TL;DR

Cross-border declines run 5 to 15 percent higher than domestic declines on the same card network, mostly because the issuer sees a foreign acquirer BIN and tightens its risk model. If you sell to buyers in 3 or more countries, routing every transaction through one US acquirer leaves money on the table. The fix is local acquiring in each major corridor, which lifts approval rates by 3 to 8 points and trims cross-border interchange by 0.40 to 1.20 percent per swipe.

What this actually is

Acquirer selection for international means choosing which licensed acquiring bank settles your card transactions in each country where you sell. The acquirer holds your merchant account, sends authorization requests to Visa or Mastercard, and deposits the net amount in your operating bank.

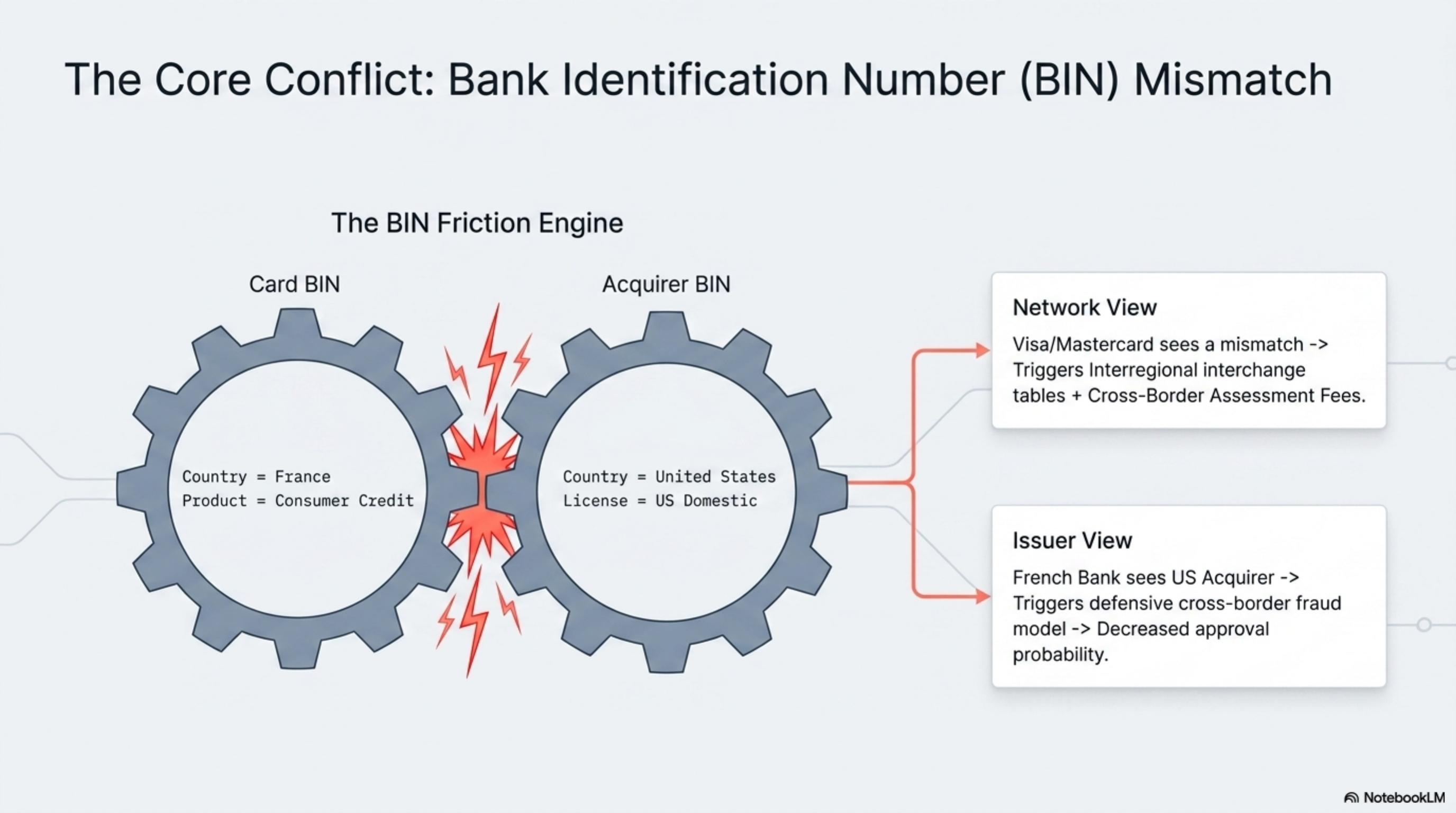

When a US acquirer routes a charge for a buyer in Berlin, the issuing bank in Berlin flags the transaction as cross-border. Visa publishes separate interchange schedules for domestic and international categories, and the cross-border rates run 0.30 to 1.20 percentage points higher than equivalent domestic rates. Mastercard publishes a similar split with cross-border assessment fees stacked on top of standard interchange.

Beyond fees, issuers run distinct fraud models for cross-border traffic. A French issuer scoring a charge from a US acquirer BIN applies a tighter approval threshold than the same charge from a French acquirer. Federal Reserve payments research documents the gap: cross-border approval rates trail domestic rates by single-digit percentage points on the same card network, with the gap widening on consumer credit cards above 100 USD ticket size.

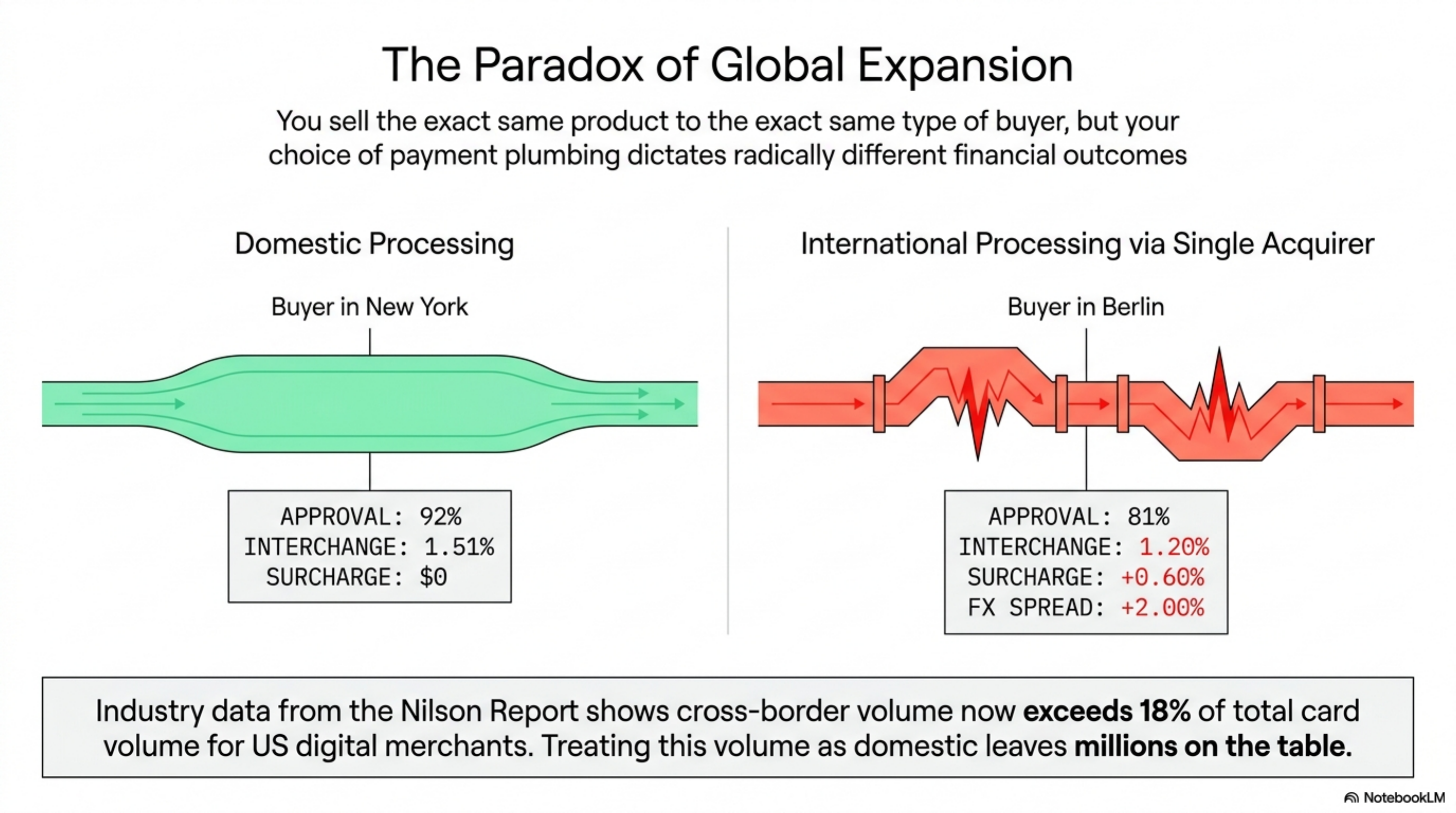

The result: same card, same buyer, same product, but the choice of acquirer changes both the fee paid and whether the charge clears at all. Industry data from Nilson Report shows cross-border volume now exceeds 18 percent of total card volume for US-based merchants selling digital goods, which makes the acquirer decision a top-three cost line for any international operator.

Acquirer selection for international is the practice of routing card transactions through a domestic licensed acquirer in each major sales region to lift approval rates and cut cross-border fees.

How it works under the hood

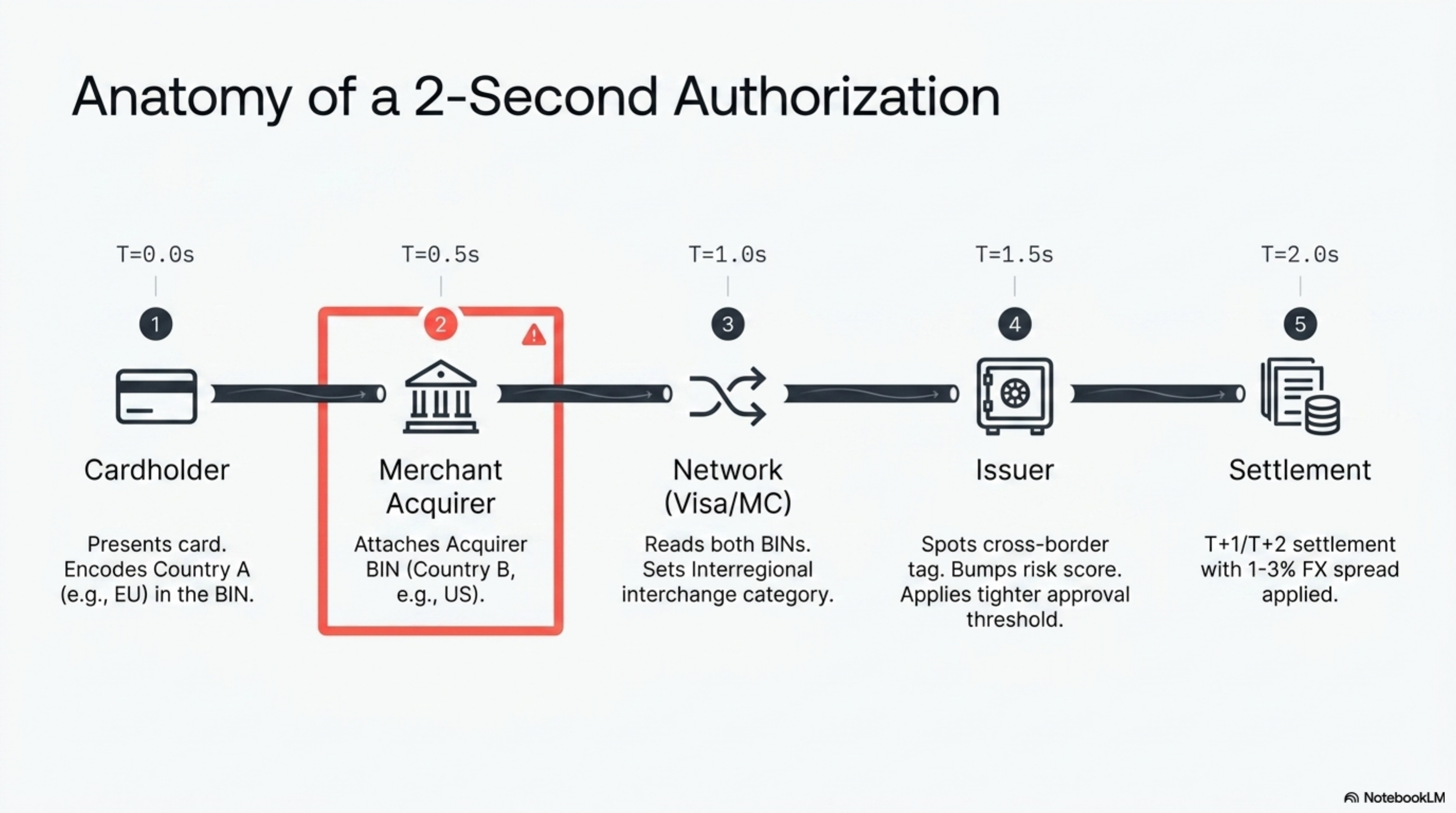

An international card transaction touches five parties in roughly two seconds. Each one has a fee, a risk model, and a regulatory footprint that shifts based on where the acquirer is licensed.

- Cardholder presents a card. The card was issued by a bank in country A. The card BIN encodes country A and the product type (consumer credit, premium, commercial, debit).

- Merchant submits to acquirer. The acquirer can be in country A (domestic), country B (cross-border), or a third country entirely. The acquirer attaches its own BIN to the authorization request.

- Network routes the auth. Visa or Mastercard reads both BINs, looks up the matching interchange category, and forwards the auth to the issuer. Visa's interchange tables separate domestic, intraregional (within the EEA for example), and interregional categories.

- Issuer scores and decides. The issuing bank pulls cardholder context, transaction history, 3DS results, and the acquirer country. A cross-border tag bumps the risk score. The issuer approves, declines, or sends a soft decline (for example, code 65 requesting 3DS step-up).

- Funds settle. The acquirer settles in its licensed currency (USD if US-based, EUR if EU-based) on T plus 1 or T plus 2. Cross-border settlement adds FX conversion, where the spread averages 1 to 3 percent depending on the acquirer's correspondent banking arrangement.

- Fees post. The merchant's statement shows interchange, network assessments, acquirer markup, and cross-border or international surcharges. Mastercard's published rates list both standard and cross-border line items, including the International Acquirer Fee at roughly 0.60 percent.

Local acquiring breaks this chain at step 2. The merchant signs separate acquirer contracts (or uses a payments orchestrator with local entities) so that EU charges hit an EU acquirer, UK charges hit a UK acquirer, and so on. The issuer at step 4 then sees a domestic BIN, drops the cross-border flag, and applies the lower-friction risk model.

Where it goes wrong for operators

Four patterns drain margin from operators who default to a single US acquirer for global sales.

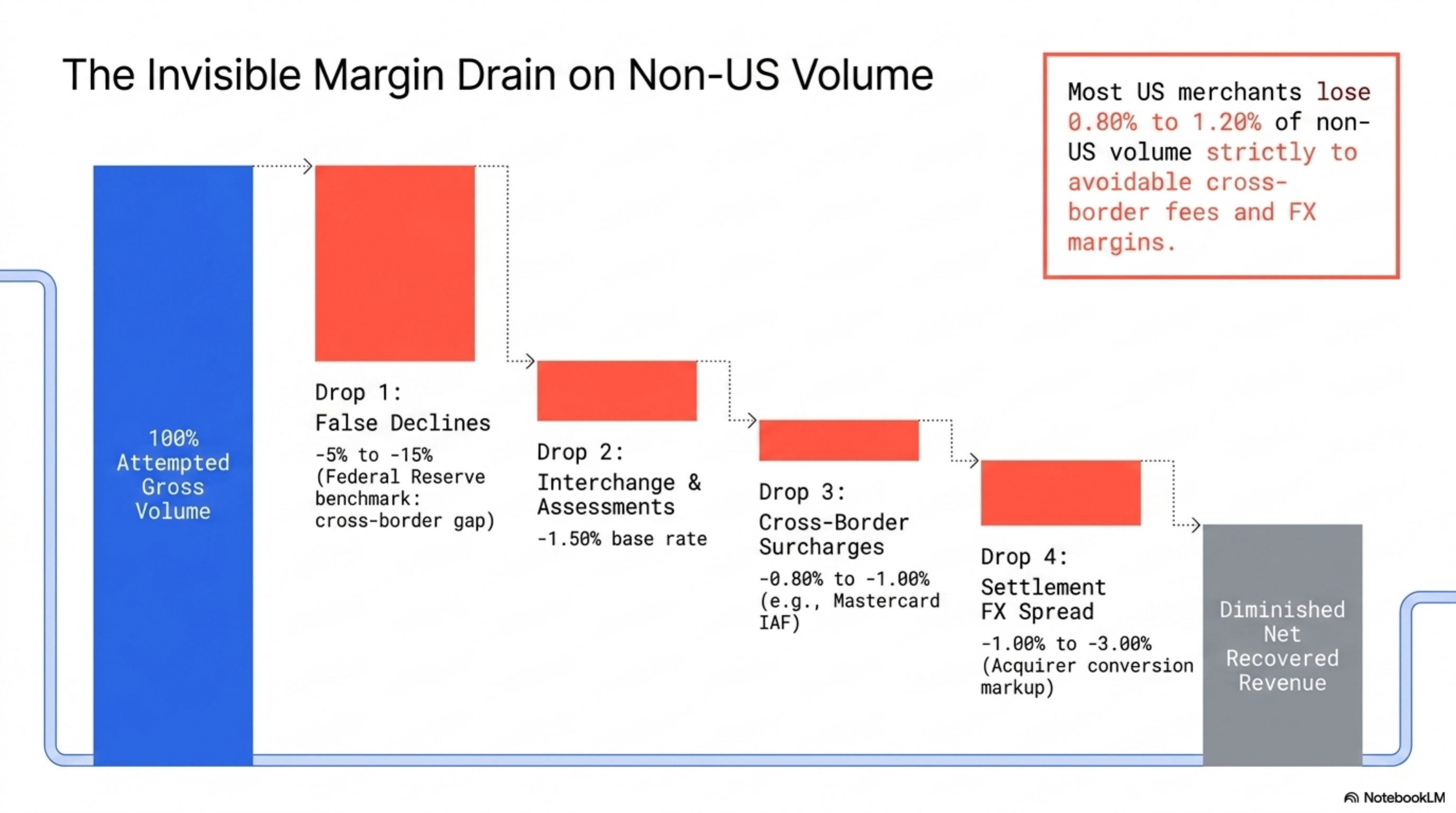

1. Stacked cross-border fees. Visa's interregional consumer credit interchange runs about 1.20 percent plus fixed fees, against roughly 1.51 percent for US consumer credit but with cross-border surcharges of 0.40 to 0.60 percent layered on top. On $400,000 of monthly EU volume routed through a US acquirer, the cross-border surcharge alone runs $1,600 to $2,400 per month, or $19,200 to $28,800 per year that a local EU acquirer would not charge.

2. Approval rate decay. Federal Reserve payments studies and processor public benchmarks show domestic approval rates in the high 80s to mid 90s, while cross-border approval rates run 5 to 15 points lower. On $400,000 of attempted EU volume at a 7-point approval gap, a merchant loses $28,000 per month in unrecovered authorizations, of which roughly half are good buyers who never retry. That is $168,000 in annualized lost good volume from one corridor.

3. Dynamic currency conversion (DCC) traps. Some US acquirers default to billing the cardholder in USD at a marked-up FX rate. Cardholders see a USD price with an estimated home-currency value and abandon. Nilson Report data on card abandonment shows DCC presentation correlates with a 3 to 6 point lift in cart abandonment for EU buyers. The acquirer pockets the FX spread either way, so they will not flag this for you.

4. PSD2 SCA exemption mismatch. EU regulations require Strong Customer Authentication on most consumer card payments above 30 EUR. A local EU acquirer can request Transaction Risk Analysis (TRA) exemptions on behalf of the merchant when fraud rates stay below thresholds set by the European Banking Authority. A US acquirer typically cannot, which means every EU consumer charge runs 3DS, costing 5 to 8 points of frictional decline.

Most US merchants lose 0.80 to 1.20 percent of non-US volume to cross-border fees and FX margin that a local acquirer would not charge.

Worked example with real numbers

Profile: a B2C SaaS company selling productivity software. Monthly card volume of $1.2M, average ticket $89, breakdown 35 percent US, 25 percent EU, 20 percent UK, 20 percent rest of world. Current setup: a single US acquirer at interchange plus 0.25 percent plus $0.10 per transaction, with cross-border surcharges passed through.

Current monthly cost on the $780,000 of non-US volume (65 percent of $1.2M):

- Interchange (cross-border consumer credit average): 1.50 percent of $780,000 = $11,700

- Cross-border network assessment: 0.80 percent of $780,000 = $6,240

- Acquirer markup: 0.25 percent of $780,000 = $1,950

- Per-transaction fixed: ($780,000 / $89) x $0.10 = $876

- FX margin embedded in settlement to USD: 1.5 percent of $780,000 = $11,700

Total non-US cost on a single US acquirer: approximately $32,466 per month, or 4.16 percent of non-US volume. Approval rate on non-US traffic: 81 percent. Of $780,000 attempted, $632,000 clears. The other $148,000 includes roughly $74,000 of recoverable good demand that the issuer declined on cross-border friction.

Switch to local acquiring: an EU acquirer for the 25 percent EU slice, a UK acquirer for the 20 percent UK slice, the US acquirer keeps the rest-of-world tail.

- EU acquirer (intraregional consumer credit average): 1.10 percent interchange, no cross-border surcharge, 0.20 percent markup, EUR settlement with no FX margin. On $300,000: $3,900 per month.

- UK acquirer (post-Brexit UK domestic cap): 1.20 percent interchange, 0.20 percent markup, GBP settlement with no FX margin. On $240,000: $3,360 per month.

- Rest-of-world ($240,000) stays on the US acquirer at the same all-in rate of about 4 percent: $9,600 per month.

Total non-US cost on local acquiring: approximately $16,860 per month. Monthly fee saving: $15,606. Annual fee saving: $187,272.

Approval rate on EU and UK volume lifts from 81 percent to roughly 88 percent based on processor benchmarks, recovering about $4,200 of additional clearing volume per month, or $50,000 per year.

Operator playbook

Seven moves to make this week, in order.

- Pull approval rate by issuer BIN country. Most processor dashboards expose this if you ask. Sort by volume. Any country above 5 percent of total volume with an approval rate more than 5 points below your US baseline is a candidate for local acquiring.

- Audit cross-border line items on your last 3 statements. Look for "International Service Assessment," "Cross-Border Transaction Fee," "ISA," or "IAF." Sum them. Divide by non-US volume. That is your cross-border surcharge rate, and it is the floor on what local acquiring can save you.

- Request quotes from 2 local acquirers per target region. In the EU: Adyen, Worldline, Nuvei. In the UK: Barclaycard, Worldpay UK. In Brazil: Cielo or Rede. Ask for interchange-plus pricing on intraregional categories with local settlement currency. Avoid blended pricing offers.

- Ask each acquirer about SCA exemption handling. Specifically: what fraud rate threshold do you maintain for TRA exemptions, and what percentage of my EU consumer auths can you route exemption-eligible. A real local acquirer answers with a number. A reseller hedges.

- Test with a traffic split before committing. Route 20 percent of EU traffic through the new local acquirer for 30 days. Compare approval rate, settlement timing, dispute rate, and net effective rate against the incumbent. The lift shows up by week 2.

- Negotiate FX margin separately. If you settle to USD from a EUR or GBP acquirer, the spread is a line item. Ask for a specific basis point margin over the ECB or Bank of England reference rate. Anything above 30 bps for $1M-plus monthly volume is negotiable.

- Build orchestration before scaling beyond two acquirers. Route based on issuer BIN country, not buyer billing address. A payments orchestration layer (Spreedly, Primer, Gr4vy, or in-house) sends each charge to the right acquirer in under 50 ms and gives you a single ledger.

Local acquiring is the single highest-impact move available to an international merchant. Nothing else recovers 3 to 8 points of approval rate without changing the product or the price.