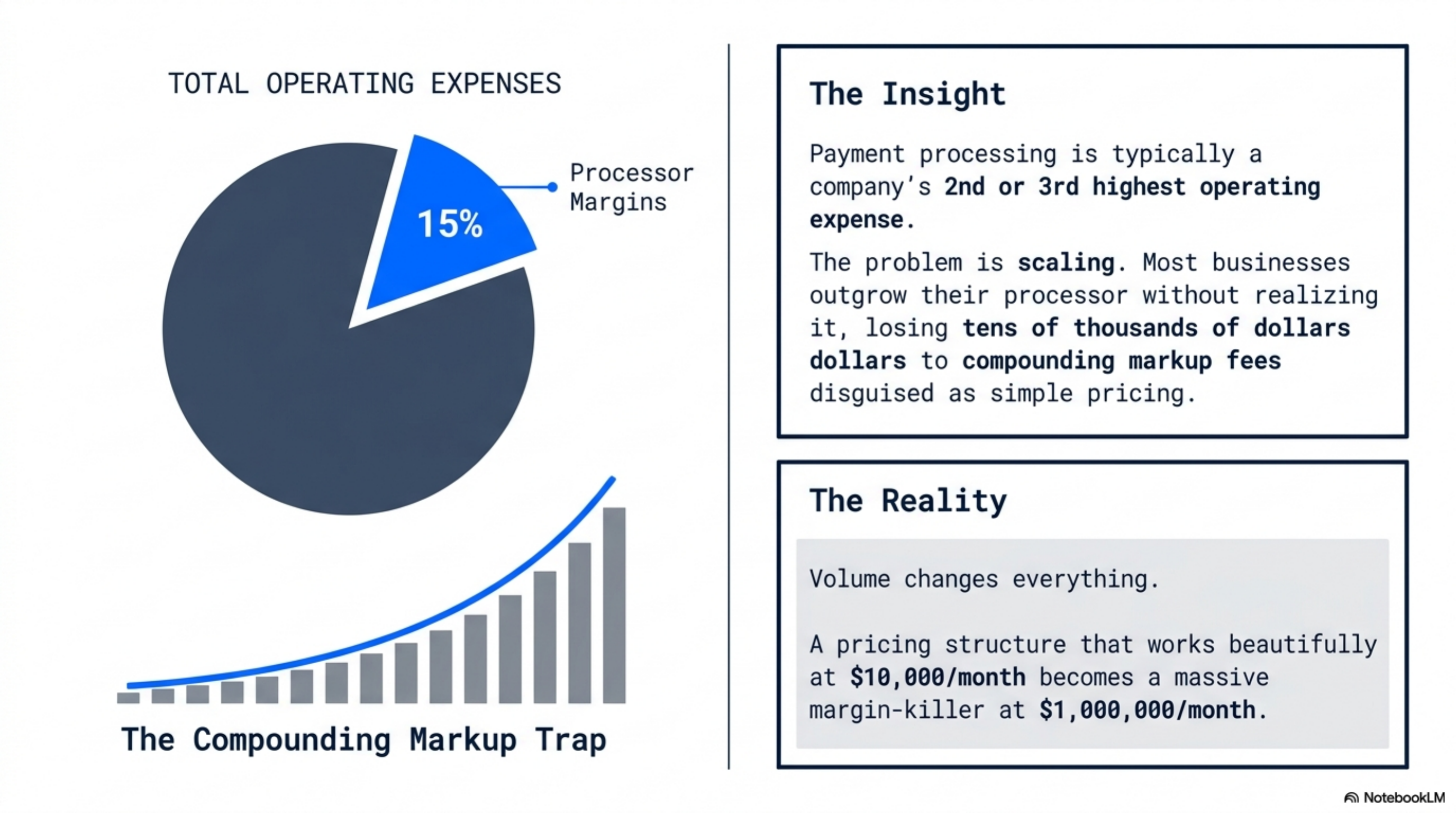

TL;DR

Stripe wins for U.S. merchants below $1M monthly card volume on standard online payments. The flat 2.9 percent plus $0.30 is simple, settlement is T+2, and there is no monthly minimum. Adyen wins above roughly $1M monthly volume, especially for cross-border merchants and high average-order-value businesses. Adyen's Interchange++ model with a fixed $0.13 processing fee per transaction beats Stripe's flat rate by 0.25 to 0.55 percent on effective rate at scale. The break-even sits around $750K to $1.2M monthly volume depending on card mix and ticket size.

How we ranked

We compared Stripe and Adyen using six weighted criteria, calibrated for U.S. merchants processing $100K to $5M monthly in card volume.

- Effective rate at $250K, $1M, and $3M monthly volume (40%): total processing cost using Visa's published interchange schedule and Mastercard's interchange rates and criteria, plus each processor's markup.

- Contract length, monthly minimums, and ETF (15%): month-to-month is worth more than a 36-month lock with an early-termination fee.

- Settlement speed (15%): T+1 beats T+2 beats weekly batch on working capital.

- Cross-border and multi-currency support (10%): relevant for marketplaces and global D2C.

- Level 2/3 data and B2B card support (10%): matters for merchants taking corporate cards.

- Dispute and chargeback workflow (10%): SLA, evidence templates, and reported win rates.

Per the Federal Reserve Payments Studies, average U.S. credit interchange sits near 1.8 percent of authorized volume. We treat that as the floor. The markup above floor is what we measure.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online, 2.7% + $0.05 in-person | Month to month, no minimum | T+2 | Sub-$1M monthly online merchants | Flat-rate markup compounds at scale |

| Adyen | Interchange + scheme + $0.13 per transaction | Month to month, ~$120 monthly invoice minimum | Weekly default, daily on request | $1M+ monthly volume, cross-border, high AOV | Complex statements, lighter US phone support |

| Helcim | IC + 0.50% + $0.25 online, IC + 0.40% + $0.08 in-person | Month to month | T+2 | U.S. merchants $50K to $500K monthly | Limited international acquiring |

| Stax | $99/mo + IC + $0.08 in-person / $0.18 online | Month-to-month membership | T+2 | $50K+ monthly with predictable volume | Membership cost at low volume |

| Worldpay | Custom Interchange-plus, sales only | 12 to 36 months with ETF | T+1 | $5M+ monthly enterprise | Long contracts, opaque pricing |

Stripe

Stripe charges 2.9 percent plus $0.30 per online card transaction and 2.7 percent plus $0.05 in-person, per its public pricing page. There is no monthly fee, no setup fee, no minimum, and no contract. International cards add 1.5 percent. Currency conversion adds 1 percent. ACH is 0.8 percent capped at $5 per transaction. Instant payouts add 1.5 percent.

At $250K monthly online volume on a typical mixed card portfolio with a 1.8 percent interchange floor, Stripe's effective rate runs roughly 2.92 percent plus per-transaction fees, or about 1.05 to 1.15 percent of markup above Interchange-plus benchmarks. At $1M monthly volume the same markup compounds into roughly $11,000 to $12,000 per month in fees above what an Interchange-plus contract would charge.

Stripe offers Custom Pricing through its sales team, typically available above $1M annual processing. Those contracts can drop effective markup into the 0.30 to 0.50 percent range, but the discount is not posted and is rarely volunteered.

Best for: U.S. SaaS, marketplaces, and D2C brands below $1M monthly volume that value developer tooling and same-day onboarding. Avoid if you process more than $2M monthly with thin margins and have not negotiated a Custom contract.

Adyen

Adyen runs Interchange++ pricing. Each transaction is billed in three components: interchange (set by Visa or Mastercard), the card scheme fee or assessment (also set by the network), and Adyen's processing markup. For most U.S. card transactions the processing markup is a fixed $0.13 per transaction, per Adyen's public pricing page. There is no percentage markup on the standard rate card.

Adyen carries a monthly invoice minimum, typically around $120 per merchant entity. If processing fees in a given month fall below that floor, you pay the floor. Settlement is weekly batch by default, configurable to daily on request. Multi-currency processing is native, with a 1 percent FX markup on conversion. Local acquiring across 30+ countries usually lifts authorization rates 1 to 3 percentage points versus single-region routing.

Best for: merchants above $1M monthly card volume, cross-border sellers, marketplaces, and B2B with high average order value. Avoid if you process below $200K monthly, want U.S.-based phone support as your default channel, or need T+1 settlement without configuration work.

Helcim

Helcim charges interchange plus 0.50 percent and $0.25 per online transaction, and interchange plus 0.40 percent and $0.08 in-person, per its public pricing page. There is no monthly fee, no contract, and no setup fee. Volume discounts apply automatically as monthly card volume rises, with markup compressing further at the $50K, $100K, and $250K tiers.

For U.S. merchants between $50K and $500K monthly volume, Helcim usually costs less than both Stripe and Adyen. Stripe's flat rate carries a percentage markup that compounds at every tier, while Adyen's monthly minimum penalizes this volume band. At $250K monthly online volume on a typical card mix with a 1.8 percent interchange floor, Helcim's effective rate runs roughly 2.30 percent, compared to roughly 2.92 percent on Stripe's flat rate.

Best for: U.S. merchants in the $50K to $500K monthly band who want Interchange-plus without negotiating a custom contract. Avoid if you need broad international acquiring, since Helcim's footprint is U.S. and Canada focused.

Stax

Stax uses subscription pricing: $99 per month plus interchange plus $0.08 per in-person transaction or $0.18 per online transaction, per its public pricing page. There is no percentage markup above interchange. The model rewards merchants with stable, predictable monthly volume.

Break-even versus Stripe's flat rate usually arrives around $25K to $40K monthly card volume. Above $100K monthly, Stax is materially cheaper than Stripe on effective rate. At $250K monthly online volume with a 1.8 percent interchange floor, Stax's effective rate runs roughly 1.93 percent, including the membership fee amortized across transactions.

Above $1M monthly volume, Adyen's no-monthly-percentage model can edge out Stax when transaction counts are very high, because Stax's per-transaction fees of $0.08 to $0.18 are higher than Adyen's $0.13 floor on large card batches.

Best for: U.S. merchants between $50K and $1M monthly volume with predictable processing. Watch out for the membership cost if your volume drops below $25K monthly in a given period.

Worldpay

Worldpay (now part of FIS) runs custom Interchange-plus contracts with no public pricing. Setup runs 7 to 14 days. Contracts typically last 12 to 36 months with early-termination fees in the $250 to $500 range, sometimes higher. Settlement is T+1. Level 2 and Level 3 data submission is supported, which matters for B2B merchants accepting corporate and government purchasing cards.

At $5M+ monthly volume Worldpay's effective rates can match or beat Adyen's, but every term is negotiated and the statements are dense. The product wins for enterprise merchants who need a dedicated account manager, ERP integration support, and detailed reconciliation files.

Best for: enterprise merchants above $5M monthly volume with complex integration and reporting needs. Avoid if you want month-to-month flexibility or transparent published rates.

Verdict

For U.S. merchants below $1M monthly card volume, Stripe wins on simplicity, developer tooling, no monthly minimum, and same-day onboarding. The flat-rate markup hurts at scale, but for sub-million volumes the convenience usually beats the math, and the gap closes further once Custom Pricing kicks in.

Above $1M monthly volume, Adyen wins on effective rate. The fixed $0.13 per-transaction processing fee scales without a percentage markup, which is why high-AOV merchants and cross-border sellers consistently choose it. Break-even sits around $750K to $1.2M monthly volume, depending on average ticket and card mix. High-AOV businesses cross over earlier, low-AOV high-volume businesses later.

The runner-up case: if your business is U.S.-only and processes $50K to $500K monthly, neither Stripe nor Adyen is the cheapest option. Helcim's Interchange-plus model usually beats both by 30 to 60 basis points at that tier.