TL;DR

Processors freeze merchant funds when chargeback ratios cross 0.9 percent, volume jumps 3x a 90-day trailing average, or underwriting flags a vertical-risk shift. Most accounts release 50 to 90 percent of held funds within 30 to 90 days, but only if the merchant supplies documentation in the first 72 hours. The recovery sequence is direct: escalate past the support queue, file a written dispute citing your processor agreement, and prepare for a 5 to 10 percent rolling reserve as a release condition.

What this actually is

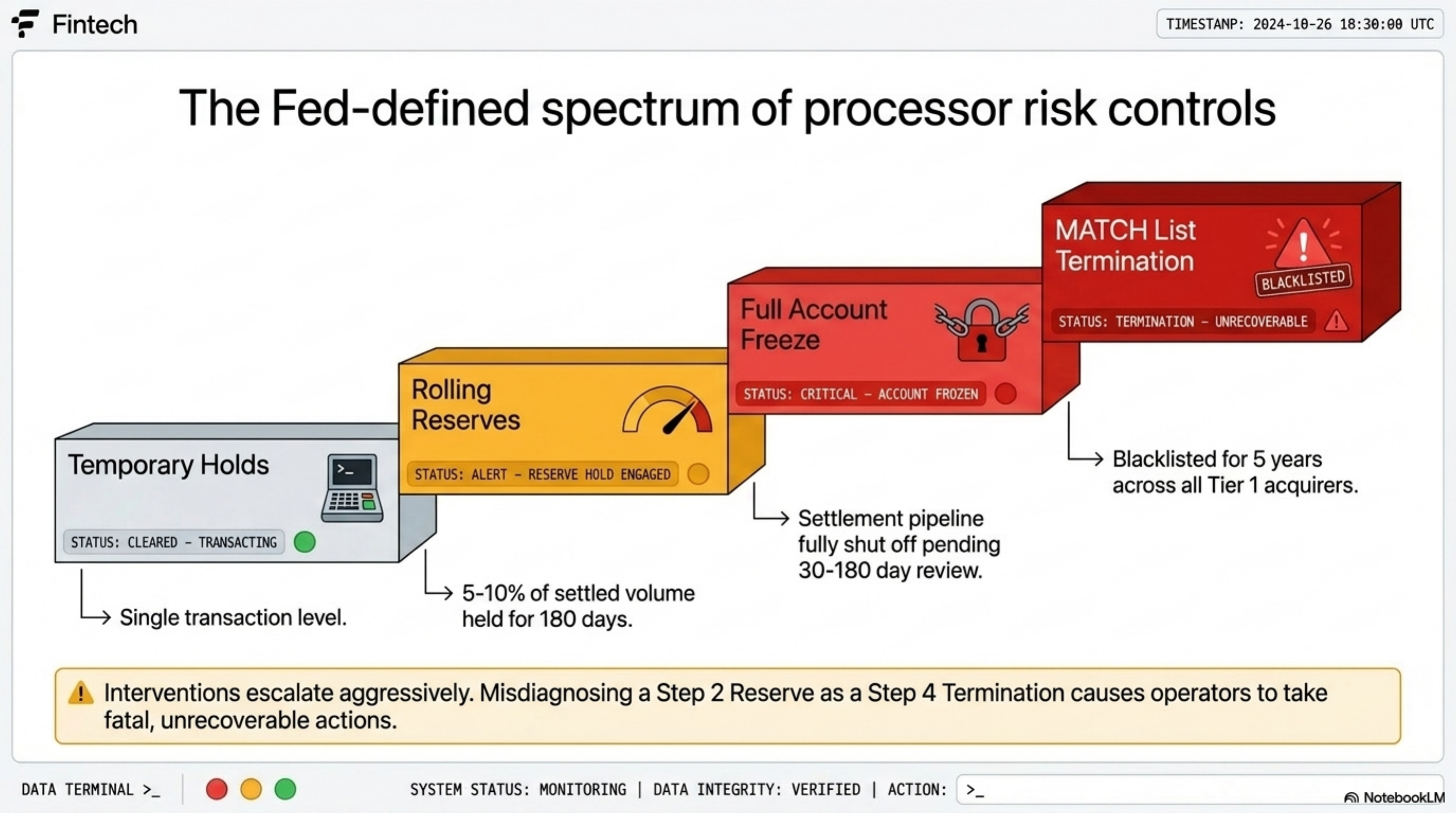

A frozen account is different from a delayed payout, a rolling reserve, or a chargeback hold. The Federal Reserve's payments oversight materials describe processor risk controls as a spectrum: temporary holds on individual transactions, rolling reserves on a percentage of settled volume, full account freezes pending review, and termination with terminal indemnification. Each step shifts more of the cash flow risk from the acquirer to the merchant.

When a processor freezes funds, the merchant's settlement queue stops releasing. New authorizations may still capture, but the cash sitting at the acquirer never hits the operating account. The processor cites a section of the merchant agreement, usually the "right to suspend funding" or "risk management" clause, and starts a review window of 30 to 180 days.

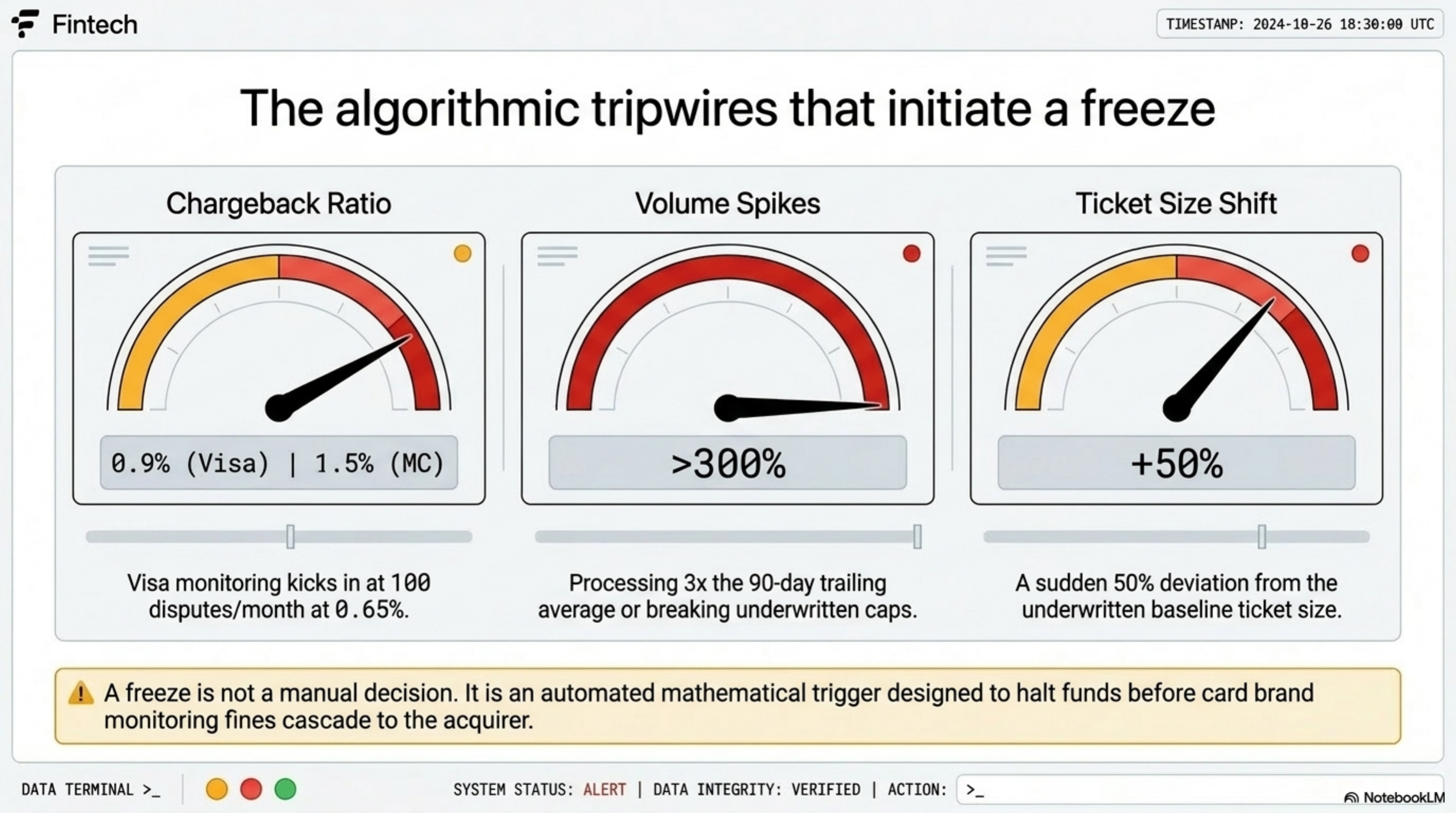

Visa's published rules on merchant monitoring set the chargeback threshold that triggers acquirer-side action at 0.9 percent of monthly transactions, with the Visa Dispute Monitoring Program kicking in at 100 disputes per month at a 0.65 percent ratio. Mastercard runs a parallel framework called the Excessive Chargeback Program with thresholds at 1.5 percent. Most processor freezes happen before the merchant ever appears on a card brand monitoring list. Acquirers freeze first to protect their own exposure.

Frozen funds are merchant settlements a payment processor holds beyond the normal funding cycle due to risk review, chargeback exposure, refund volume, or a reserve clause in the merchant agreement.

How it works under the hood

The mechanics are simple once you separate the trigger from the action. A trigger is the event that flags the account. The action is what the processor does to the settlement queue.

Common triggers:

- Chargeback ratio crosses 0.9 percent on Visa or 1.5 percent on Mastercard for two consecutive months.

- Monthly volume rises 200 to 300 percent above the underwritten cap on the original application.

- Average ticket size shifts 50 percent or more from the underwritten baseline.

- A single transaction is flagged by the AML or sanctions screen.

- The business model changes (new product lines, new geographies) without re-underwriting.

- A bank counterparty calls about a possible kiting or layering pattern.

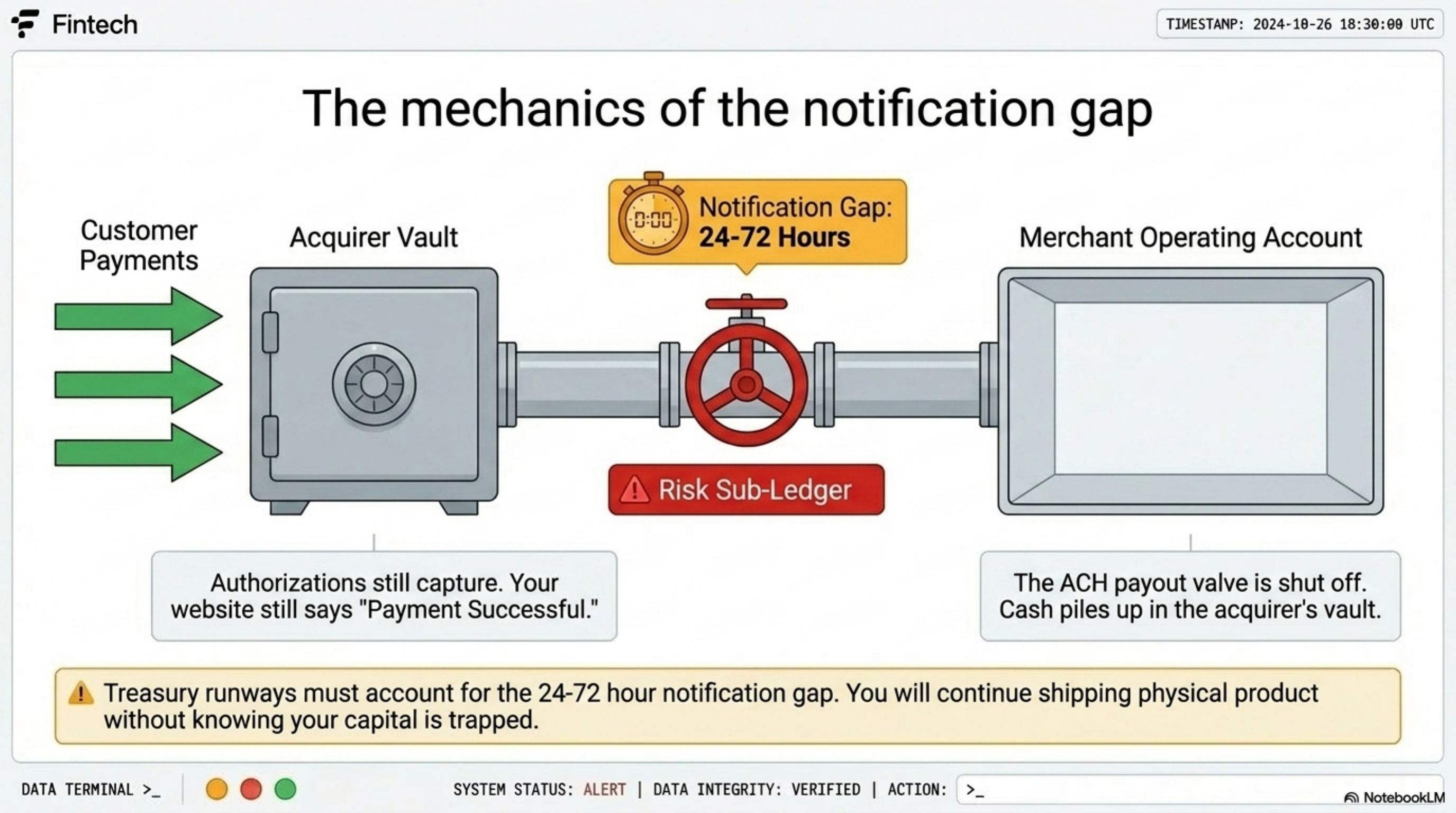

Once triggered, the processor's risk team places the merchant identifier (MID) on a watchlist. The action varies by acquirer, but the funding queue is typically suspended within 1 to 3 business days. The cash that would have settled to the operating account stays at the acquiring bank, segregated in a reserve sub-ledger. This is not the same as a chargeback hold against a single transaction, which only ties up the disputed amount plus a fee. A full freeze affects every dollar in the settlement pipeline, including transactions that have already cleared the issuer and are waiting on the ACH window to deliver to the operating account.

The notification gap is the most damaging part. The Stripe Services Agreement permits holds for the duration necessary to investigate, with notification "as soon as practicable" but no specific window committed. The PayPal User Agreement permits holds of at least 21 days on flagged transactions and longer for ongoing reviews. The Square Seller Agreement describes reserves and holds that can extend up to 90 days as a standard, with longer periods available for risk reviews. Build your treasury runway assuming you may not know about a freeze for 24 to 72 hours after it starts.

The review then runs. Depending on the processor, a risk analyst pulls the last 90 to 180 days of transaction data, requests supporting documents (invoices, fulfillment proof, supplier agreements, customer support tickets, bank statements), and decides whether to release, partially release, or terminate. Risk teams generally work in queue order, so the documentation packet that lands first and is organized cleanly tends to clear faster than one delivered piecemeal across multiple emails.

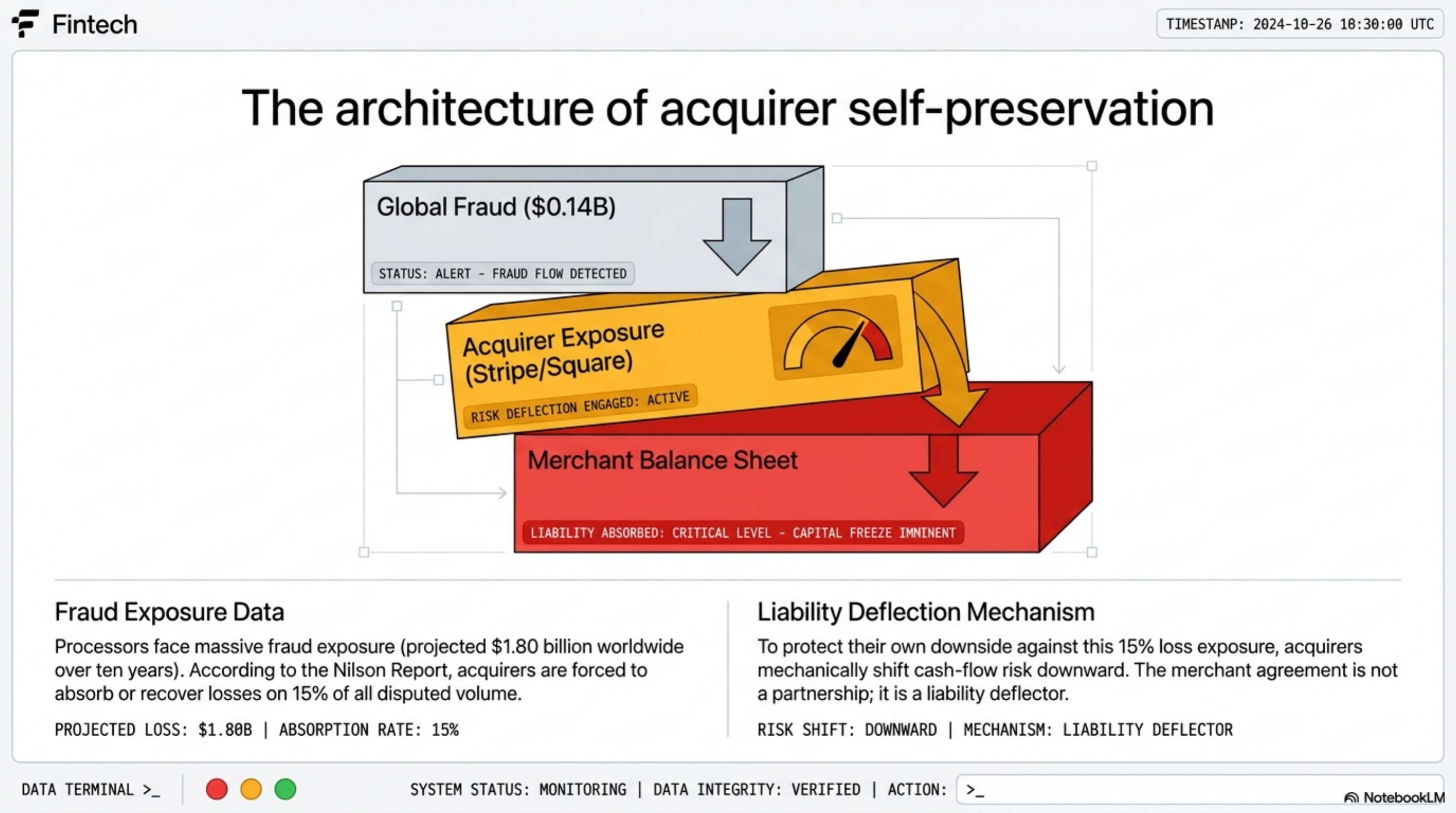

Most merchants get a partial release: the bulk of funds released back, with a 5 to 10 percent rolling reserve held for 180 days against future chargeback exposure. According to Nilson Report annual chargeback data, processors recover or absorb the chargeback losses on roughly 15 percent of disputed volume, so the reserve math protects the acquirer's downside on the trailing window.

The contract clause that controls all of this is rarely read at signing. Most merchant agreements give the acquirer unilateral authority to freeze, reserve, or terminate "upon reasonable belief" of risk, with no objective threshold defined.

Where it goes wrong for operators

Three patterns cause the most damage.

Pattern 1: The 270-day clause. Most merchant agreements allow a hold for up to 270 days. The Square Seller Agreement cites a 90-day standard hold window. The Stripe Services Agreement references holds that can extend up to the duration necessary to complete an investigation. That open-ended language is the lever the processor uses to stretch a 30-day review into 90 days, and a 90-day review into 180. At a $250,000 monthly volume, a 180-day hold parks roughly $1.5 million in settlement cash if compounded across multiple funding cycles.

Pattern 2: The mid-freeze switch. The merchant tries to move to a new processor mid-freeze. The new processor's underwriting pulls the merchant's history from the MATCH list (Mastercard's Member Alert to Control High-Risk Merchants file). Once a merchant is on MATCH, most Tier 1 acquirers will not board the account. The freeze functions as a soft termination even when the processor says it is only a review. At a $500,000 monthly volume, 60 days of denied alternatives compounds the cash flow gap into seven figures.

A MATCH listing stays on file for 5 years. The acquirer that filed it must remove it, which only happens if you dispute and win. Dispute success rates are not publicly reported and most operators find them low. Treat any mid-freeze processor switch attempt as a permanent banking-relationship decision, not a vendor swap.

Pattern 3: The combative email. The operator sends angry messages before pulling the contract. Risk analysts see hundreds of merchant disputes per month. The ones that move fast have a specific subject line ("Formal dispute under Section X.X of Merchant Agreement, MID #######"), a documented timeline, and supporting documents organized as PDF attachments. The ones that stall use phrases like "you are stealing my money." Risk teams forward those to legal, who then takes 30 to 90 days to respond.

The carry cost of a freeze scales with the operator's cost of capital. A small DTC operator bridging the gap with credit cards or a merchant cash advance commonly absorbs 25 to 50 percent annualized financing costs on the bridge. On $100,000 monthly volume, that translates to a few thousand dollars in interest for a 30-day freeze, roughly mid-five figures for a 90-day freeze, and high-five figures for a 180-day freeze stacked with a rolling reserve. The exact number depends entirely on what financing instrument the operator uses to cover payroll and supplier obligations while the cash is parked at the acquirer.

Worked example with real numbers

Merchant profile: direct-to-consumer e-commerce, sells consumer electronics, monthly volume $180,000, average ticket $85, current processor Stripe at 2.9 percent plus 30 cents per transaction. The merchant ran a Black Friday promotion and processed $620,000 in 9 days, a 3.4x lift over the trailing 90-day average. Two days after the promo ended, Stripe flagged the MID and froze the next $145,000 in settlements under the risk management clause of the Stripe Services Agreement.

Math on the freeze:

- Pre-freeze run rate: $180,000 per month, settling on a 2-day rolling basis.

- Promo volume processed: $620,000 over 9 days.

- Already settled before freeze: $475,000.

- Held at freeze: $145,000.

- Scenario A (full release after review): $145,000 released at day 35.

- Scenario B (partial release with 10 percent rolling reserve): $130,500 released at day 28, $14,500 held 180 days.

- Scenario C (extended review with chargebacks emerging): $145,000 held 90 days, then $130,500 released, $14,500 reserved 180 days.

Working capital impact at an assumed 25 percent annual cost of capital (a reasonable approximation for a small DTC operator bridging payroll with a business credit card or a moderate merchant cash advance): scenario A costs roughly $3,500, scenario B costs $4,300, scenario C costs $8,900. If the operator's financing cost is closer to 50 percent annualized (typical for short-duration MCA bridges), each number roughly doubles.

The merchant pulled the Stripe agreement within 1 hour of the freeze notification, identified Section 8 (Risk Management), filed a written dispute via certified email by end of day 1, and compiled fulfillment proof for the entire $620,000 promo (shipping confirmations, tracking numbers, customer order timeline) by day 2. Documentation was submitted as a single ZIP file labeled with the MID on day 3. Stripe partially released $130,500 on day 28, with a 10 percent rolling reserve on the remaining $14,500 for 180 days. Total cash flow impact: $4,300. Had the merchant escalated late or sent combative emails, the same case sits in scenario C at $8,900.

The merchant's recovery cost a fraction of the alternative because the documentation arrived inside 72 hours and the dispute cited a specific contract section. Risk analysts move faster on disputes that read like internal escalations, not customer complaints. Two practical follow-ups make the difference between a clean partial release and a longer review: confirm in writing that the documentation packet is considered complete, and request a named risk analyst contact rather than a generic disputes alias. Without those two steps, the case can recycle back into the general queue when the analyst rotates off shift, costing another 7 to 14 days.

Operator playbook

- Pull your merchant agreement within 1 hour of the notification. Find the "risk management," "right to suspend funding," or "reserve" clause. Quote the section number in every subsequent email.

- Send one written dispute, by email, to the disputes inbox and your account manager. Subject line format: "Formal dispute, MID #######, Section X.X." Keep the body under 200 words. Attach the contract clause, the freeze notification, and a timeline.

- Pull statements for the last 90 days. Mark every transaction over $1,000, every chargeback, and every refund. Build a single PDF, labeled with the MID.

- For volume spikes, compile fulfillment proof: shipping confirmations, tracking numbers, customer service logs, refund policy screenshots, supplier invoices showing inventory was on hand.

- Ask the risk team three questions in writing: (a) what is the review window, (b) what documentation closes the review, (c) what reserve percentage will release the held funds. Get the answer in writing before agreeing to anything.

- Do not switch processors during the freeze. A switch triggers a MATCH lookup that may end with both processors declining you. Keep the original relationship until the freeze resolves.

- Open a backup MID with a second acquirer before any future volume spike. Cost: $500 to $2,000 in setup and ongoing minimum fees. Value: prevents the next freeze from killing 100 percent of your cash flow.

- If the freeze extends past 60 days, retain a payments-specialist attorney. The threat of arbitration (most agreements waive jury trial and require AAA arbitration under the AAA Commercial Arbitration Rules and Fee Schedules) is often enough to move a stalled case, though outcomes vary by acquirer and case facts.