TL;DR

A contactless tap from a plastic card or an Apple Pay, Google Pay, or Samsung Pay wallet runs on the same card-present interchange as a chip dip. The networks do not add a wallet surcharge, and Apple bills the card issuer, not you. The cost problem is downstream: terminals that downgrade taps to keyed rates, processor line items like 'digital wallet access,' and tokenized debit that gets routed to the expensive network. Pull last month's statement and check the qualification column before you accept any 'NFC fee.'

What this actually is

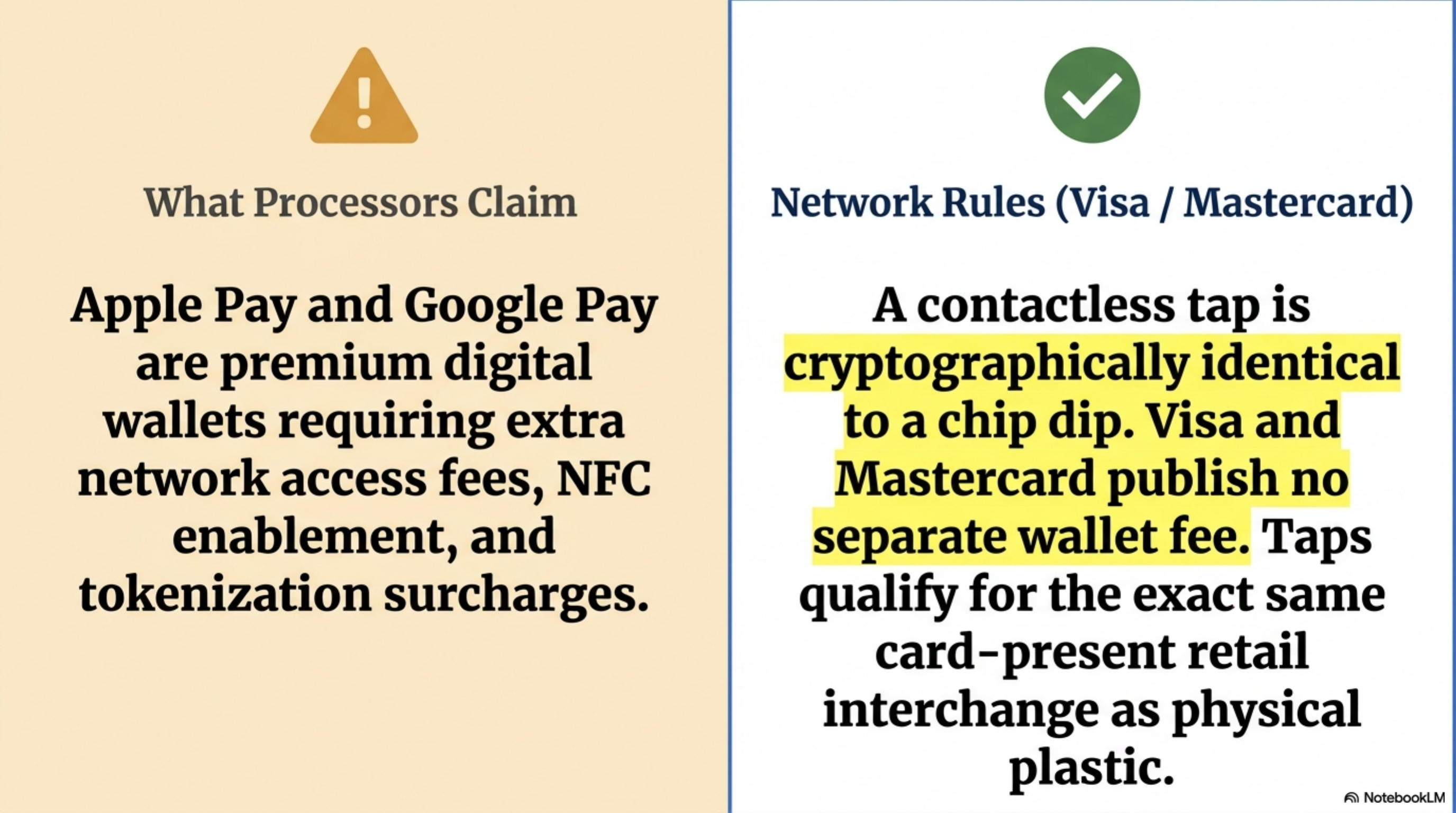

Contactless payments use the EMV contactless specification, the same chip-card cryptography that runs a dipped transaction, transmitted over NFC instead of contact pads. A tapped plastic card, an Apple Pay transaction, a Google Pay transaction, and a Samsung Pay transaction all generate a one-time cryptogram that the terminal sends to the acquirer and then to the network for authorization. From the network's perspective, these are card-present transactions that meet the highest authentication tier.

Mobile wallets add one layer on top: tokenization. The phone never stores or transmits the real 16-digit Primary Account Number. Instead, the wallet provisions a Device Primary Account Number through the Visa Token Service or Mastercard Digital Enablement Service, and the terminal sees that token plus a transaction cryptogram. The Federal Reserve's payments studies document the steady migration of in-person card volume toward this contactless flow.

Network rules treat a properly captured contactless tap as card-present for both interchange and chargeback liability. The published Visa interchange schedules and the Mastercard interchange rates and criteria assign tapped consumer credit to the same retail or supermarket categories as chip-and-PIN, not to a separate 'wallet' bucket.

Contactless and mobile wallet fees are the costs a merchant pays when a customer taps a physical card or a phone to complete a purchase, billed at card-present interchange rates set by Visa and Mastercard.

How it works under the hood

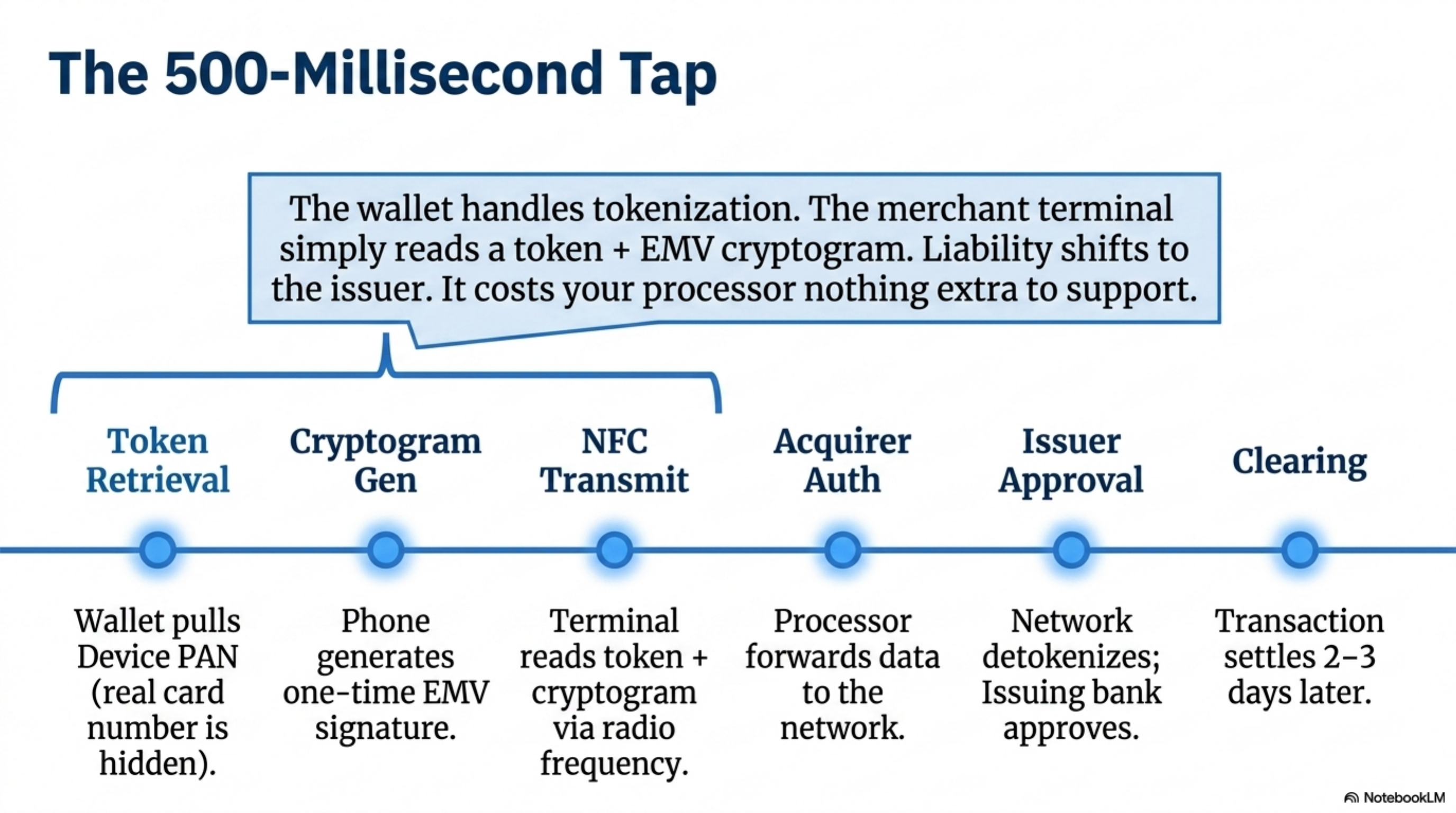

When a customer holds a phone to a contactless reader, six things happen inside roughly 500 milliseconds. Knowing each step is how you spot the place a fee gets added that should not be there.

- Token retrieval. The wallet pulls the Device PAN that the issuer provisioned during card enrollment. The merchant terminal never sees the real card number.

- Cryptogram generation. The secure element on the phone signs the transaction with a one-time cryptogram. This is the same EMV process a chip card runs during a dip.

- NFC transmit. The terminal reads the token, cryptogram, and a short data set over NFC. The card brand on the customer side determines the routing rail.

- Acquirer authorization. Your processor sends the authorization to the network. The network detokenizes through the Visa Token Service or MDES and forwards the real PAN to the issuer.

- Issuer approval. The issuing bank approves or declines. Liability for fraud sits with the issuer for any properly captured contactless transaction with a valid cryptogram.

- Clearing and interchange. The transaction settles two to three business days later. Interchange is assessed against the qualified card-present rate for the product type.

For tokenized debit, Regulation II applies the same way it does to a swiped or dipped debit transaction. Regulated debit issuers, banks with over $10 billion in assets, are capped at 21 cents plus 0.05 percent of the transaction plus a 1 cent fraud adjustment. Merchants also retain the right to route the transaction over a competing debit network, even when the wallet defaults to Visa or Mastercard rails.

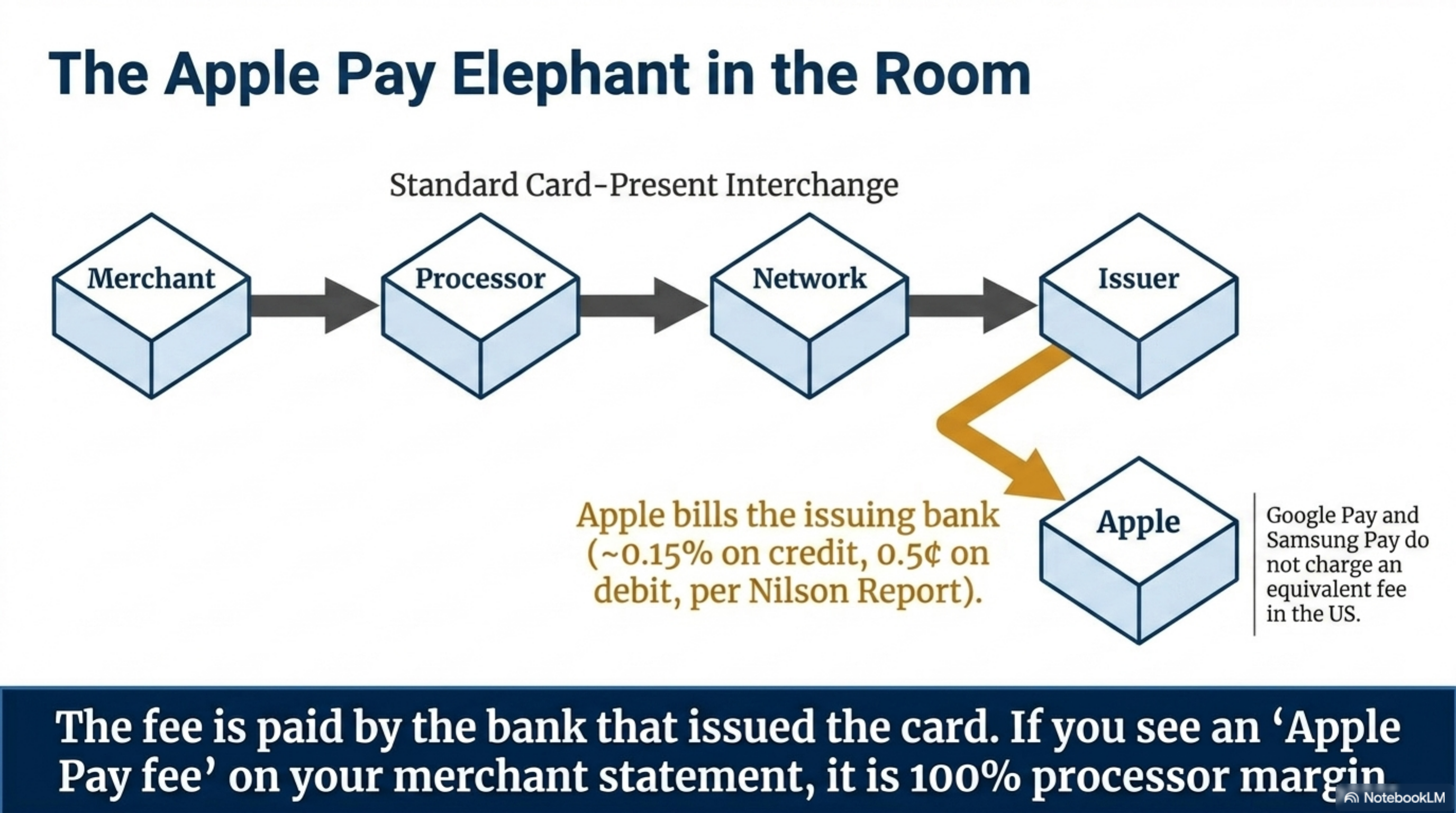

Apple's wallet has one extra wrinkle: Apple bills the issuer roughly 0.15 percent on US credit transactions and about 0.5 cents on US debit, per multiple Nilson Report summaries. The fee is paid by the bank that issued the card, not by you. Google Pay and Samsung Pay do not charge an equivalent fee in the United States.

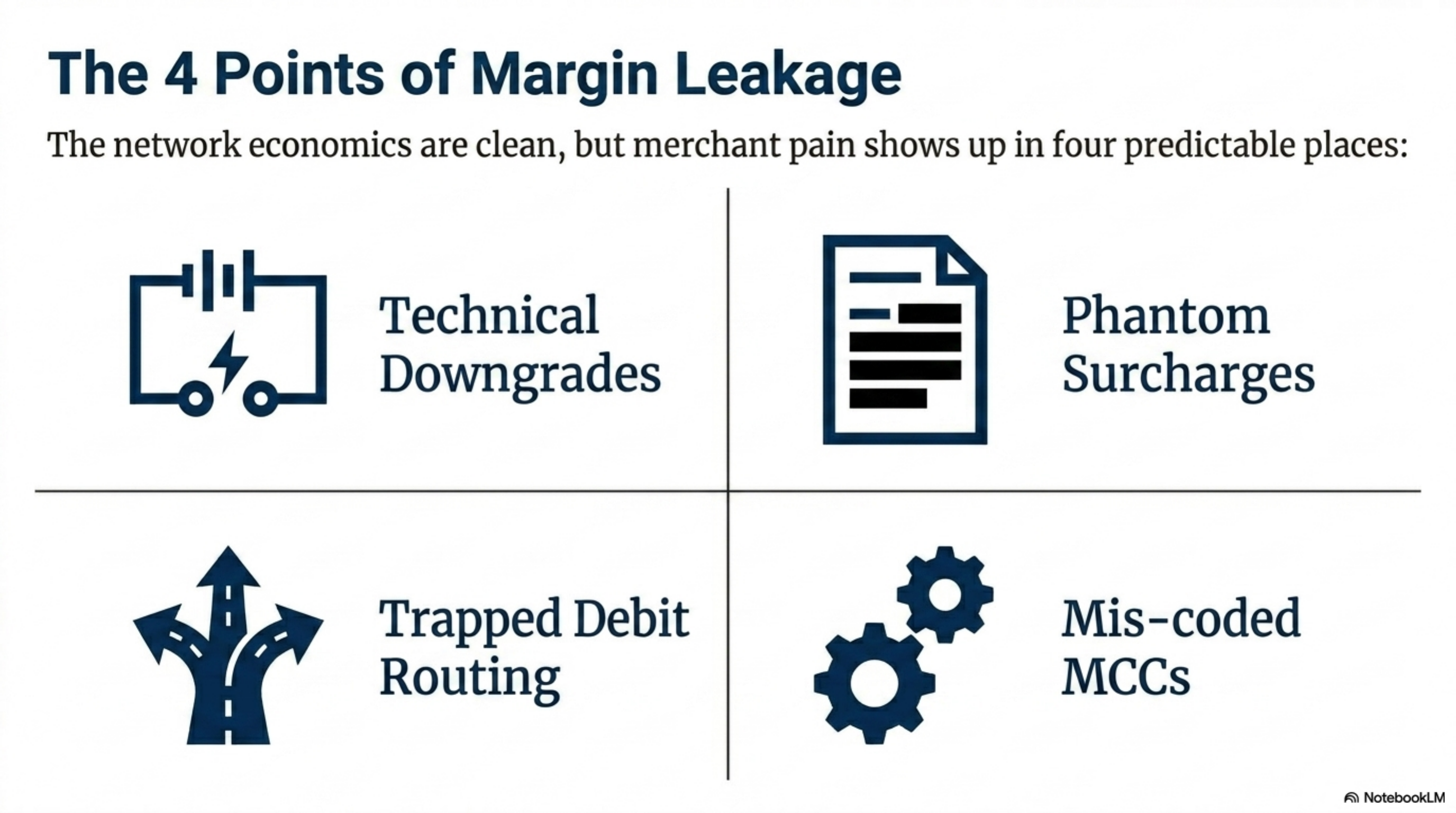

Where it goes wrong for operators

The network economics of contactless are clean. The pain shows up in four predictable places.

1. Downgrade to keyed or card-not-present rates. If the terminal is not properly EMV-contactless certified, or the cryptogram fails to transmit cleanly, the transaction can clear as a magnetic-stripe or keyed entry. That moves a Visa consumer credit transaction from CPS Retail at roughly 1.51% plus 10 cents to EIRF at 2.30% plus 10 cents, an 0.79 percent jump. At $300,000 in monthly card volume, that is about $2,370 per month in avoidable interchange.

2. Processor 'digital wallet' surcharges. Several processors list line items labeled 'mobile wallet access,' 'NFC enablement,' or 'tokenization fee.' None of these are network-published. They are processor markup on a product that costs them nothing extra to support. We have seen these range from 0.05 percent to 0.25 percent.

3. Debit routing left on the expensive rail. Tokenized debit can default to Visa or Mastercard global rails. If you do not enable PINless debit routing over networks like Maestro, Star, NYCE, or Pulse, you pay the full regulated cap on every regulated debit tap and well above that on unregulated debit. The Fed's 2023 Reg II amendment clarified that this routing right applies to card-not-present and tokenized transactions, not only swipes.

4. Mis-coded MCC affecting interchange tier. Visa and Mastercard publish lower interchange for supermarkets, fuel, utilities, charities, and quick-service restaurants. If your business should sit in one of those categories but your processor coded you as general retail, every contactless tap clears at the wrong rate. The gap can be 0.30 percent to 0.65 percent on consumer credit.

Worked example with real numbers

Take a 14-location quick-service coffee operator in the Pacific Northwest. Monthly card volume: $1.4 million across all stores. Average ticket: $9.40. Card mix: 62 percent contactless (split roughly evenly between tap-enabled cards and Apple Pay or Google Pay), 24 percent chip dip, 10 percent swipe, 4 percent online ahead-orders. Current processor: tiered pricing at 1.79 percent qualified, 2.49 percent mid, 3.19 percent non-qualified, plus 12 cents per transaction, plus a 0.15 percent 'mobile wallet enablement' fee on all NFC transactions.

Approximate monthly cards: 148,936. Contactless transactions: 92,340. The wallet enablement line alone runs 0.15 percent times the $868,000 contactless volume, or $1,302 per month. The tiered plan also misclassifies roughly 18 percent of contactless taps as mid-qualified because the processor groups all rewards cards into mid by default, even when they tapped cleanly under CPS Retail interchange.

Add PINless debit routing for the 38 percent of card mix that is debit. Roughly half of those qualify as regulated debit at the Reg II cap. Routing more of the tokenized debit traffic over Star or Pulse trims another estimated 0.08 percent off the effective rate, or about $1,120 per month. The combined impact is roughly $7,840 per month on a base the merchant previously thought was 'just what cards cost.'

Most merchants on tiered plans pay 0.30 to 0.50 percent more on contactless than they would on a transparent interchange-plus plan, almost entirely through downgrade definitions and surcharge line items the contract does not flag.

Operator playbook

This is the sequence that wins. Run it in order, do not skip.

- Pull the last 90 days of statements as PDFs. You need three months because seasonal mix shifts and one month is not enough to spot a pattern.

- Find the line items labeled 'digital wallet,' 'mobile wallet,' 'NFC access,' 'tokenization,' or 'Apple Pay.' Total them and divide by your contactless volume. That is your wallet markup. Then ask your processor in writing for the Visa or Mastercard bulletin number that authorizes the line item.

- Audit qualification columns. On a tiered statement, look at the share of contactless volume in mid-qualified or non-qualified buckets. If it is over 5 percent, downgrades are systematic and your terminal config or pricing plan is wrong.

- Verify your MCC. Pull the four-digit Merchant Category Code from page one of your statement. Compare it to the Visa MCC list and the Mastercard Quick Reference Booklet. If you operate a QSR, supermarket, fuel, charity, or utility but the MCC reads 5999 or 5311, that is a billable error.

- Enable PINless debit routing. Ask your processor which debit networks they support and whether your account is configured for least-cost routing. If they say it costs extra to enable, that is a flag. Reg II protects this right.

- Move to interchange-plus pricing or surcharge pricing if your model supports it. Pull two competing quotes that itemize interchange separately from the processor markup. Reject any quote that bundles 'NFC,' 'PCI,' or 'wallet' fees into the markup column without a line-item breakdown.

- Re-test the terminals. Run a tap, a chip dip, and a swipe on each device and confirm the transaction shows in the qualified column the next day. If a tap clears as keyed, the device firmware or the contactless reader configuration is broken.

- Document the negotiation in writing. When you negotiate the new schedule, get the wallet enablement fee removed in the schedule A, not in a side email. Side emails do not survive a sales-rep change.