TL;DR

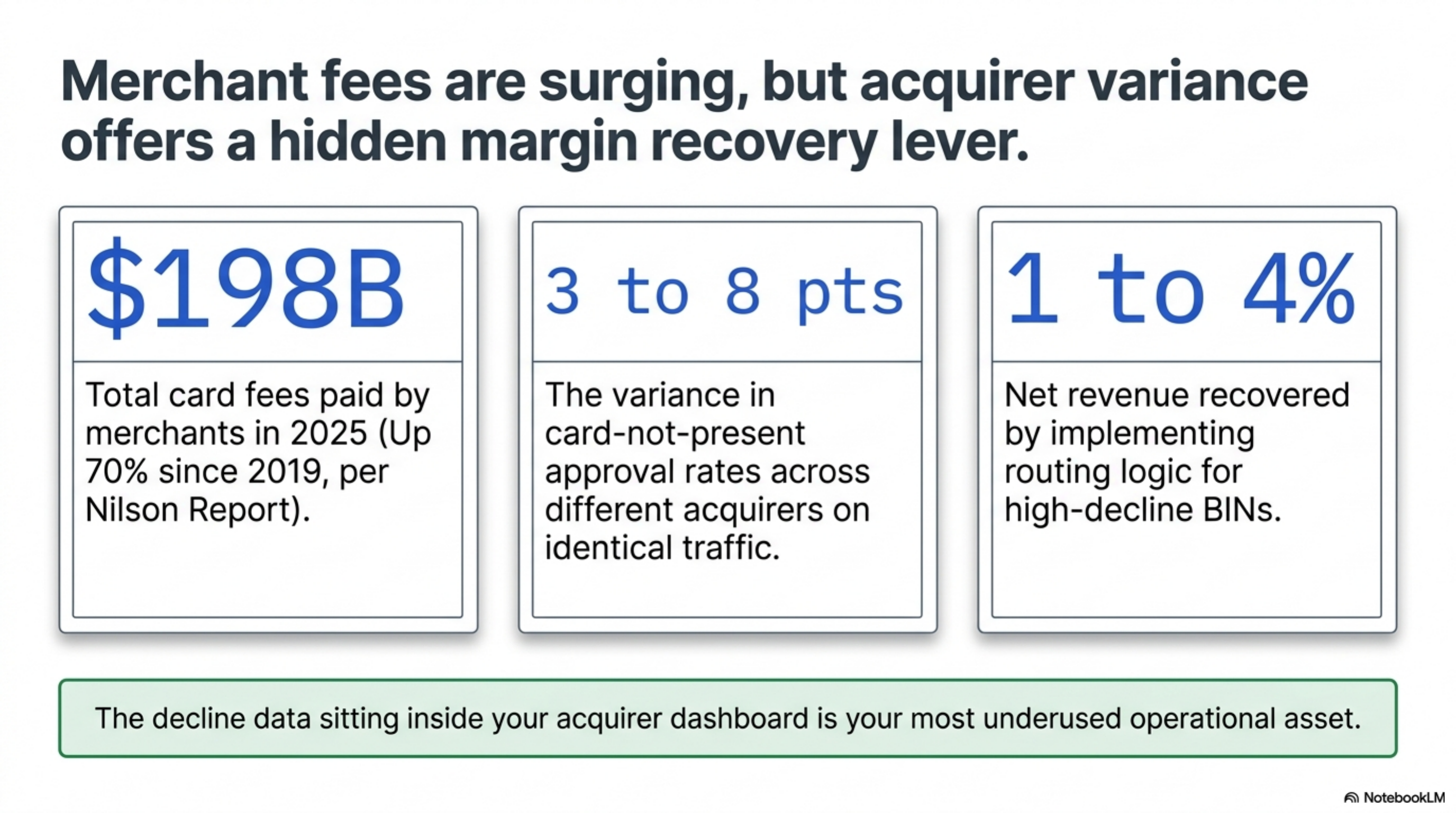

BIN routing is the practice of selecting which acquirer handles a card transaction based on the first six to eight digits of the card number. Card-not-present approval rates vary 3 to 8 percentage points across acquirers on identical traffic, and the gap widens on international BINs. Operators processing 500,000 dollars per month or more can recover 1 to 4 percent of net revenue by routing high-decline BINs to a second acquirer. The first move is pulling a BIN-level decline report from your gateway and segmenting it by issuer country and response code.

What this actually is

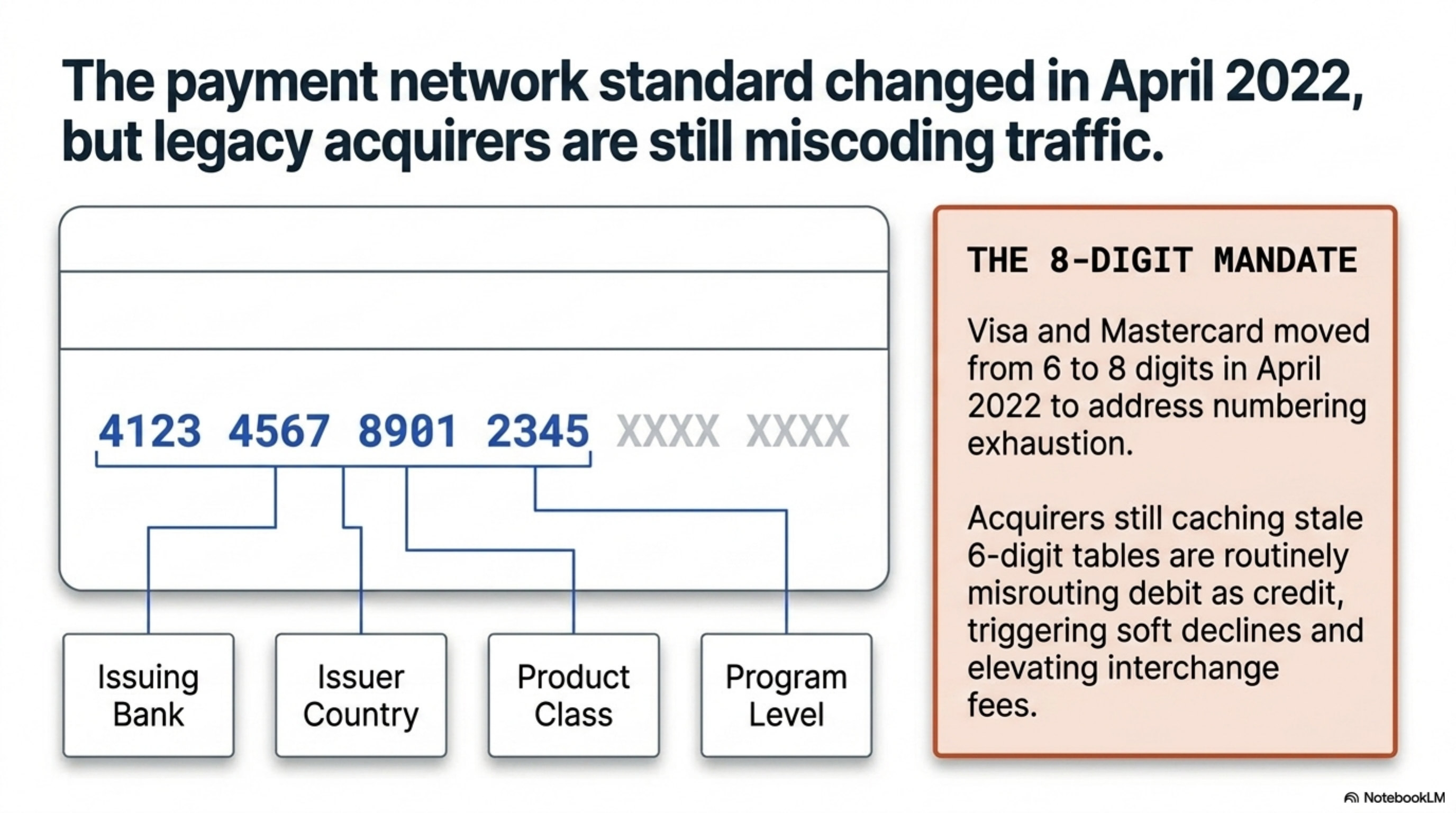

A Bank Identification Number, or BIN, is the leading six digits of a payment card account number. The card networks moved to an eight-digit standard in April 2022 to address numbering exhaustion, and acquirers that have not refreshed their BIN tables route some cards using stale assumptions. Each BIN identifies the issuing bank, the issuer country, the product class (debit, credit, prepaid), and the program level (consumer, commercial, premium rewards). Visa and Mastercard publish BIN range files to licensed acquirers and processors, with the rate criteria laid out in the public Visa interchange schedules and the Mastercard interchange documentation.

BIN routing, in operator terms, is the decision about which acquirer receives a given authorization request. If your gateway connects to two acquirers, you can send Visa consumer debit BINs from one issuer to Acquirer A and Visa commercial credit BINs from another issuer to Acquirer B. The Federal Reserve's payments study series tracks aggregate card volumes but does not publish per-BIN approval data; that data sits inside acquirer dashboards and remains one of the most underused assets in card-not-present operations.

Why this matters: not every acquirer has the same issuer relationships, network token coverage, or fraud rules. A BIN that returns soft declines (Visa response code 05, "Do not honor") at Acquirer A may approve cleanly at Acquirer B, and the only way to know is to run the test and read the report. The Nilson Report tracks North American card-not-present volume that now runs in the trillions of dollars annually, and a 100 basis point approval lift on a slice of that traffic is a meaningful operator lever.

BIN routing sends each card transaction to the acquirer most likely to approve it, based on the first six to eight digits of the card number.

How it works under the hood

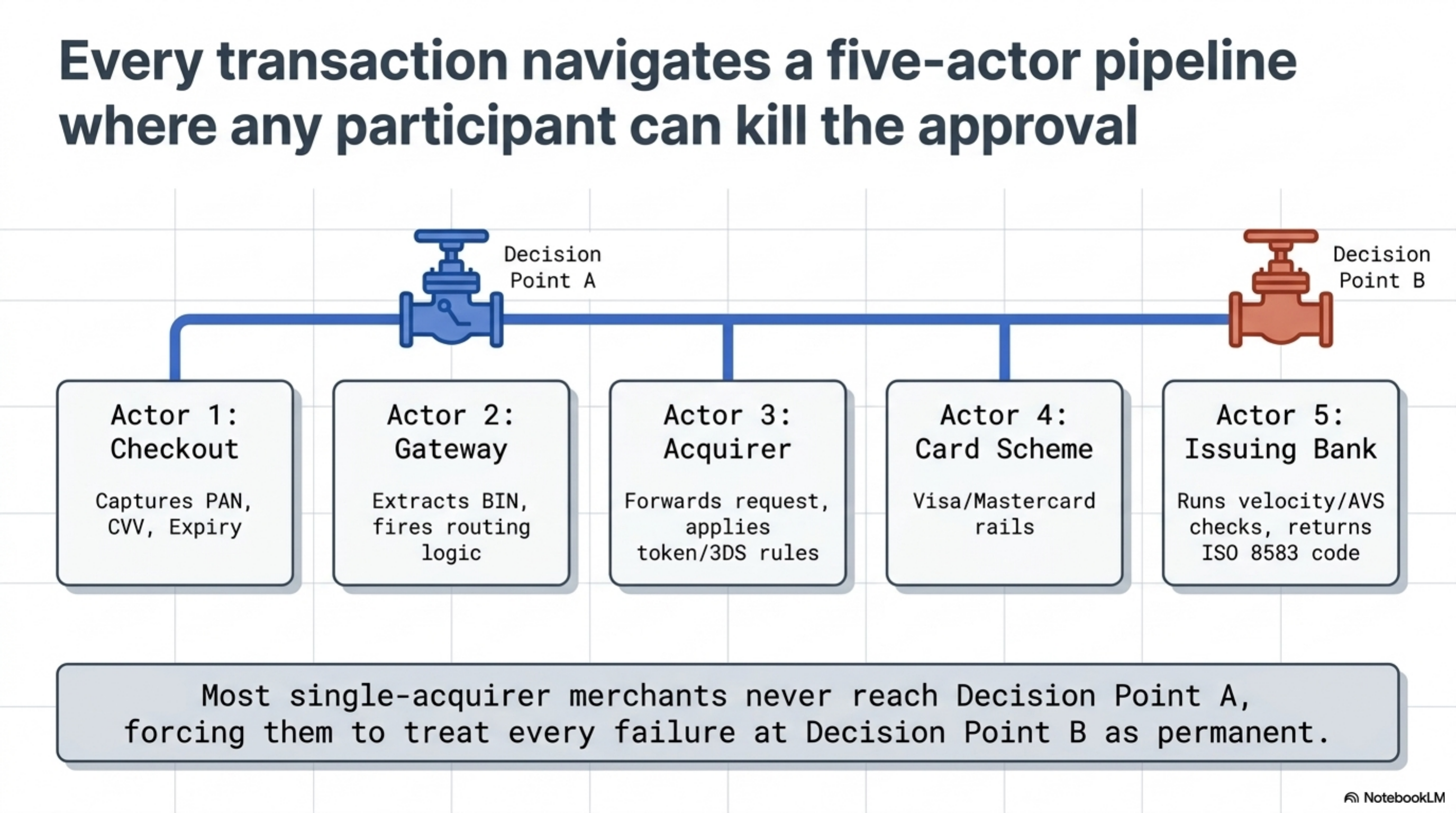

The flow that turns a checkout button click into an approved authorization passes through five distinct actors. Each one has the option to deflect, downgrade, or decline the transaction.

- Cardholder submits card data at your checkout. Your gateway or orchestration layer captures the PAN, expiry, CVV, and billing address. The first six to eight digits are extracted and used to look up the BIN attributes (country, product, issuer name) from a reference table maintained against Visa and Mastercard files.

- Gateway routing logic fires. If you have a single acquirer, the request goes there. If you have multiple acquirers or an orchestrator like Spreedly, Primer, Gr4vy, or a homegrown rules engine, the routing layer inspects the BIN, the amount, the currency, the customer history, and the routing rules you wrote. The output is one acquirer endpoint.

- Acquirer receives the authorization request and forwards it to the appropriate card scheme (Visa or Mastercard rails). The acquirer's BIN tables determine the routing path, the interchange category that will apply at settlement, and whether the transaction qualifies for network tokens or 3-D Secure 2.x friction-light flows.

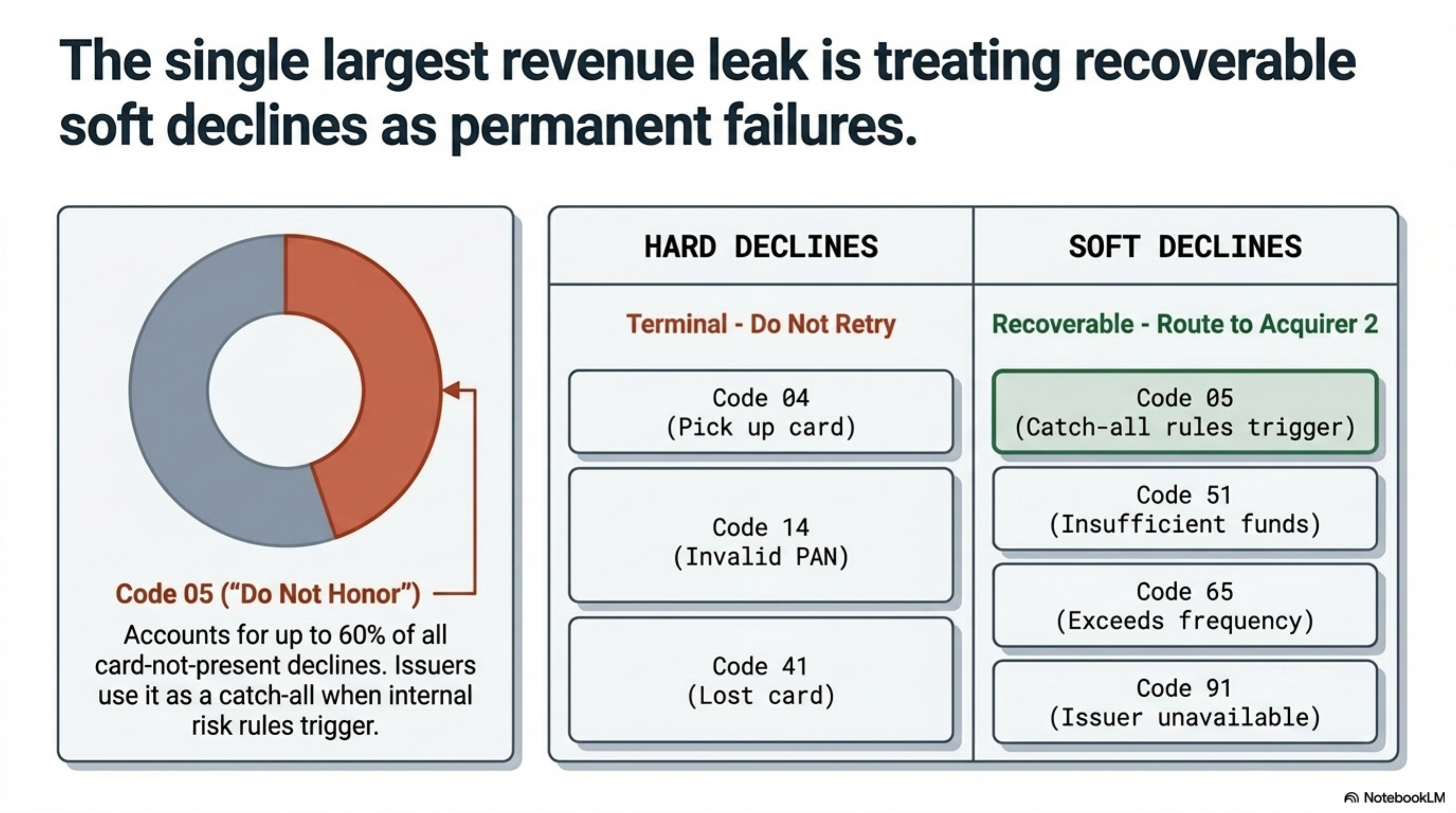

- Issuing bank decisions the request. The issuer runs its own rules: velocity checks, AVS match, CVV match, device intelligence, prior decline history with the merchant descriptor, and amount risk. The issuer returns an ISO 8583 response code. Approved is 00. Soft declines are 05 (do not honor), 51 (insufficient funds), 65 (exceeds withdrawal frequency), and 91 (issuer unavailable). Hard declines are 04 (pick up card), 14 (invalid PAN), and 41 (lost card).

- Gateway returns the result to your application. If you have routing logic, a soft decline can be retried on a second acquirer, sometimes with a different MID descriptor, and sometimes with stepped-up authentication via 3-D Secure 2.

The decision points are steps 2 and 5. Most merchants on a single acquirer never reach a routing decision, and they treat every soft decline as final. That is the lost margin.

Where it goes wrong for operators

Five patterns account for almost all of the missed approvals at sub-orchestration merchants. Each one is fixable, but only after you can see it in the data.

1. Exclusivity clauses in the processor contract. Many full-stack processors include a primary-acquirer clause that requires you to route all qualifying volume through them. Stripe, Adyen, and Braintree contracts vary; the public terms reference volume commitments that are negotiable above 1 million dollars in monthly volume. At 850,000 dollars monthly, an exclusivity clause that prevents adding a second acquirer can cost 1.5 to 3 percent of authorized volume in lost approvals, roughly 12,000 to 25,000 dollars per month.

2. Stale BIN tables. The card networks transitioned to 8-digit BINs in April 2022, but some processors and many ISO-resold gateways still cache 6-digit tables. The result: a BIN that should route as Visa consumer debit gets coded as Visa consumer credit, lifting interchange by 50 to 100 basis points and sometimes triggering soft declines because the issuer flags the mismatch. At 500,000 dollars monthly, a 60 basis point misrouting cost runs about 36,000 dollars per year.

3. Cross-border BINs treated as fraud. A U.S. merchant accepting a card issued in the UK or Germany sees that BIN as foreign. If your gateway risk rules auto-decline non-US BINs above a threshold, you are walling off the highest-AOV segment. Cross-border interchange runs higher per the Visa fee tables, but the AOV uplift usually justifies the rate. At a 145 dollar AOV, a 4 percent approval uplift on a 12 percent international slice nets roughly 5,000 dollars per month per 500,000 dollars of volume.

4. Soft-decline retry loops with no backoff. Some acquirers will let your system retry a 05 immediately. Visa's Integrity Fees penalize repeat retries on the same authorization within 24 hours. The fee stacks per offending transaction. A merchant retrying every soft decline three times on the same MID can rack up several thousand dollars per month in fees that never appear on a line item; they roll into the interchange dump.

5. Network token misalignment. If your card-on-file vault stores PAN but the acquirer expects network tokens, recurring auths get downgraded to non-tokenized, and approval rates fall 2 to 5 points on rebills alone.

Worked example with real numbers

Profile: a direct-to-consumer skincare brand running on a Shopify store with a custom checkout. Vertical: health and beauty subscriptions. Monthly card volume: 850,000 dollars. Average ticket: 145 dollars. Mix: 78 percent card-not-present new orders, 22 percent recurring subscription rebills. Current setup: single acquirer (a major full-stack processor) at a blended 2.65 percent plus 10 cents per authorized transaction. International order share: 14 percent.

The merchant pulled a 90-day BIN-level decline report and found three patterns. First, overall approval rate of 84.2 percent, with a sharp dip to 71 percent on rebills. Second, response code 05 accounted for 41 percent of all declines, concentrated on six issuer BINs that together represented 19 percent of attempted volume. Third, international BIN approval ran at 68 percent versus 87 percent for US BINs.

The math on the routing fix: 850,000 dollars per month at 84.2 percent approval equals 715,700 dollars of net authorized volume. Lift overall approval to 88.0 percent through dual-acquirer routing on the high-decline BINs, and net authorized volume becomes 748,000 dollars, a gain of 32,300 dollars per month or roughly 388,000 dollars per year in incremental gross merchandise volume.

Net contribution after the second acquirer's processing cost (roughly 2.75 percent plus 10 cents on routed traffic, slightly higher than the primary): incremental gross margin at the merchant's 58 percent gross margin level runs about 225,000 dollars per year. The cost of the orchestration layer plus the second acquirer's monthly minimum is approximately 24,000 dollars per year. Net annual benefit: about 200,000 dollars.

The breakeven on building the routing logic, even on a homegrown rules engine, lands inside one quarter at this volume tier.

Operator playbook

Run this sequence over the next four weeks. None of these steps require a new processor relationship to start; they require data and a list.

- Pull a BIN-level decline report from your gateway for the last 90 days. The exact line items to ask for: BIN (8-digit), issuer country, product type, attempt count, approval count, decline count, response code distribution. If the gateway cannot produce this, escalate to your acquirer relationship manager and ask in writing.

- Segment the report by issuer country and response code. Separate US versus international BINs. Within each, isolate response codes 05, 51, 65, and 91. These are your recoverable buckets. Codes 04, 14, and 41 are not recoverable through routing.

- Identify your top 20 high-decline BINs. These are the BINs that together represent 60 to 80 percent of your soft declines. Calculate the lost authorized volume at each BIN. Anything above 5,000 dollars per month per BIN is a routing candidate.

- Verify your BIN tables are 8-digit. Ask your processor in writing: do you maintain Visa and Mastercard BIN tables at the 8-digit standard effective April 2022? A hedged answer or a no is grounds for an RFP.

- Audit your contract for exclusivity language. Search for primary acquirer, minimum processing commitment, right of first refusal, and exclusive. If any are present, calculate the cost of compliance versus the cost of waiver. At 850,000 dollars monthly, the waiver cost is usually negotiable.

- Request a second acquirer trial or onboard an orchestration layer. Quote two to three orchestrators (Spreedly, Primer, Gr4vy) and one direct second-acquirer trial. Define the routing rules in writing before signing.

- Implement soft-decline retry with backoff. Retry response code 05 once on a second acquirer within 4 to 10 seconds. Do not retry hard declines. Log every retry outcome to a structured decline-recovery table.

- Review weekly for the first 60 days. Track approval rate, response code distribution, and incremental volume. Anything below a 2 point lift after 30 days means the routing rules need tuning, not abandonment.