TL;DR

Helcim wins for most U.S. merchants above $25K in monthly card volume. Stripe's flat 2.9 percent plus $0.30 online rate is easy to budget but stops being competitive once interchange averages run below 1.8 percent. Helcim's interchange-plus model passes through the wholesale cost and adds 0.50 percent plus $0.25 online, with automatic volume discounts that drop the margin further at $50K, $100K, and $250K monthly tiers. Stripe wins on developer tooling and global card support.

How we ranked

We compared Stripe and Helcim across six criteria that matter to operating merchants, not feature checkboxes.

- Effective rate at $250K monthly volume on a typical 60 percent debit, 40 percent credit mix, weighted to the rates published in Visa's public interchange schedule and the Mastercard interchange schedule.

- Contract length, monthly minimums, and early termination fees.

- Settlement speed in business days from authorization to bank deposit.

- Level 2 and level 3 data support for B2B merchants who can qualify for lower interchange categories.

- Hardware lock-in and switching cost if the merchant outgrows the platform.

- Dispute and chargeback handling, including documentation tools and SLAs.

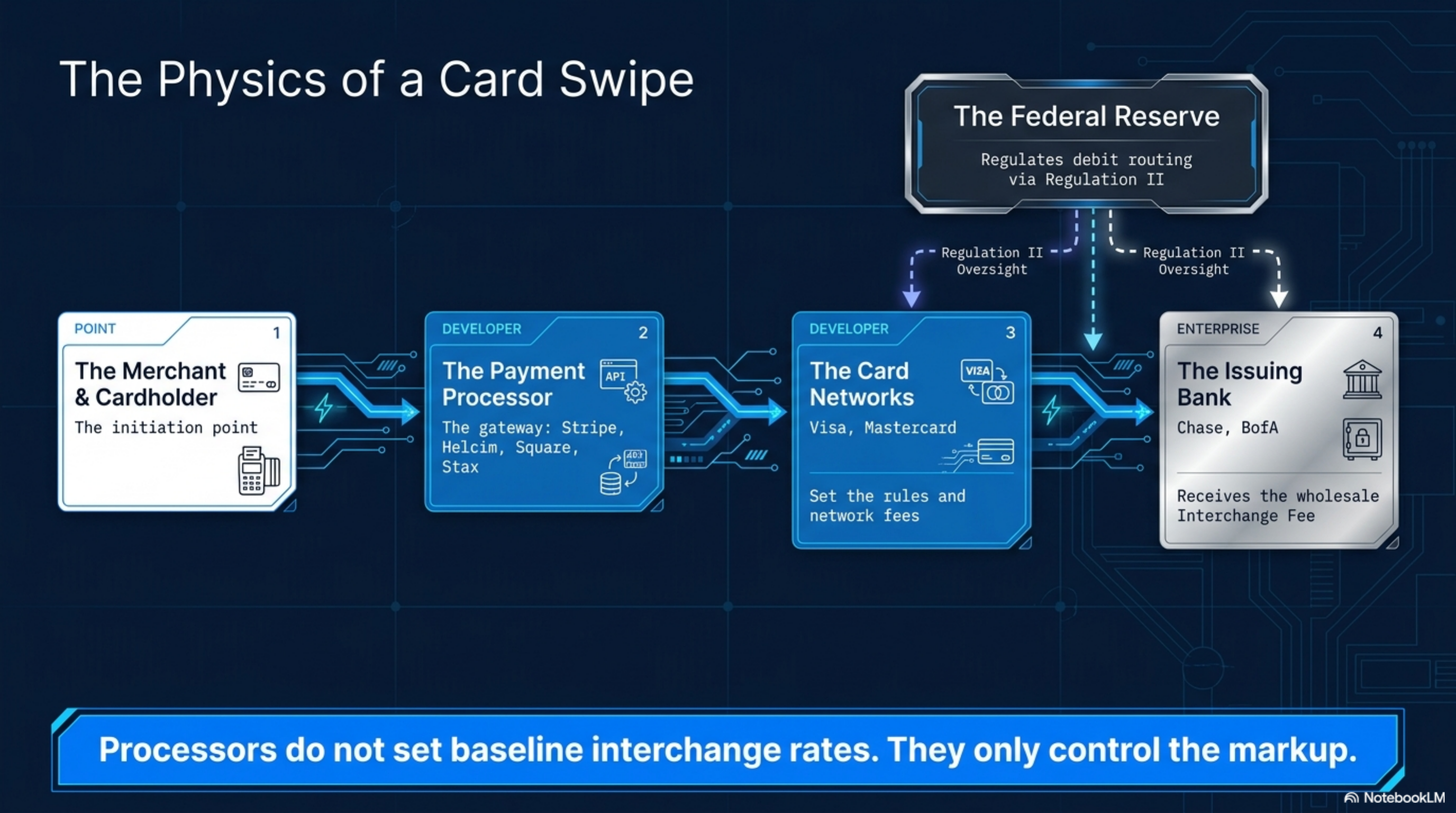

Per the Federal Reserve payments studies, U.S. card interchange has averaged near a 1.7 to 1.9 percent weighted rate across recent reporting cycles, which sets the baseline for our effective rate calculations. We did not weight features like recurring billing, invoicing, or developer SDKs above pricing. Those features matter, but they rarely cost a merchant $40K a year. Processing rates do.

At a glance

Headline rates pulled from each provider's public pricing page. Effective rates depend on card mix, ticket size, and qualification for lower interchange categories.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in-person | Month-to-month | 2 business days | Developer ecommerce, marketplaces | Flat rate persists past $1M volume |

| Helcim | IC + 0.50% + $0.25 online; IC + 0.40% + $0.08 in-person | Month-to-month | 2 business days | $25K to $1M monthly, B2B, retail | Lighter developer tooling |

| Stax | $99/mo + IC + $0.18 online; + $0.08 in-person | Month-to-month | 1 to 2 business days | $50K+ predictable budget | Fixed fee hurts under $40K |

| Square | 2.6% + $0.10 in-person; 2.9% + $0.30 online | Month-to-month | 1 to 2 business days | Retail, food service under $40K | No interchange-plus until $250K |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 | Month-to-month | 1 to 2 business days | Brick and mortar above $40K | Limited ecommerce tooling |

Stripe

Stripe's public pricing is 2.9 percent plus $0.30 per online transaction, and 2.7 percent plus $0.05 for in-person card-present sales through Stripe Terminal. There are no monthly fees, no setup fees, and no contract. International cards add 1.5 percent, and currency conversion adds 1 percent, per Stripe's pricing page.

The 2.9 percent flat rate covers the wholesale interchange cost paid to the card issuer, the network assessment fees paid to Visa and Mastercard, and Stripe's markup. On a typical U.S. consumer card mix, interchange averages between 1.5 and 2.0 percent, which means Stripe's effective markup is 0.90 to 1.40 percent above wholesale before the fixed per-transaction fee.

Stripe wins on developer experience. Its API, SDKs, and Connect platform are the deepest in the market. For SaaS, marketplaces, subscription billing, and any business that runs international cards through more than five currencies, Stripe is hard to beat on engineering velocity.

Stripe loses on rate. A retail merchant doing $250K monthly in U.S. card volume pays the same 2.9 percent on a $20 transaction that they pay on a $2,000 transaction. There is no volume discount until the merchant negotiates a custom contract above roughly $1M monthly volume.

Who it's for: developer-led ecommerce, SaaS, marketplaces, international sellers. Who should avoid it: high-volume retail or B2B card-present merchants who would benefit from interchange-plus pricing.

Helcim

Helcim publishes interchange-plus pricing with no monthly fee, no setup fee, and no early termination fee. Per Helcim's pricing page, the online rate is interchange plus 0.50 percent plus $0.25, and the in-person rate is interchange plus 0.40 percent plus $0.08. Keyed transactions add a small risk premium.

Helcim also applies automatic volume discounts. As monthly volume crosses $25K, $50K, $100K, and $250K, the markup over interchange drops in steps. Helcim publishes the schedule on its pricing page. There is no need to call sales to renegotiate as volume scales.

Helcim supports level 2 and level 3 data on its hosted gateway, which matters for B2B merchants who accept corporate, purchasing, and government cards. Qualifying for these lower interchange categories can reduce the effective rate by an additional 0.50 to 1.00 percent on commercial card transactions, per the Visa interchange schedule cited above.

Who it's for: U.S. and Canadian merchants between $25K and $1M monthly card volume, especially B2B and high-ticket sellers. Who should avoid it: businesses that need a deep international card mix or a custom developer platform. Helcim's API is functional but not at Stripe's depth.

Stax

Stax, formerly Fattmerchant, prices on a subscription model rather than a percentage markup. Per Stax's pricing page, the base plan is $99 per month plus interchange plus $0.08 per in-person transaction or $0.18 per online transaction. Higher-volume tiers run $199 per month.

The math favors subscription pricing only above a clear volume threshold. At $50K monthly volume on a typical card mix, the $99 fee divided across 500 transactions adds roughly $0.20 per transaction. Combined with the per-item fee, the effective markup is about 0.30 to 0.40 percent above interchange. Below $40K monthly, Helcim's percentage model is usually cheaper because there is no fixed subscription drag.

Stax includes a payment dashboard, reporting, invoicing, and 24/7 phone support. The platform suits high-ticket B2B sellers above $50K monthly who want predictable monthly pricing.

Who it's for: subscription-friendly merchants above $50K monthly, B2B, professional services. Who should avoid it: under $40K monthly volume, where the fixed fee eats the savings.

Square

Square uses flat-rate pricing similar to Stripe. Per Square's pricing page, in-person card-present runs 2.6 percent plus $0.10, online runs 2.9 percent plus $0.30, and manually keyed cards run 3.5 percent plus $0.15. There are no monthly fees for the base POS and gateway.

Square's strength is its free POS software and tight hardware integration. For retail, restaurants, and personal services under $40K monthly volume, the all-in package is hard to match. Same-day funding is available on a paid plan.

Square loses on rate above $40K monthly. The flat 2.6 percent card-present rate carries a markup of roughly 0.60 to 0.90 percent above interchange after the per-transaction fee. Square does not move to interchange-plus until volume passes roughly $250K monthly through a custom contract.

Who it's for: retail, food service, personal services under $40K monthly volume that need a POS. Who should avoid it: high-volume merchants where flat-rate markup compounds.

Payment Depot

Payment Depot prices on a membership model. Per Payment Depot's pricing page, plans range from $79 to $199 per month and pass interchange through with a fixed per-transaction fee of $0.05 to $0.15.

The math is similar to Stax. Above roughly $40K monthly volume, the membership fee divided across transactions is competitive with Helcim's percentage markup. Below that, the fixed monthly fee makes Helcim cheaper.

Payment Depot routes processing through Worldpay and other backend processors. Hardware options include Clover and Dejavoo terminals. The contract is month-to-month with no early termination fee, per the published terms.

Who it's for: brick-and-mortar above $40K monthly volume, wholesale, distribution. Who should avoid it: sub-$40K monthly volume merchants and ecommerce-only sellers where Helcim's online tooling is more complete.

Verdict

For most U.S. merchants between $25K and $1M monthly card volume, Helcim is the lower-cost choice. Interchange-plus pricing with automatic volume discounts beats Stripe's flat 2.9 percent at the rates published on both companies' pricing pages, especially on high-ticket B2B sales where level 2 and level 3 data qualifies the merchant for lower interchange.

Stripe wins in three cases: developer-led ecommerce that needs deep API tooling, marketplaces using Stripe Connect, and international sellers running more than five currencies. The flat-rate premium is the cost of engineering velocity, not a tax to avoid.

Below $25K monthly card volume, both processors are fine. The savings difference is usually under $200 per month, and the time spent switching outweighs the gain. Above $1M monthly volume, neither company is the right answer. Get quotes from a subscription processor like Stax or a tier-one acquirer and compare against a Visa Interchange Schedule baseline.