TL;DR

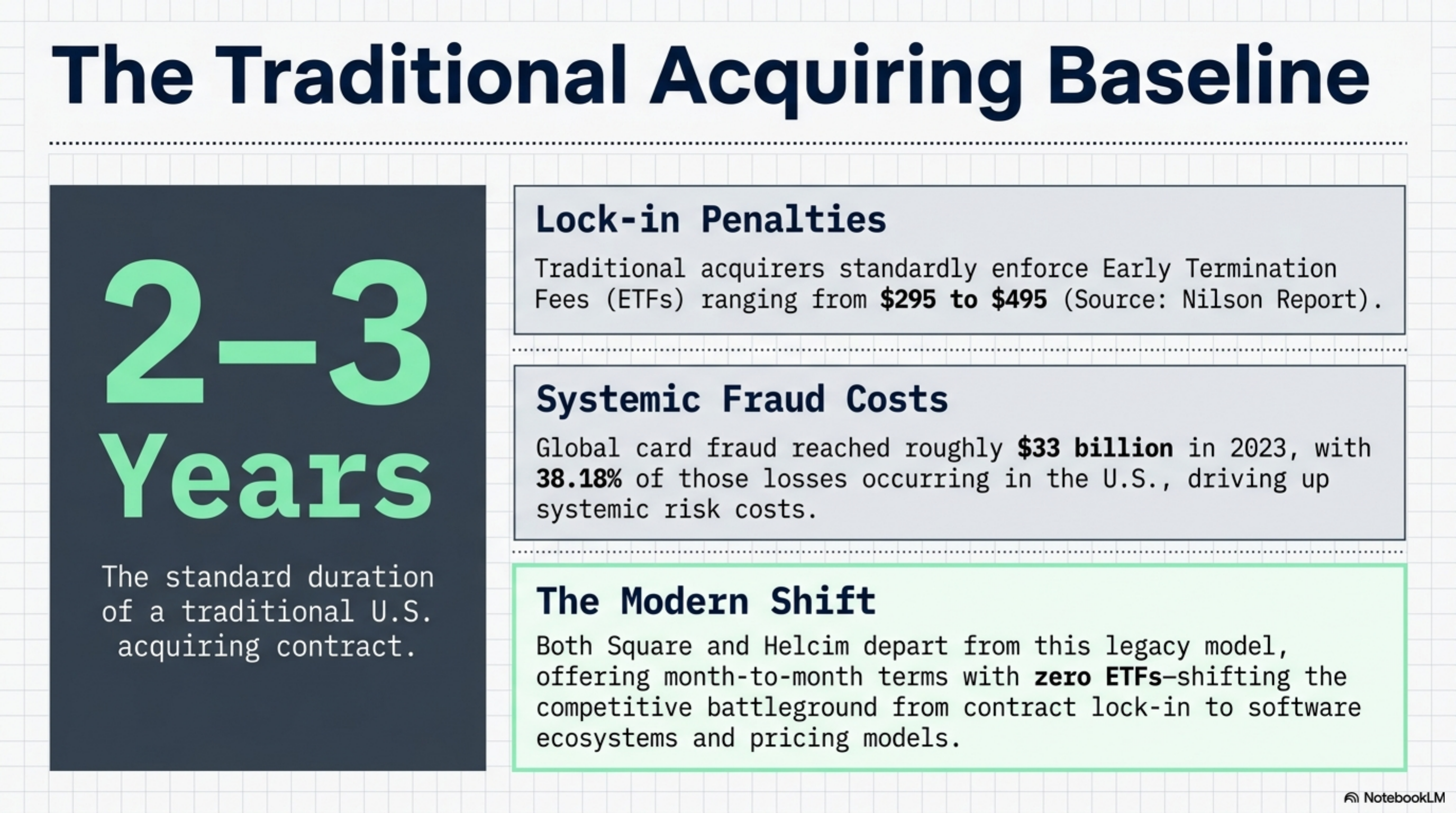

Verdict, May 2026: Helcim costs less than Square at every monthly volume above $10,000. Square charges a flat 2.6% + $0.10. Helcim's interchange-plus pricing (IC + 0.40% + $0.08 in-person) saves a retail merchant $90-$130 per $25K of volume. Barak Bachar verified the math.

How we ranked

Both providers publish full pricing online, so we ran them against the same merchant scenarios instead of taking marketing copy at face value. Six criteria, weighted in this order:

- Effective rate at $25K, $100K, and $500K monthly volume. Modeled on a typical retail card mix (75 percent Visa/Mastercard credit, 15 percent debit, 10 percent rewards or business cards) using Visa's published interchange schedule.

- Contract terms. Length, early termination fees, automatic renewal clauses.

- Settlement speed. How quickly funds hit your bank, and what the instant-deposit fee is.

- Hardware and platform lock-in. Whether you can switch processors and keep using the terminals.

- Level 2 and Level 3 data support. Critical for B2B or government cards, which can reduce interchange by 50 to 100 basis points.

- Dispute and chargeback handling. Response window, evidence portal, win-rate transparency.

Pricing data is pulled from each provider's public pages as of May 2026.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Square | 2.6% + $0.10 in-person, 2.9% + $0.30 online, 3.5% + $0.15 keyed | Month-to-month, no ETF | Next business day (free); instant for 1.75% | Sub-$10K monthly volume, single-location retail and food service | Flat rate gets expensive past $20K; reserve policy is uncapped |

| Helcim | IC + 0.40% + $0.08 in-person, IC + 0.50% + $0.25 online | Month-to-month, no ETF, no monthly fee | Two business days standard | $20K+ monthly volume, B2B, multi-location retail | No same-day settlement; smaller hardware catalog |

Square: flat-rate simplicity, baked-in margin

Square's published in-person rate is 2.6 percent plus 10 cents per tap, dip, or swipe. Online is 2.9 percent plus 30 cents, manually-keyed runs 3.5 percent plus 15 cents. No monthly fee on the free plan, no contract, no early termination fee.

What you give up for that simplicity is margin. Visa's published interchange for a CPS Retail credit transaction is roughly 1.51 percent plus 10 cents; Mastercard's Merit III credit category sits in the same range, per the Mastercard Interchange Rates and Criteria. Add scheme assessments of about 0.13 percent and true cost lands between 1.64 and 1.80 percent. Square's 2.6 percent leaves about 0.80 to 0.95 percent in markup on every credit transaction, regardless of your volume. The markup does not shrink as you grow.

Hardware is where Square pulls ahead. Square Reader is $49, Square Stand starts at $149, and the free POS app covers inventory, orders, employee logins, and basic reporting without an upgrade. Setup is genuinely same-day, and Square Banking settles next-business-day at no charge.

Who it fits: single-location retail, coffee shops, food trucks, weekend pop-ups, and any merchant under $10K monthly volume who values not reading statements over saving 40 basis points.

Who should avoid it: any merchant above $25K monthly volume, B2B vendors that accept purchasing cards, and any business whose card mix skews toward rewards or corporate cards (interchange of 2.4 percent vs. Square's flat 2.6 percent).

Helcim: interchange-plus that gets cheaper as you grow

Helcim's published in-person rate is interchange plus 0.40 percent plus 8 cents; online is interchange plus 0.50 percent plus 25 cents. No monthly fee, no statement fee, no setup fee, no early termination clause. Pricing tiers down automatically as monthly volume crosses $25K, $50K, $100K, and $250K.

On a typical retail card mix at $25K monthly volume, Helcim's effective rate lands around 2.18 to 2.25 percent plus $0.08. Square on the same mix is 2.60 percent plus $0.10. On 500 transactions per month, that is a $90 to $115 monthly delta in Helcim's favor, before Helcim's volume tier kicks in.

Helcim publishes its full interchange-plus markup schedule on the pricing page, which is unusual in U.S. acquiring; most processors keep it inside a sales rep's PDF. Statements show every interchange category, every assessment, and Helcim's exact margin. That transparency makes statement audits possible and quarterly renegotiation pointless.

Hardware is leaner: the Helcim Card Reader is $99, the Smart Terminal runs $329. The POS app, virtual terminal, hosted checkout pages, recurring billing, and ACH come bundled at no extra cost.

Who it fits: U.S. or Canadian merchants doing $20K+ monthly, B2B sellers (Level 2/3 data is automatic), and multi-location retail that wants one rate card across all stores.

Who should avoid it: merchants who need instant same-day funding, and micro-merchants under $5K monthly where the per-transaction 8 cents starts to dominate small-ticket math.

Effective rate at $25K, $100K, and $500K

The flat-rate vs. interchange-plus comparison only matters at the volume tier where you actually operate. Modeled on a retail mix (75 percent Visa/Mastercard credit, 15 percent debit, 10 percent rewards or business cards), with a $50 average ticket and Visa's published CPS Retail credit rate of 1.51 percent plus $0.10:

| Monthly volume | Square cost | Helcim cost | Delta per month | Delta per year |

|---|---|---|---|---|

| $25,000 (500 tx) | $700 | $590 | $110 | $1,320 |

| $100,000 (2,000 tx) | $2,800 | $2,360 | $440 | $5,280 |

| $500,000 (10,000 tx) | $14,000 | $11,300 | $2,700 | $32,400 |

The math flips below roughly $8,000 monthly volume. At that level the per-transaction 8 cents on Helcim, combined with the longer settlement window, makes Square's marginally higher rate worth it for cash-flow reasons.

Contracts, hardware, and lock-in

Both processors run month-to-month with zero early termination fee. That is rare in the U.S. acquiring market, where two- and three-year contracts with $295 to $495 ETFs remain standard, per Nilson Report coverage of merchant acquirer practices. On paper, walk-away friction is equally low at either.

Hardware lock-in is where they diverge. Square Readers, Stands, and Registers are gateway-locked to Square's processing. If you leave Square, the hardware is a $49 to $799 brick. Helcim sells its own Smart Terminal but also supports a broader list of bring-your-own-device options through its API and virtual terminal, which keeps the switching cost lower.

Account stability is the other lock-in to think about. Square's underwriting model leans heavily on machine review and is documented for placing holds on accounts flagged for chargebacks, sudden ticket size changes, or vertical risk. Funds held under review can take 30 to 120 days to release. Helcim underwrites manually before the account opens and holds funds mid-stream less often, but the trade-off is that Helcim is slower to onboard high-risk verticals (firearms, CBD, supplements, ticketing) and may decline them outright.

Verdict

Helcim wins for any merchant doing more than $20,000 in monthly card volume. Interchange-plus with a 0.40 percent in-person margin, no monthly fee, automatic volume discounts, and a fully published rate card make it the cheaper and more transparent option from $20K all the way through $5M monthly. The annual savings versus Square scale roughly linearly: $1,300 at $25K monthly, $5,300 at $100K, $32,400 at $500K.

Square wins in three narrower scenarios. First, true micro-merchants under $8K to $10K monthly volume, where Square's lower per-transaction fee and free first reader beat Helcim's flat 8 cents per transaction. Second, merchants who need same-day or instant deposit access for cash-flow reasons. Third, founders running a brand-new business who want to be live within an hour and have no patience for a manual underwriting call.