TL;DR

For merchants under roughly $80,000 in monthly card volume, Helcim costs less because it charges no monthly fee and adds 0.40 percent plus 8 cents to interchange in-person. Payment Depot's membership model, $79 to $199 per month plus interchange and 5 to 15 cents per transaction, wins above $80,000 to $100,000 monthly volume, where the membership amortizes into a lower effective rate. Card mix and average ticket size shift the crossover up or down by 15 to 25 percent.

How we ranked

We compared Helcim and Payment Depot across six operator-level criteria, with effective cost weighted highest.

- Effective rate at $25,000, $100,000, and $250,000 monthly volume on a typical retail card mix.

- Contract structure: month-to-month flexibility, early termination fees, and renewal terms.

- Settlement speed and reserve requirements.

- Level 2 and level 3 data pass-through for B2B and government card acceptance.

- Hardware compatibility and cost of switching processors later.

- Dispute response SLA and chargeback handling.

Pricing inputs come from each processor's public pricing page. Interchange benchmarks come from the Visa and Mastercard published schedules (Visa, Mastercard). Industry transaction volume context comes from the Federal Reserve payments studies (Federal Reserve). We weighted effective cost at typical card mix more heavily than feature parity, because at this price tier both processors clear the basic functionality bar.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Helcim | IC + 0.40% + $0.08 in-person, IC + 0.50% + $0.25 online | Month-to-month, no ETF | 1 to 2 business days | Under $80K monthly volume, transparent pricing | No 24/7 phone support |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 per transaction | Month-to-month membership | 1 to 2 business days | Above $100K monthly volume with predictable ticket size | Membership fees still apply in slow months |

Helcim

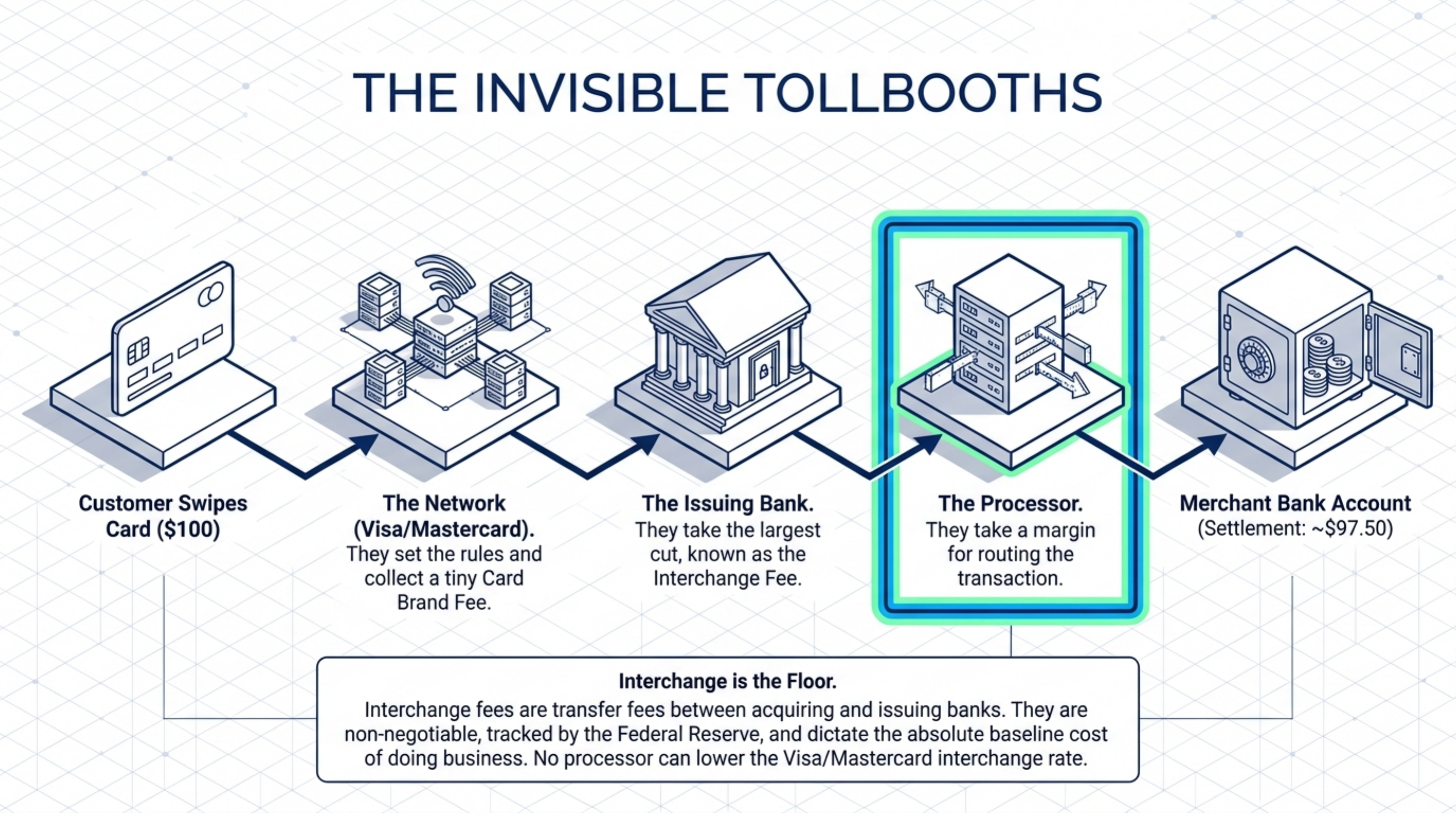

Helcim publishes interchange-plus pricing on its public site: 0.40 percent plus 8 cents added to interchange for in-person transactions, and 0.50 percent plus 25 cents added to interchange for online and keyed-in transactions (Helcim pricing). There is no monthly account fee, no statement fee, no PCI compliance fee, no setup fee, and no early termination fee on the standard merchant agreement.

Helcim applies automatic volume discounts. Once monthly volume crosses published tier thresholds, the markup percentage drops without a renegotiation. The discount applies starting the month after you cross the threshold and resets each month based on actual volume, so seasonal swings are reflected automatically rather than locked in for a year.

Helcim supports level 2 data on its standard plan and level 3 data on its hosted invoicing tools, which matters for B2B operators accepting commercial cards. Hardware is unlocked: terminals are available on month-to-month rental or one-time purchase, and there is no proprietary processing lock that prevents you from switching processors with the same device line.

Funding speed is typically 1 to 2 business days for U.S. accounts. Customer support runs phone, chat, and email during business hours; there is no 24/7 phone line. Chargeback handling follows the standard card network timelines, and the dispute portal accepts evidence uploads directly without a phone queue.

Who it fits: merchants under $80,000 monthly volume who want pricing transparency, no contract risk, and no surprise fees. Who should avoid it: very high-volume operators above $250,000 monthly where a pure subscription model amortizes more efficiently, and any merchant that needs 24/7 live phone support.

Payment Depot

Payment Depot uses a membership model with published plans ranging from $79 to $199 per month, depending on volume tier (Payment Depot pricing). Above the membership fee, merchants pay interchange plus a per-transaction fee between 5 cents and 15 cents, with no percentage markup added to interchange.

Payment Depot was acquired by Stax Payments in 2020 and now operates under the same parent company. The membership pricing structure remained in place after the acquisition, though backend processing and underwriting moved to the Stax platform. Membership plans are typically month-to-month with no early termination fee on the membership itself, though hardware financing agreements carry separate terms that survive plan cancellation.

Payment Depot supports level 2 and level 3 data on request, which can drop B2B interchange categories by 70 to 100 basis points on commercial cards. Hardware is sold or financed separately and is typically tied to the First Data, Clover, or Dejavoo terminal ecosystems, which carries some lock-in if you later move to a non-Fiserv platform.

Funding speed is 1 to 2 business days. Customer support is U.S.-based phone and email during business hours. Dispute handling runs through the Stax case-management portal, visible in the merchant dashboard. Reserves are uncommon at this tier, but high-risk verticals such as nutraceuticals or subscription billing may face holdback requirements during underwriting.

Who it fits: established merchants above $100,000 monthly volume with predictable transaction counts. Who should avoid it: seasonal businesses where slow months still owe the full membership, and low-ticket operators where the 10 to 15 cent per-transaction fee dominates the math.

Crossover math: which one is cheaper at your volume

The pricing decision usually comes down to one calculation: at what volume does Helcim's 0.40 percent in-person markup equal Payment Depot's membership fee divided by your transactions?

The break-even for the $99 Payment Depot plan against Helcim's 0.40 percent in-person rate sits where 0.40 percent of monthly volume equals $99 plus the per-transaction delta. At an average ticket of $75 and a 10-cent Payment Depot per-transaction fee versus Helcim's 8 cents, the crossover lands near $30,000 monthly volume on percentage alone. Once you factor in typical card mix and the $25 difference per 1,000 transactions on per-item fees, the practical crossover shifts higher, to roughly $75,000 to $90,000 monthly.

For online and keyed-in volume, Helcim's 0.50 percent plus 25 cents is heavier per transaction. Card-not-present merchants reach Payment Depot's break-even sooner, around $50,000 to $60,000 monthly volume, especially on lower average tickets where the 25-cent Helcim per-transaction fee compounds quickly.

Verdict

Helcim wins below $80,000 monthly volume on in-person retail and below $50,000 on card-not-present. The no-monthly-fee structure means slow months do not cost extra, and the automatic volume discount keeps pace as you grow without a renegotiation cycle.

Payment Depot wins above $100,000 monthly volume with predictable transaction counts and a stable average ticket. The membership fee gets diluted across enough transactions that the zero-percentage markup beats Helcim's 0.40 percent in-person blend. The crossover is sharper for retail with low average ticket sizes than for e-commerce with high average tickets, and sharper for B2B card-present than card-not-present.

If you are unsure which side of the crossover you fall on, run the math against three months of actual statements rather than projections. Both processors publish enough pricing to compute exact effective rates against your real card mix, transaction count, and average ticket. The Federal Reserve payments data is a useful reference for card-mix benchmarks if your statement does not break it out clearly.