TL;DR

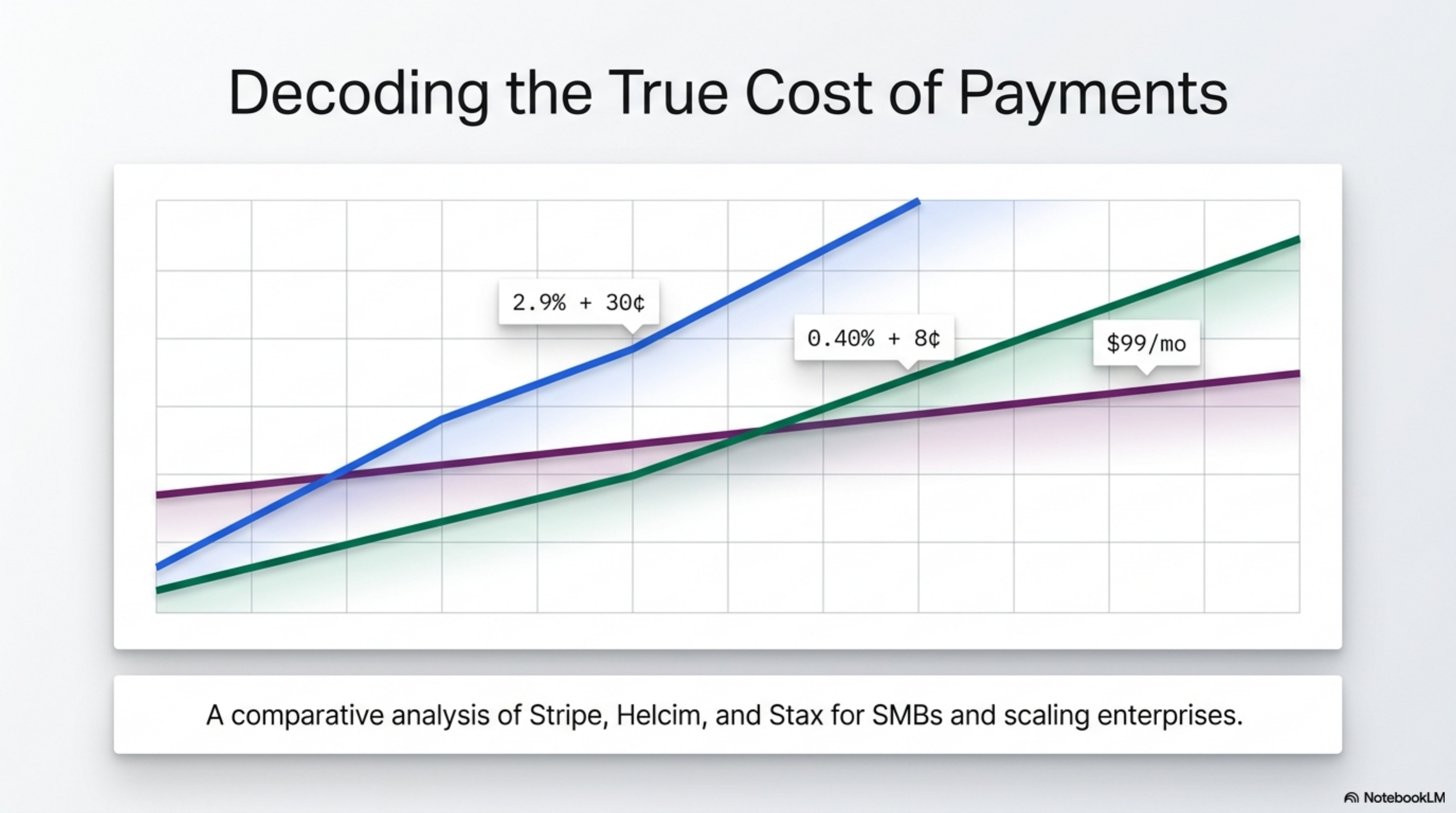

For merchants processing $50,000 to $5 million per month with predictable card mix, Stax usually costs less than Stripe. Stax charges a $99 monthly subscription plus interchange and $0.08 (in-person) or $0.18 (online) per transaction. Stripe charges 2.9 percent plus $0.30 per online transaction on its flat-rate plan. At $50,000 monthly online volume with a $50 average ticket, Stax saves roughly $500 per month. Stripe still wins for global currencies, embedded platforms, and merchants under $20,000 monthly volume.

How we ranked

We compared Stripe and Stax on the five line items that move the most money on a real merchant statement.

- Effective rate at $250K monthly volume, calculated against the published Visa and Mastercard interchange schedules.

- Total monthly cost including subscription, per-transaction fees, gateway fees, and statement fees.

- Contract terms: month-to-month versus term contracts, early termination fees, and price-lock language.

- Settlement speed in standard banking days.

- Hardware and platform lock-in: proprietary terminals, gateway portability, and the cost of switching processors later.

Each line item was weighted by how often it shows up on the statement of a $50K to $1M monthly volume merchant. Pricing is verified against each provider's public pricing page. Where a provider publishes a range, we noted the range rather than picking a midpoint, because the midpoint hides what actually shows up on the statement.

At a glance

Five processors that a merchant choosing between Stripe and Stax should also price out before signing. Numbers come from each provider's public pricing page.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in-person | Month-to-month | 2 business days | Under $20K volume, global | Flat rate scales badly above $50K |

| Stax | $99/mo + IC + $0.08 in-person / $0.18 online | Month-to-month | 1 to 2 business days | $50K-$5M mixed volume | Subscription pays off above ~$8K volume |

| Helcim | IC + 0.40-0.50% + $0.08-$0.25 | Month-to-month | 2 business days | $5K-$25K transparent pricing | No same-day funding |

| Payment Depot | $79-$199/mo + IC + $0.05-$0.15 | Month-to-month | 1 to 2 business days | $20K-$80K brick-and-mortar | Tier caps trigger upgrades |

| Square | 2.6% + $0.10 in-person; 2.9% + $0.30 online | Month-to-month | Same day | Under $15K, new businesses | No rate negotiation below flat rate |

Stripe

Stripe's headline rate is 2.9 percent plus $0.30 per online transaction and 2.7 percent plus $0.05 in person. There is no monthly subscription, no setup fee, and no minimum on the Standard plan. Settlement runs on a two-business-day rolling basis for new accounts. Instant payouts cost an additional 1.5 percent.

Stripe makes sense for:

- New businesses under $25,000 monthly volume where no subscription beats any percentage discount.

- Online-only operators who need recurring billing, multi-currency, or developer APIs.

- Marketplaces and platforms using Stripe Connect for split payments.

- International expansion: Stripe supports 135-plus currencies across 47 countries.

Stripe is the wrong choice for:

- Card-present retail or restaurant volume above $50K monthly, where flat rate stops being competitive.

- B2B operators who need level 2 and level 3 data optimization to bring down commercial card interchange.

- Merchants whose card mix skews toward rewards and corporate cards: flat rate hides the real cost.

Stax

Stax (formerly Fattmerchant) prices on a subscription model. The base plan is $99 per month plus interchange plus $0.08 per in-person or $0.18 per online transaction. There is no percentage markup on top of interchange. Per-transaction fees stay flat as volume grows, which is the whole point.

That structure flips the math. The break-even point against Stripe lands at roughly $7,000 to $9,000 in monthly volume depending on card mix and average ticket. Above that, every additional dollar of processing costs less at Stax than at Stripe.

Interchange: $925

Per-transaction fees (1,000 x $0.18): $180

Subscription: $99

Total: $1,204 per month

Same volume on Stripe Standard: roughly $1,750. Stax saves about $546 per month, or $6,552 per year, on this profile.

Stax fits:

- $20K to $5M monthly volume merchants with predictable transaction counts.

- Retail, professional services, and SaaS operators who want interchange transparency.

- Businesses that want to use their own terminal hardware via Stax's open gateway integration.

Helcim

Helcim publishes interchange-plus pricing with no monthly subscription and automatic volume discounts. Online starts at interchange plus 0.50 percent plus $0.25; in-person starts at interchange plus 0.40 percent plus $0.08. Markup drops as monthly volume crosses tier thresholds at $25K, $50K, $100K, and $250K.

For merchants between $5K and $25K monthly volume, Helcim usually beats both Stripe and Stax. There is no subscription to pay off, lower markup than Stripe's flat rate, and no minimum.

Above $50K, Stax's flat per-transaction model often wins because Helcim's percentage markup keeps scaling with volume while Stax's per-transaction fee does not.

Helcim is the wrong choice for businesses that need same-day payouts (it funds in two business days) or for high-volume B2B merchants who need a dedicated rep working level 3 optimization on commercial cards.

Payment Depot

Payment Depot, owned by Stax Payments since 2021, sells a similar subscription model under a different brand. Plans run from $79 to $199 per month plus interchange plus $0.05 to $0.15 per transaction.

The $79 plan caps at $25K monthly processing. The $199 enterprise tier handles unlimited volume. Payment Depot tends to come in cheaper than Stax at the lower bands and roughly the same at high volume.

The acquisition by Stax means the two products share underwriting and settlement infrastructure. The pricing is published publicly, which is unusual among wholesale processors.

Payment Depot fits:

- Brick-and-mortar retailers with $20K to $80K monthly volume.

- Operators who want subscription pricing but lower than Stax's $99 base.

Watch the per-transaction fee range. The published numbers are starting points; confirm what your card mix actually triggers before signing.

Square

Square charges 2.6 percent plus $0.10 in person, 2.9 percent plus $0.30 online, and 3.5 percent plus $0.15 keyed. No monthly fee on the free plan, no contract, no minimum.

Square has the lowest-friction onboarding in the industry. Same-day funding is included. The POS software is free. Hardware starts at $0 for the magstripe reader and $59 for the contactless terminal.

Square fits:

- New retailers and restaurants with less than $15K monthly volume.

- Pop-up shops, farmer's market vendors, mobile service businesses.

- Operators who want to be processing payments by tomorrow morning.

Above $25K to $30K in monthly volume, Square's flat rate stops being competitive. Stax, Payment Depot, and Helcim all cost less at that point. Square does not negotiate rates below the published flat rate for most accounts, and the lack of interchange visibility makes it hard to optimize a high-volume card mix.

Verdict

For merchants doing $50K or more per month in mixed in-person and online volume, Stax costs less than Stripe in nearly every realistic scenario. The break-even tips toward Stax somewhere between $7K and $10K monthly volume, depending on average ticket and card mix. At $250K monthly volume, the gap can clear $50,000 annually on a typical retail card mix.

Stripe wins three scenarios. First: monthly volume under $20K, where no subscription beats the lower per-transaction cost. Second: international expansion, where Stripe's currency and country coverage is unmatched. Third: developer-built platforms using Stripe Connect, Issuing, or embedded finance, products Stax does not offer.

If neither fits, look at Helcim for sub-$50K volume merchants who want interchange transparency without a subscription, or Payment Depot for retailers who want Stax's pricing model at a lower base fee. The Federal Reserve's payments studies show interchange remains the largest line on most merchant statements. The right processor is the one that exposes it, not the one that buries it.