TL;DR

Payment Depot beats Stripe on total cost above roughly $30,000 in monthly card volume. Its $79 to $199 membership plus interchange-plus pricing settles around 2.3 to 2.5 percent effective on a typical U.S. card mix, where Stripe's flat 2.9 percent plus 30 cents stays fixed. Stripe still wins for online businesses under $25,000 monthly, marketplaces, any merchant needing global multi-currency acceptance, and software companies built on its API. The choice tracks volume, not feature lists.

How we ranked

We weighted six criteria. Effective rate at $50,000 and $250,000 monthly volume, modeled against a card mix of 60 percent debit, 30 percent rewards consumer credit, and 10 percent commercial cards, drawn from card usage patterns in the Federal Reserve payments studies. Contract length and early termination fee, sourced from each provider's published terms. Settlement speed in business days. Hardware lock-in. Level 2 and level 3 data support, which matters for B2B card-not-present and can drop interchange on commercial cards by 0.40 to 1.00 percent per Visa's published interchange schedule. Dispute handling and chargeback fee structure.

All pricing came from each company's public pricing page. Interchange figures came from Visa's and Mastercard's published interchange rates and criteria. We did not model promotional credits, custom enterprise contracts, or any sales-negotiated rates.

At a glance

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online, 2.7% + $0.05 in person | Month-to-month, no ETF | 2 business days | Online-first under $30K/mo, global, developer-led | Margin compounds above $40K monthly |

| Payment Depot | $79 to $199/mo + IC + $0.05 to $0.15 per txn | Month-to-month, no ETF on base plans | 2 business days | $30K to $500K monthly U.S. card volume | Membership eats savings under $20K/mo |

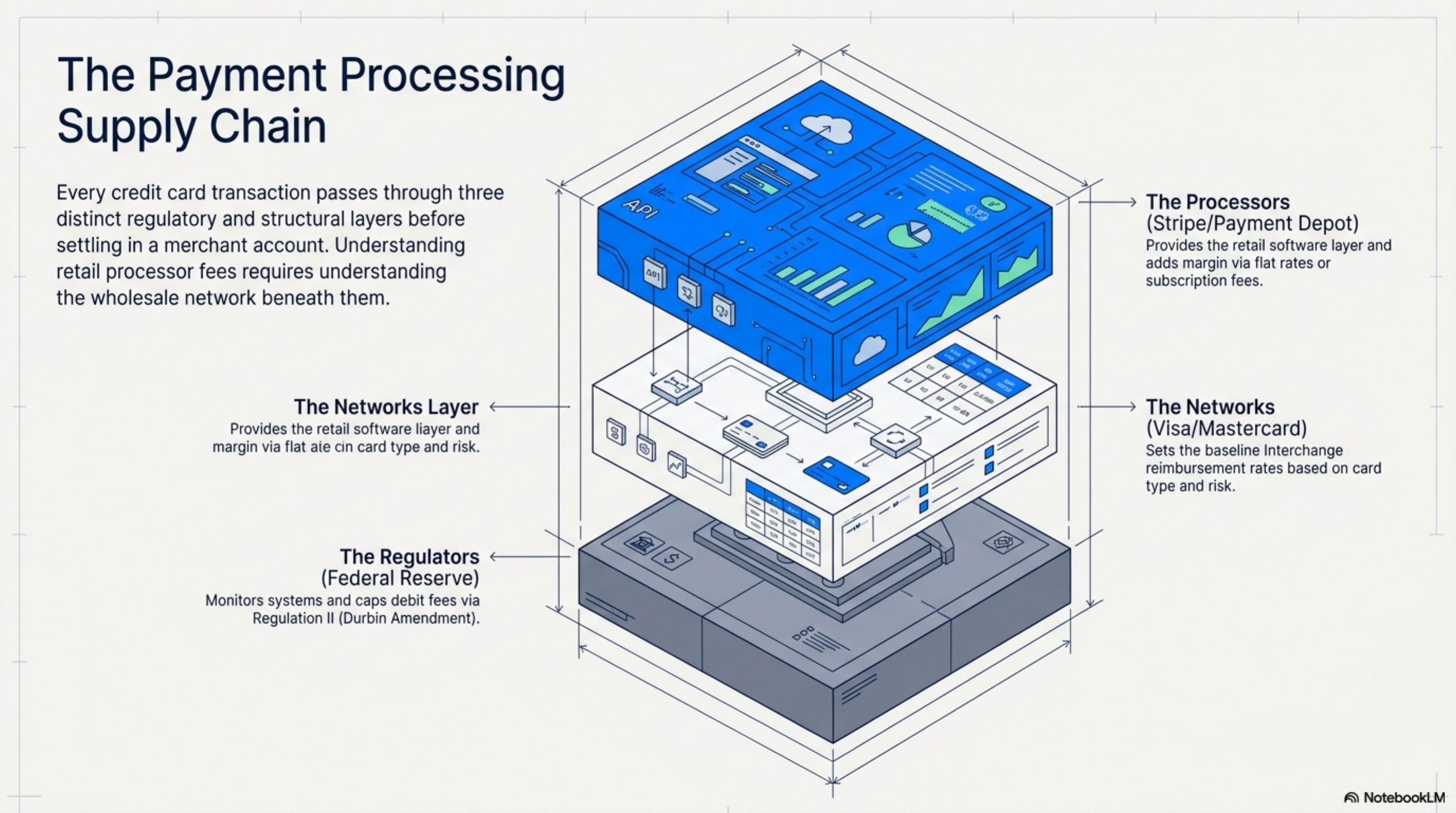

Two providers, two pricing models. Stripe pools all costs into a flat percentage. Payment Depot separates the wholesale cost (interchange) from the processor's markup (a flat membership fee plus a small per-transaction charge). The same $250,000 in monthly card volume produces meaningfully different effective rates under the two structures.

Stripe

Stripe's published rate is 2.9 percent plus 30 cents for online card payments and 2.7 percent plus 5 cents in person, per its public pricing page. There is no monthly fee, no PCI fee, and no statement fee on the standard plan. Settlement is 2 business days for most U.S. merchants.

The flat-rate model means Stripe earns more on debit transactions than on premium rewards credit. Debit interchange is capped at 0.05 percent plus 22 cents under the Durbin Amendment for regulated issuers, while Stripe still bills 2.9 percent plus 30 cents. On a $50 debit purchase, true network cost is around 25 cents but Stripe collects $1.75. The math works fine at low volume. It compounds at scale.

A SaaS company at $30,000 in monthly card volume on Stripe pays roughly $930 per month in processing. The same volume on Payment Depot's $99 plan lands around $760 per month, a $170 monthly difference. At $30K the gap is real but small, so most operators stay on Stripe until volume justifies the switch.

What Stripe sells well: same-day onboarding, a developer-first API, broad international card coverage across 135 currencies, and a payments stack you can deploy without negotiating a sales contract. For marketplaces, SaaS, and any online business under roughly $25,000 monthly, the flat rate beats the time cost of a interchange-plus relationship.

What it does not sell well: surcharging, cash discount programs, and level 2 or level 3 data optimization on commercial cards, all of which are gated behind enterprise contracts. There is also no native path to lower per-transaction cost as volume climbs on the standard plan.

Payment Depot

Payment Depot uses a membership model. Per its public pricing page, plans run $79 to $199 per month plus interchange plus a fixed per-transaction markup of $0.05 to $0.15 depending on plan tier. There is no percentage markup over interchange. Standard plans are month-to-month with no early termination fee.

Take a $250 average ticket on a Visa rewards consumer credit card. Interchange on that transaction is roughly 1.65 percent plus 10 cents per Visa's published schedule. Payment Depot's all-in cost lands around 1.65 percent plus 20 to 25 cents in fixed markup, versus Stripe's flat 2.9 percent plus 30 cents. The per-transaction difference is roughly $3.15. On $250,000 in monthly volume with that mix, the annual difference clears $18,000.

Ask Payment Depot for a side-by-side analysis using your last 3 months of Stripe statements. The membership tier you qualify for depends on volume and average ticket, and a real comparison usually moves you down one plan tier and saves another $40 to $60 per month.

Payment Depot supports level 2 and level 3 data on standard plans, which can shave another 0.40 to 1.00 percent off commercial card interchange for B2B merchants. Settlement runs 2 business days. Support is U.S.-based but limited to Monday through Friday business hours.

What it does not do well: no native multi-currency support, no developer-first API, and account setup takes 1 to 2 business days against Stripe's same-day account. The membership structure also means below roughly $20,000 monthly, the fixed monthly fee swamps any interchange-plus savings.

Read the merchant services agreement, not just the pricing page. Check for PCI compliance fees, monthly minimum processing requirements, gateway transaction fees if you use a third-party gateway, and any annual fee separate from the monthly membership. Hardware leases are a separate contract with their own terms.

Verdict

For merchants processing more than $30,000 per month in U.S. card volume, Payment Depot costs less. The membership model converts what Stripe charges as percentage markup into a fixed monthly fee, and the gap at $100,000 to $500,000 monthly is meaningful. A merchant at $250,000 monthly typically saves $1,500 to $2,000 per month moving from Stripe's flat rate to Payment Depot's interchange-plus structure, modeled against a standard U.S. card mix.

Stripe wins three specific cases. Online businesses under $25,000 monthly volume, where the membership fee outweighs the markup savings. Any merchant needing global multi-currency acceptance, where Stripe's 135-currency coverage has no equivalent at Payment Depot. And software companies that need Stripe's API, billing primitives, and developer infrastructure, where switching cost is operational rather than financial. For everyone else processing meaningful U.S. card volume, the wholesale-style membership model is the cheaper path.