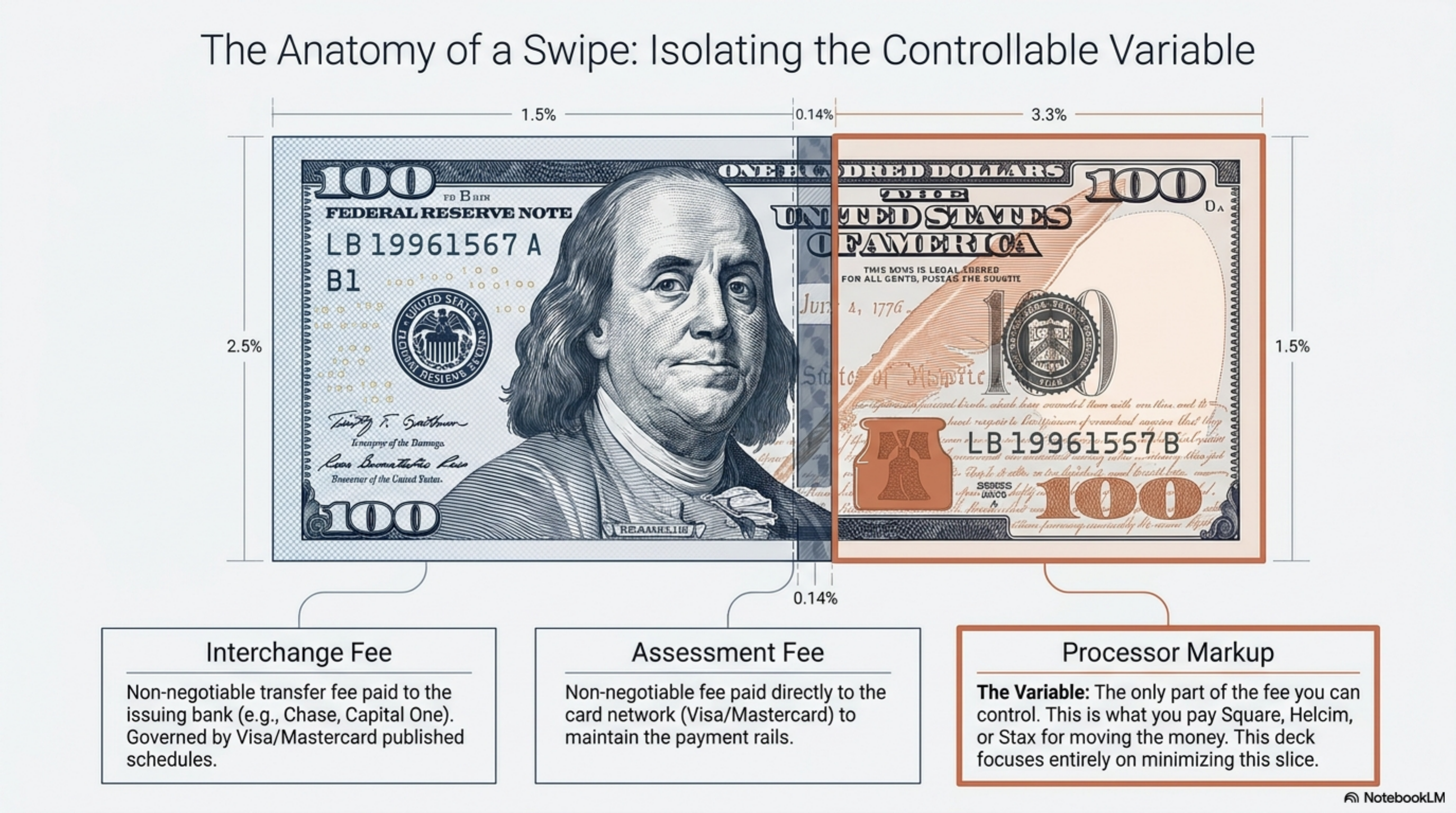

We weighted six factors against each provider's public pricing as of May 2026.

- Effective rate at $20K, $80K, and $250K monthly volume, modeled against a 70% credit / 30% debit mix using published Visa interchange schedules and Mastercard interchange rates.

- Contract length and early termination fees, since multi-year locks at small volume cost more than the headline rate savings.

- Hardware lock-in: whether terminals work only with the processor's gateway or accept standard EMV rails.

- Settlement speed to bank account, with one-business-day funding scored full marks.

- Level 2 and Level 3 data support for any B2B card-not-present volume.

- Dispute and chargeback workflow, since a single $400 friendly-fraud case eats six months of rate savings if the processor lacks a documented response path.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Square | 2.6% + $0.10 in-person | Month to month | Next day | Under $50K monthly | Account holds |

| Clover | $14.95 to $54.95/mo + 2.3% to 2.6% + $0.10 | Hardware lease 36 to 48 mo | Next day | Restaurants, retail | Hardware lock-in |

| Helcim | IC + 0.40% + $0.08 in-person | Month to month | 2 business days | $25K to $500K monthly | 2-day funding |

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in-person | Month to month | 2 business days | Online-first | Account reviews |

| Stax | $99/mo + IC + $0.08 in-person | Month to month after term | 2 business days | $80K+ monthly | Not worth under $50K |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 | Month to month membership | 2 business days | $40K to $200K monthly | PCI fees extra |

| PayPal | 3.49% + $0.49 standard; 2.29% + $0.09 in-person | Month to month | Same day to balance | Online sellers | Highest invoice rate |

Square

Square charges 2.6% + $0.10 per in-person card transaction, 2.9% + $0.30 for online checkout, and 3.5% + $0.15 for manually keyed transactions, per its published pricing. The basic POS software costs zero monthly. Square Reader hardware starts at $59 and Terminal at $299. Funding lands next business day standard, or same-day for a 1.75% instant-deposit fee.

Contract: month to month, no early termination fee.

Best for: retail, mobile services, food trucks, and pop-ups processing under $50K monthly. A coffee shop running $40K monthly at a 70% credit mix pays roughly 2.55% effective once the per-item fee is factored.

Clover

Clover plans run $14.95 to $54.95 per month across Starter, Standard, and Plus tiers, per the Clover POS page. In-person card rates run 2.3% to 2.6% + $0.10; keyed transactions are 3.5% + $0.10. Hardware ranges from the $49 Go reader to the $1,799 Station Duo.

Contract: hardware is frequently financed through Fiserv-affiliated ISOs on 36 or 48 month leases. Read who you sign with carefully, because the same Clover device sold through different resellers can carry different processing rates and PCI fees.

Best for: counter-service restaurants and small retail that want tableside ordering, kitchen printers, and built-in inventory without writing custom integrations. A Station 3 plus a Mini handheld covers most quick-service setups.

Helcim

Helcim publishes interchange-plus pricing of IC + 0.40% + $0.08 per in-person transaction and IC + 0.50% + $0.25 online, per the Helcim pricing page. Markup tiers down automatically as monthly volume grows: Helcim publishes nine bands from $0 to over $1M monthly, with the top tier dropping the in-person markup to 0.15%.

Contract: month to month, no statement fee, no PCI fee, no monthly minimum.

Best for: small business between $20K and $500K monthly card volume that wants the savings of interchange-plus without negotiating a contract. A retailer at $80K monthly running 65% credit typically sees a 0.30 to 0.45 percentage-point effective-rate drop vs. Square.

Stripe

Stripe charges 2.9% + $0.30 for online card payments and 2.7% + $0.05 for in-person (Terminal), per Stripe's pricing page. There is no monthly software fee on the standard plan. Custom interchange-plus pricing is available above roughly $80K monthly.

Contract: month to month. Standard two-business-day payout, with same-day available on Stripe Express at 1.5%.

Best for: small businesses with significant online or recurring revenue: SaaS, e-commerce, marketplaces, subscription boxes. The developer API quality remains the benchmark for engineering-led teams.

Watch out for: in-person POS hardware (Stripe Terminal) is best suited as part of an in-house build, not a turnkey countertop replacement. The Stripe Reader S700 requires custom app work to match what a Square Terminal does out of the box. Stripe is also active on account reviews; check the Restricted Businesses list before signing up for a vertical it flags.

Stax

Stax charges $99 per month for businesses under $250K annual volume, plus IC + $0.08 per in-person transaction and IC + $0.18 online, per the Stax pricing page. Above $250K annual, plans scale to $199 monthly. No per-transaction percentage markup is added on top of interchange.

Contract: month to month after the initial term. Cancellation requires written notice within the specified window; read the merchant agreement.

Best for: small businesses between $80K and $500K monthly volume with a high-ticket card mix. The flat $99 plus interchange beats Square's 2.6% above roughly $80K monthly.

Watch out for: under $50K monthly, the $99 fee outruns any interchange-plus savings. Start on Helcim or Square and migrate when the math flips.

Payment Depot

Payment Depot offers wholesale interchange pricing with monthly memberships of $79 to $199, plus a per-transaction surcharge of $0.05 to $0.15 depending on plan, per the Payment Depot pricing page. The model is similar to Stax: pay a flat monthly fee, then interchange plus a small per-item charge.

Contract: month to month for the membership; processor-side agreements may carry separate terms.

Best for: small businesses with predictable monthly volume above $40K who want lower fees than Stax's $99 entry tier. The $79 membership wins for mid-range volume; $199 only makes sense above $200K monthly.

Watch out for: hardware is sold separately and most terminals are EMV-standard. PCI compliance fees are not always included in the membership; ask for the full fee schedule in writing before signing.

PayPal

PayPal Standard charges 3.49% + $0.49 for invoiced and Pay-with-PayPal checkouts, 2.59% + $0.49 for advanced credit card processing, and 2.29% + $0.09 for Zettle in-person card transactions, per the PayPal business fees page.

Contract: month to month, no early termination fee. Funding lands in the PayPal balance the same day, with one to three business days to a linked bank account.

Best for: small online sellers who want PayPal-button checkout conversion lift without running a separate processor. The Zettle hardware works for occasional in-person sales (markets, events) but is not a full restaurant or retail POS.

Verdict

For most U.S. small businesses under $50K monthly card volume, Square is the right starting POS. Free software, no contract, transparent 2.6% + $0.10 in-person pricing, and same-day setup beat every alternative on time-to-revenue and total cost of ownership at low volume.

Once monthly card volume crosses $25K to $50K and stays there for three months, run the Helcim math. An interchange-plus drop of 0.30 to 0.45 percentage points usually clears $200 to $400 in monthly savings with no contract risk to switch.

Stax wins above $80K monthly when average ticket size is high enough that per-transaction fees dominate percentage markup. Clover wins when tableside restaurant hardware is required out of the box. For online-first or SaaS businesses, Stripe remains the default. PayPal earns inclusion only as a secondary checkout button, not as the primary processor. Federal Reserve payments data shows debit-heavy verticals widen the Square-vs-interchange-plus gap further.