TL;DR

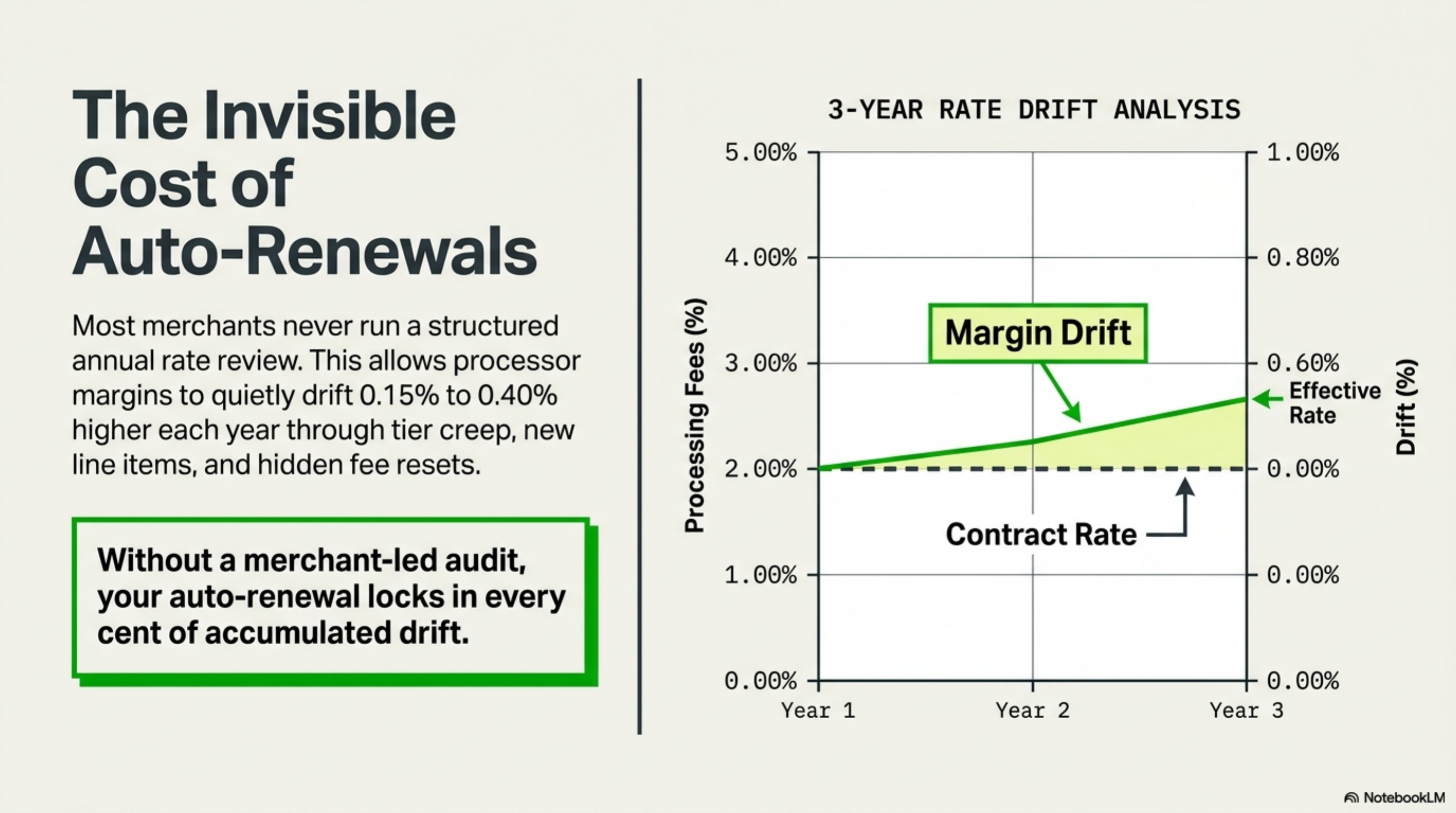

Most merchants never run a structured annual rate review. That is how processor margins drift 0.15 to 0.40 percent higher each year through tier creep, new line items, and quiet PCI fee resets. A 90-minute audit of 12 monthly statements catches the drift. Pull statements, calculate effective rate, compare against current Visa and Mastercard interchange schedules, then send a written repricing request. Merchants in the $500K to $5M monthly range typically recover $8,000 to $60,000 per year.

What this actually is

The annual rate review is a structured audit, run by the merchant, that compares every fee charged over the past 12 months against three reference points: the signed contract, the current interchange tables published by the card networks, and what a similar merchant would pay today.

It is not the renewal call from the processor's relationship manager. That conversation works backward from the processor's margin goal. The merchant-led review works forward from the actual numbers on the statement. The two paths produce different outcomes because they start from different incentives.

The mechanics rest on a separation that flat-rate marketing tends to blur. Every card transaction carries three cost layers. Interchange goes to the issuing bank and is set by the card networks. Assessments go to Visa, Mastercard, Discover, or American Express at a fixed percentage of volume. Processor markup goes to your processor and is the only piece you can negotiate. Federal Reserve payments research tracks the growth of U.S. card payment volume and documents the role of interchange in card economics. Visa publishes its U.S. interchange schedules quarterly. Mastercard publishes its rates and qualification criteria publicly.

An annual review exists because the first two layers are fixed by the networks while the third drifts. Tiered buckets get re-classified. PCI compliance fees creep from $99 to $199 annually. Cross-border assessments appear when a customer pays from a foreign-issued card. Statement fees, batch fees, and gateway fees show up after a contract anniversary, often within 60 days of the auto-renewal date.

Most merchant processing agreements auto-renew on a 1, 2, or 3 year cycle. Without an annual review, the auto-renewal locks in whatever rate the statement currently shows, including every cent of drift since signing. The processor's renewal notice usually arrives 30 to 60 days before the anniversary as a single page that does not break out the effective rate trend.

An annual rate review is a merchant-led audit of 12 months of processor statements against contract terms, current interchange schedules, and benchmark pricing.

How it works under the hood

A working review follows a fixed sequence. The discipline matters because each step depends on output from the prior one. Skipping any single step means a later step rests on an assumption rather than a number.

- Pull the last 12 monthly statements from the processor portal. Most processors retain statements for 18 to 24 months online; older statements require a request to support.

- Pull the original merchant processing agreement, every addendum, and the most recent renewal notice or rate change notification.

- Build a spreadsheet with 12 rows, one per month, and columns for gross sales, refunds, net volume, total interchange, total assessments, processor fees, and total fees billed.

- Calculate the effective rate per month as total fees divided by gross sales. Plot the trend across all 12 months.

- Pull the current quarterly interchange tables from Visa and Mastercard. Match your card mix (consumer credit, consumer debit, commercial, rewards, international) against the published rates.

- Identify any line item that was not in the original contract or that has increased over the year. Note the dollar amount and the first month it appeared.

- Build a one-page summary showing the 12-month effective rate trend, the contract terms, the benchmark from current interchange-plus quotes, and the dollar gap between current spend and benchmark.

- Send the summary to the processor's relationship manager with a written repricing request, a target rate, and a response deadline of 14 days.

The math underneath step 4 is what most merchants get wrong. The effective rate is not the contract rate. A merchant on a 0.20 percent markup over interchange-plus with a 1.85 percent weighted average interchange will run an effective rate near 2.05 percent before assessments. Add 0.13 percent in network assessments and 0.05 percent in per-item processor fees, and the realistic effective rate sits between 2.20 and 2.30 percent for a card-present retailer with a mixed consumer card portfolio.

Statement layout varies by processor. Look for three sections: a transaction summary showing gross volume and counts by card brand, an interchange detail listing each interchange category and its dollar cost, and a fees section showing processor-side charges. Some processors bury per-item fees inside the interchange line; others break them out. Pull the same line from each of the 12 statements to verify what you are summing.

Most merchants on tiered pricing run 0.50 to 0.90 percent above interchange-plus. The gap is invisible until a 12-month review puts the numbers side by side.

When the effective rate climbs above 2.50 percent on a card-present consumer-card book, the gap is markup, not interchange. Nilson Report data on processor economics shows average net processor margin on a small-to-mid merchant book sits between 0.25 and 0.55 percent. Anything above that range is a negotiation lever, not a market floor.

Calculate the effective rate every month, not every year. A 0.05 percent monthly drift hides inside a year and looks like a 0.60 percent surprise at renewal. The monthly calculation takes five minutes once the spreadsheet template exists.

Where it goes wrong for operators

Five patterns account for most of the drift between the rate on the contract and the rate on the statement. Each has a specific dollar impact at a typical merchant volume tier.

Pattern 1: Tier reclassification

On a tiered pricing plan, the qualified rate covers a narrow set of consumer debit and standard consumer credit transactions. Anything else (rewards, corporate, keyed, international) routes to mid-qualified or non-qualified at 0.80 to 1.50 percent higher. At $400,000 monthly volume with a 40 percent reward-card mix, the difference between a clean interchange-plus passthrough and a tiered downgrade pattern is roughly $1,600 to $2,000 per month.

Pattern 2: Annual PCI compliance fee

The line item typically appears in the anniversary month at $99 to $250. Some processors charge a separate PCI non-compliance fee of $19.95 to $49.95 monthly until the merchant completes the self-assessment questionnaire. A retailer who missed two SAQ deadlines and one annual PCI fee will see roughly $600 to $800 in unexpected line items by year end.

Pattern 3: Cross-border and international service assessments

Visa charges a 0.40 to 1.20 percent international service assessment depending on settlement currency. Mastercard charges a 0.60 to 1.00 percent cross-border fee. Most processors pass these through with an additional markup of 0.10 to 0.30 percent. A retailer who started accepting foreign-issued cards mid-year will see the international assessment line grow month over month without any signed change to the contract.

Pattern 4: Auto-renewal with a price adjustment

The contract typically includes a clause that allows the processor to adjust pricing with 30 days written notice at any time. The notice often appears as a single line on the statement. A 0.10 percent across-the-board markup increase on $1.2 million monthly volume is $14,400 in annual margin transferred from merchant to processor.

Pattern 5: Hidden batch, statement, gateway, and chargeback fees

Each one is small ($5 to $35 monthly). Stacked, they add $400 to $900 per year. None of them show up in the summary the processor sent at signing. A typical statement carries 8 to 14 separate processor-side line items; the contract summary listed three.

Stacked across all five patterns at a $1 million monthly volume merchant, combined drift typically runs 0.20 to 0.50 percent above the rate at signing. That is $24,000 to $60,000 in annual margin transfer that does not require any explicit fee increase notice or signed amendment.

A processor that resists sending a flat itemized list of all monthly fees in writing is signaling that one or more of these patterns is active on your account. The written list is the leverage point; do not accept a verbal walk-through.

Worked example with real numbers

Profile: B2B parts distributor on a tiered pricing plan. $850,000 monthly card volume. $1,250 average ticket. Card mix: 60 percent commercial card, 30 percent consumer credit, 10 percent debit. Current contract: 2.45 percent qualified, 2.85 percent mid-qualified, 3.15 percent non-qualified, plus $0.15 per item.

Pull 12 statements. The monthly effective rate ran 2.72 percent in January, climbed to 2.91 percent by June, hit 3.04 percent in October. Twelve-month average: 2.87 percent. Total card volume across 12 months: $10.2 million. Total fees billed: roughly $293,000.

Step one. Separate interchange from markup. Commercial card interchange for a B2B distributor with no Level 2 or Level 3 data submission runs between 2.50 and 2.95 percent under current Visa schedules. With Level 2 data fields populated (customer code, tax amount): 2.05 to 2.20 percent. With Level 3 data (line items, freight, shipping): 1.90 to 2.05 percent.

Step two. Estimate the markup. Pure passthrough interchange-plus at 0.20 percent markup with Level 2 data submission produces an effective rate of roughly 2.40 percent. Difference from the current 2.87 percent 12-month average: 0.47 percent. Annual savings on $10.2 million volume: roughly $48,000.

Step three. Add Level 3 data submission through a B2B-optimized gateway. Estimated effective rate: 2.10 to 2.20 percent. Annual savings versus the current contract: $70,000 to $80,000.

Step four. For the same distributor on a flat-rate plan at 2.9 percent plus $0.30 per item, the math runs differently. $10.2 million in volume produces $295,800 in percentage fees plus $2,448 in per-item fees on 8,160 transactions: $298,248 annually. The interchange-plus path with Level 3 data saves roughly $77,000 against flat-rate.

The merchant has two requests on the table for the relationship manager. First, move from tiered to interchange-plus at 0.20 percent and $0.10 per item. Second, enable Level 2 and Level 3 data transmission through the gateway, which most processors charge $20 to $40 per month to activate. The activation fee pays for itself inside the first week of transactions.

This distributor moved from a 2.87 percent effective rate to 2.18 percent over two billing cycles after a documented review. Recovered margin in year one: $68,000. The repricing took 14 business days from written request to first repriced statement. No contract termination required.

Operator playbook

Run this sequence over one week. None of the steps require new software, outside consultants, or a contract termination.

- Pull 12 monthly statements and your original processing agreement from the portal. Save them in one folder, named by month.

- Build a 12-row spreadsheet with columns for gross sales, refunds, net volume, total interchange, total assessments, total processor fees, and monthly effective rate. Calculate the effective rate per month and plot the trend.

- List every line item billed in the most recent statement that is not in the original contract. Common offenders: PCI compliance, PCI non-compliance, statement fee, batch fee, network access fee, monthly minimum fee, regulatory product fee, IRS reporting fee.

- Pull the current Visa and Mastercard quarterly interchange tables. Calculate a weighted average interchange for your card mix. The difference between your effective rate and that weighted average is the all-in markup, which combines processor margin, assessments, and per-item fees.

- Get two written interchange-plus quotes from competing processors for your monthly volume tier. Use the signed rate sheet, not the verbal pitch. A typical competitive quote at $500K to $2M monthly is 0.15 to 0.30 percent over interchange plus $0.05 to $0.10 per item.

- Send the relationship manager a one-page written repricing request that includes the 12-month effective rate trend, the list of new line items, the competitive benchmark, the target rate, and a 14-day response deadline.

- If the response misses the deadline or proposes a one-time credit instead of a rate reset, request a formal early termination fee quote and a current account balance in writing.

- Compare 12 months of projected savings under the competing quote against the early termination fee plus switching costs ($500 to $5,000 depending on hardware and integration). If savings exceed costs, move. If they do not, the threat of moving usually still produces a smaller repricing.

"The repricing request only works in writing. Verbal renegotiations leave no paper trail and almost never produce more than a $50 monthly statement credit."