TL;DR

For US merchants under $25K monthly volume, Square charges 2.6 percent plus 10 cents in-person and Stripe charges 2.7 percent plus 5 cents. Square wins on tickets above $50; Stripe wins below. Both charge 2.9 percent plus 30 cents online. Above $80K monthly volume, neither flat rate fits: an interchange-plus processor like Helcim typically saves 0.30 to 0.60 percent. Square wins for in-person retail and food service. Stripe wins for online businesses with global card mix.

How we ranked

We weighted five criteria for a US merchant evaluating Stripe vs Square in 2026:

- Effective rate at $250K monthly volume, modeled with a typical retail card mix of 35 percent regulated debit, 50 percent rewards credit, and 15 percent business and corporate cards, using Visa and Mastercard published interchange tables.

- Contract length and ETF. Any plan over 12 months with an early termination fee above $295 was marked down hard.

- Settlement speed. Same-day or next-day funding with no fee beats 2 business day funding with a 1.5 percent instant payout.

- Hardware lock-in. Terminals locked to a single processor are marked down because they raise switching cost.

- Public pricing transparency. Rates that are not on the public site without a sales call are marked down.

Each provider section names the volume tier and vertical where it wins, not whether it is best in the abstract.

At a glance

Five providers, headline pricing pulled from each public pricing page as of May 2026.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in-person | None | 2 business days | Online businesses, global card mix | No phone support on free plan; instant payout costs 1.5% |

| Square | 2.6% + $0.10 in-person; 2.9% + $0.30 online; 3.5% + $0.15 keyed | None | Next business day | Retail, food service, free POS | Account holds and reserves on high-risk MCCs |

| Helcim | IC + 0.40% + $0.08 in-person; IC + 0.50% + $0.25 online | None | 2 business days | $25K+ monthly volume seeking interchange-plus | No free hardware bundle; needs PCI scan |

| Clover | $14.95 to $54.95/mo plan + 2.3 to 2.6% + $0.10 in-person; 3.5% + $0.10 keyed | Often 36 mo via reseller | Next business day | Quick-service restaurants needing POS hardware | Sold via Fiserv and ISOs with variable pricing and ETFs |

| PayPal | 3.49% + $0.49 standard; 2.59% + $0.49 advanced card; 2.29% + $0.09 in-person | None | Same day to wallet, 1 day to bank | Online checkout with PayPal-loyal buyers | Highest per-transaction fixed fee in this group |

Stripe

Stripe charges 2.9 percent plus 30 cents per online card payment and 2.7 percent plus 5 cents per in-person tap or chip read on its standard plan, per the published Stripe pricing page. There is no monthly fee, no setup fee, no PCI compliance fee, and no contract. Settlement runs on a rolling 2 business day schedule for new accounts; instant payout to a debit card costs 1.5 percent of the transfer amount.

For US-only retail volume under $25K per month, Stripe is rarely the cheapest answer. The math gets interesting when you sell internationally (Stripe adds 1 percent for international cards and 1 percent for currency conversion), accept Apple Pay or Google Pay through a custom checkout, or need to support 135-plus currencies and 30-plus payment methods without bolting on a separate gateway.

Stripe Connect, Stripe Issuing, and the Radar fraud engine are the practical reasons engineering-led businesses pick it. Above $80K monthly card-not-present volume, ask Stripe sales for an interchange-plus quote. The published 2.9 percent plus 30 cents bakes in roughly 0.40 to 0.60 percent of markup over interchange depending on card mix, money you are leaving on the table at scale.

Avoid Stripe if you need a free phone support number, want a brick-and-mortar POS with a built-in cash drawer, or process predominantly large in-person tickets where Square's flat 2.6 percent edges it on every receipt over $50.

Square

Square's published rates are 2.6 percent plus 10 cents per tap, dip, or swipe; 2.9 percent plus 30 cents for invoices and online checkout; and 3.5 percent plus 15 cents for manually keyed cards, per the Square pricing page. The free plan includes the Square POS app, the Square Dashboard, basic inventory, and a free magstripe reader. Hardware ranges from a $59 Square Reader for contactless and chip to the $799 Square Register.

Funding is free next business day to a linked bank account, or instant for 1.75 percent. Square does not charge monthly fees, PCI fees, statement fees, or contract ETFs on the free tier. Square for Restaurants Plus runs $69 per location per month. Square for Retail Plus runs $89 per location per month.

Square wins for storefront retail under $1M annual volume, food trucks, mobile services, and any operator who values not paying a monthly fee for a working POS over saving 0.20 percent on processing.

Helcim

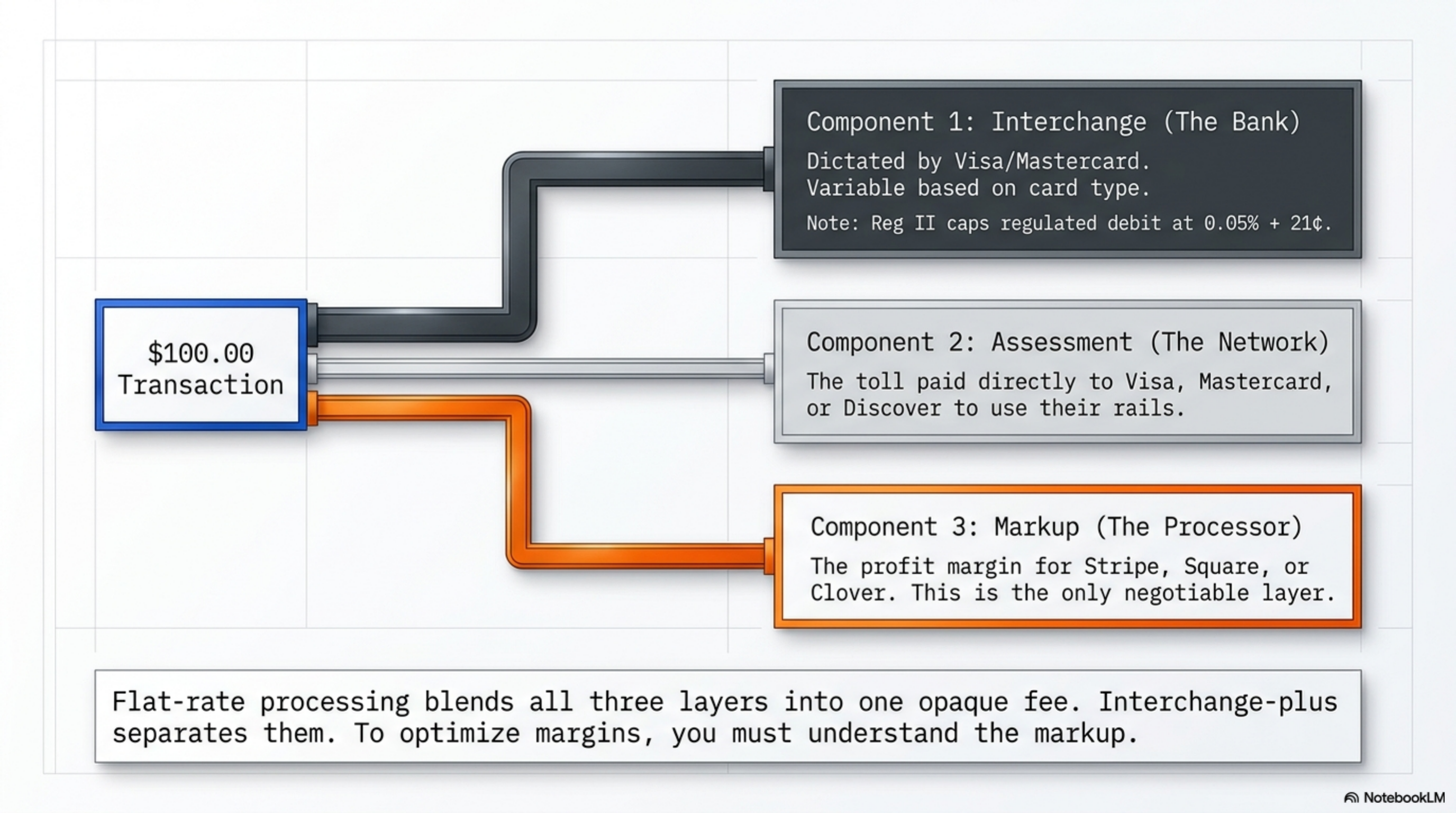

Helcim publishes interchange-plus rates with automatic volume discounts. The advertised markup is interchange plus 0.40 percent plus 8 cents in-person, and interchange plus 0.50 percent plus 25 cents card-not-present, per the Helcim pricing page. There is no monthly fee, no statement fee, no PCI fee, and no contract. As your monthly card volume rises, the markup steps down automatically across published volume tiers.

For a $250K monthly retail business with a typical card mix of regulated debit and Visa/Mastercard credit (regulated debit is capped at 0.05 percent plus 21 cents per the Federal Reserve Reg II rule), Helcim's effective rate lands around 2.10 to 2.30 percent all-in versus Square's 2.7 percent flat. On $3M annual volume that is a $12,000 to $18,000 per year difference, before any savings on level 2/3 data for B2B card-not-present volume.

Helcim provides a virtual terminal, hosted checkout, in-person card readers, ACH at 0.5 percent capped at $6, and an open API. Settlement runs 2 business days. Customer support is business-hours phone, chat, and email.

Avoid Helcim if you process under $5K monthly (the per-transaction fixed costs eat the markup advantage), if you need 24/7 phone support, or if you are wedded to a specific POS hardware ecosystem like Clover or Toast.

Clover

Clover is a hardware-first POS sold direct, through Fiserv (its parent), and through hundreds of independent sales agents and ISOs. Clover's direct online plans range from $14.95 to $54.95 per month, with rates of 2.3 to 2.6 percent plus 10 cents in-person and 3.5 percent plus 10 cents keyed, per the Clover product pages. Hardware bundles run from the $49 Clover Go reader to the $1,799 Clover Station Solo.

Clover also locks transaction processing to First Data/Fiserv. You cannot switch processors and keep your Clover terminals fully functional without buying a license fee or new hardware. That is a structural cost most POS comparisons skip.

Clover wins for quick-service restaurants and salons that want a polished tablet POS with a working app marketplace, and that are willing to negotiate hard at signing and to push back on a 36 month contract.

PayPal

PayPal is two products in one merchant account. The PayPal-branded checkout button is 3.49 percent plus 49 cents per transaction, per the PayPal merchant fee schedule. PayPal Advanced Credit and Debit Card processing, the white-labeled card form on your site, is 2.59 percent plus 49 cents. In-person via PayPal Zettle is 2.29 percent plus 9 cents.

The 49 cent fixed fee is the highest among the five providers in this comparison. On a $25 average ticket, PayPal Advanced is roughly 4.55 percent all-in versus Stripe's 4.10 percent and Square Online's 4.10 percent. On a $200 ticket the gap closes: PayPal is about 2.83 percent versus Stripe's 3.05 percent. PayPal wins on larger card-not-present tickets where the percentage rate matters more than the per-transaction fixed.

The two-product structure exists for a reason. PayPal Advanced and the PayPal button together can convert better than a card-only checkout for some merchant types (digital goods, donations, B2C services), per consumer payment data published by the Federal Reserve Payments Studies. If your customers want to pay with a PayPal balance or Pay in 4, the conversion lift can outrun the higher per-transaction cost.

Avoid PayPal as your only processor if you sell B2B and your average ticket runs under $50, or if you need level 2/3 commercial card data passed through.

Verdict

Square is the right answer for in-person retail and food service under roughly $80K monthly card volume. The free POS, free magstripe reader, next-day funding, and absence of monthly fees make it the lowest total cost when you account for hardware and software, not just the percentage on the statement.

Stripe is the right answer for online businesses, marketplaces, and any product where the engineering team picks the processor. The international card support, the 30-plus alternative payment methods, and Stripe Connect are the reasons, not the rate.

Above $80K monthly volume, neither flat rate is the cheapest answer. Helcim's interchange-plus pricing typically saves 0.30 to 0.60 percent at scale, and at $3M annual card volume that is real money. The right move at that point is to keep Square or Stripe as a secondary, not primary, processor.