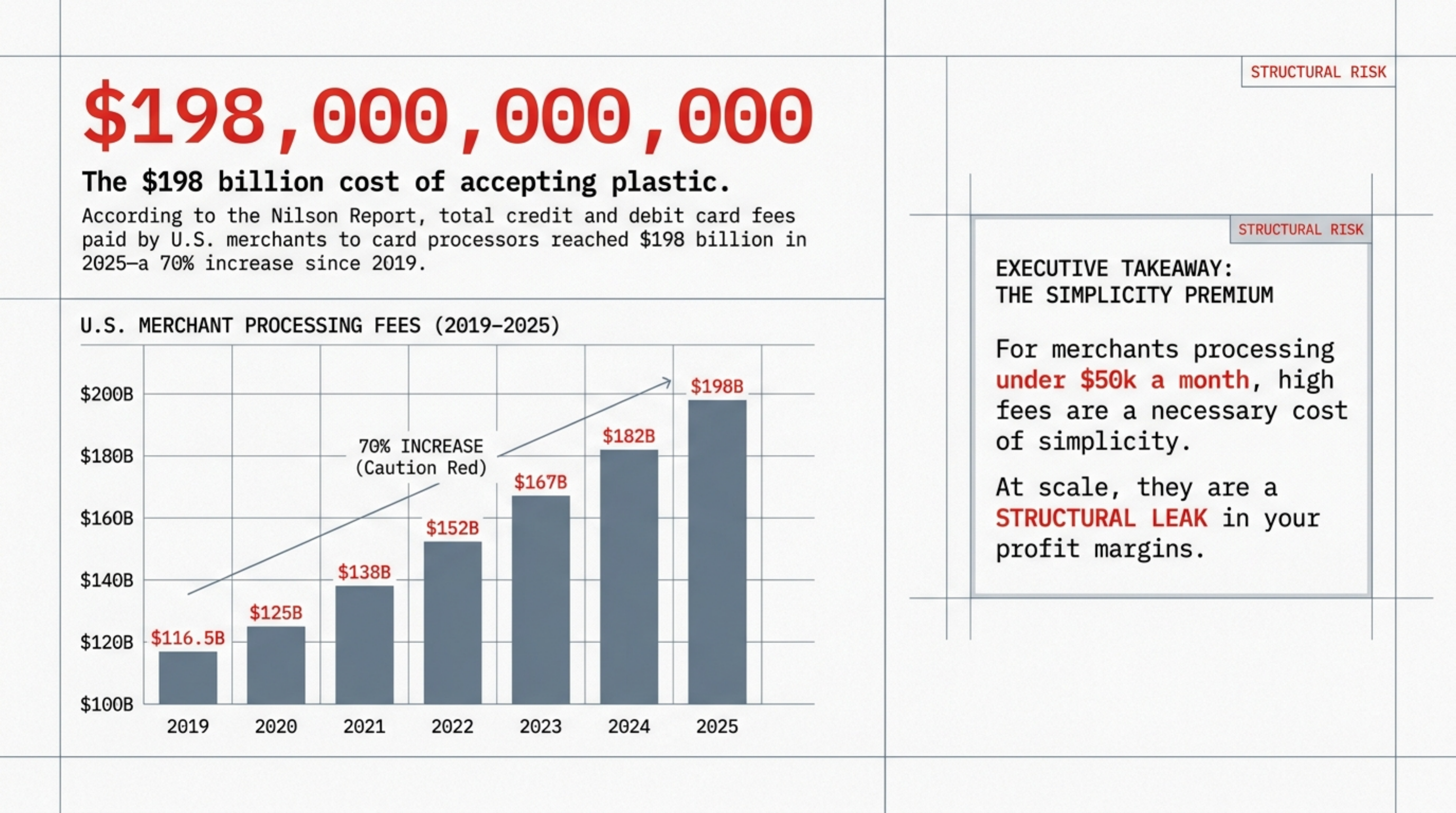

TL;DR

IC++ pricing passes the card network's wholesale interchange and assessment fees straight to the merchant, then adds a separate processor markup on top. For merchants doing more than $50,000 in monthly card volume, IC++ usually runs 0.30 to 0.80 percent cheaper than a flat-rate plan like Stripe or Square. The trap is the markup line, where padded basis points, monthly platform fees, and PCI surcharges add up fast. Pull your last three statements and check the effective rate before signing anything.

What this actually is

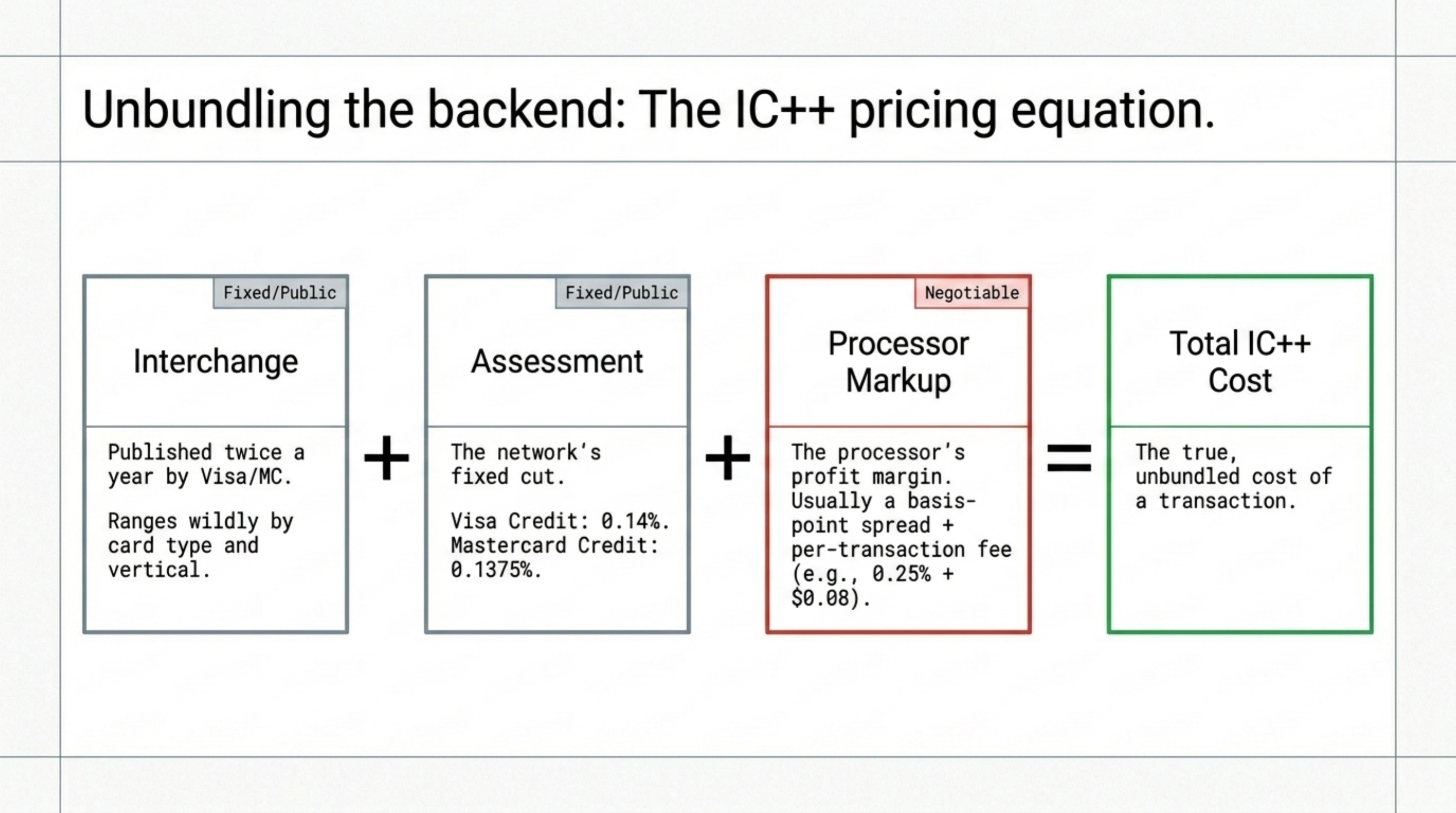

IC++ stands for Interchange Plus Plus. The first "plus" is the card network's assessment fee, which is the percentage Visa, Mastercard, Discover, and American Express charge on every transaction that crosses their rails. The second "plus" is the processor's markup, expressed as a basis-point spread plus a per-transaction fee. According to the Federal Reserve's payments studies, interchange accounts for roughly 70 to 80 percent of what most merchants pay in card fees, with the remainder split between network assessments and processor margin.

Interchange itself is set by the card networks, not by the processor, and the rates are published openly twice a year. Visa's interchange schedule and Mastercard's interchange rates and criteria are public PDFs updated in April and October. The schedules list hundreds of interchange categories segmented by vertical, card type, and authorization method.

On an IC++ statement, every transaction shows three line items: the interchange rate the card network charged, the assessment fee (currently 0.14 percent for Visa credit and 0.1375 percent for Mastercard credit), and the processor's markup. Flat-rate plans like Stripe and Square bundle all three into one blended percentage, which is why those merchants pay 2.9 percent plus 30 cents on every transaction whether the card is a basic Visa debit or a premium Visa Infinite. IC++ exposes the components so the merchant can see what the network charged versus what the processor added.

IC++ pricing is a card-acceptance model where the merchant pays the published interchange rate, the network assessment, and a separately negotiated processor markup on every transaction.

How it works under the hood

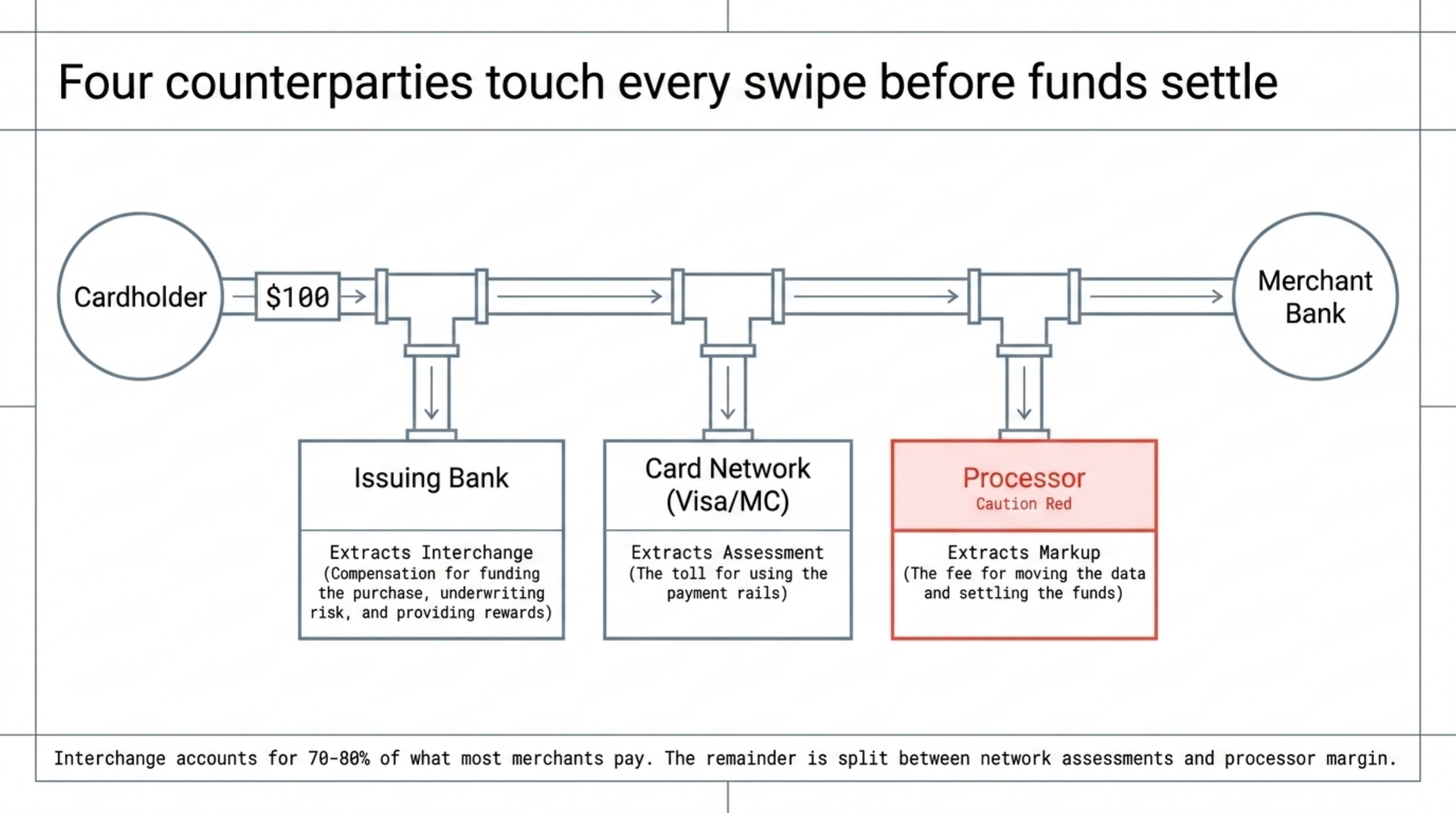

A card transaction touches four counterparties before funds settle: the cardholder's issuing bank, the card network, the processor, and the merchant's acquiring bank. IC++ pricing makes each counterparty's cut visible on the statement. Here is the flow for a $100 Visa Infinite swipe at a sit-down restaurant:

- The card network publishes the interchange rate. Visa's restaurant interchange for Visa Infinite Signature credit currently runs around 2.10 percent plus $0.10, per the public schedule.

- The issuing bank collects that interchange as compensation for funding the cardholder's purchase, underwriting risk, and providing rewards.

- The card network bills the merchant's processor for the assessment fee. Visa credit charges 0.14 percent of the transaction amount; Mastercard credit charges 0.1375 percent.

- The processor adds its negotiated markup. A competitive IC++ deal at $250,000 monthly volume typically runs 0.20 to 0.40 percent plus $0.08 to $0.12 per transaction.

- The acquiring bank settles the net amount (transaction minus all three fees) to the merchant's bank account, usually T+1 or T+2 depending on the contract.

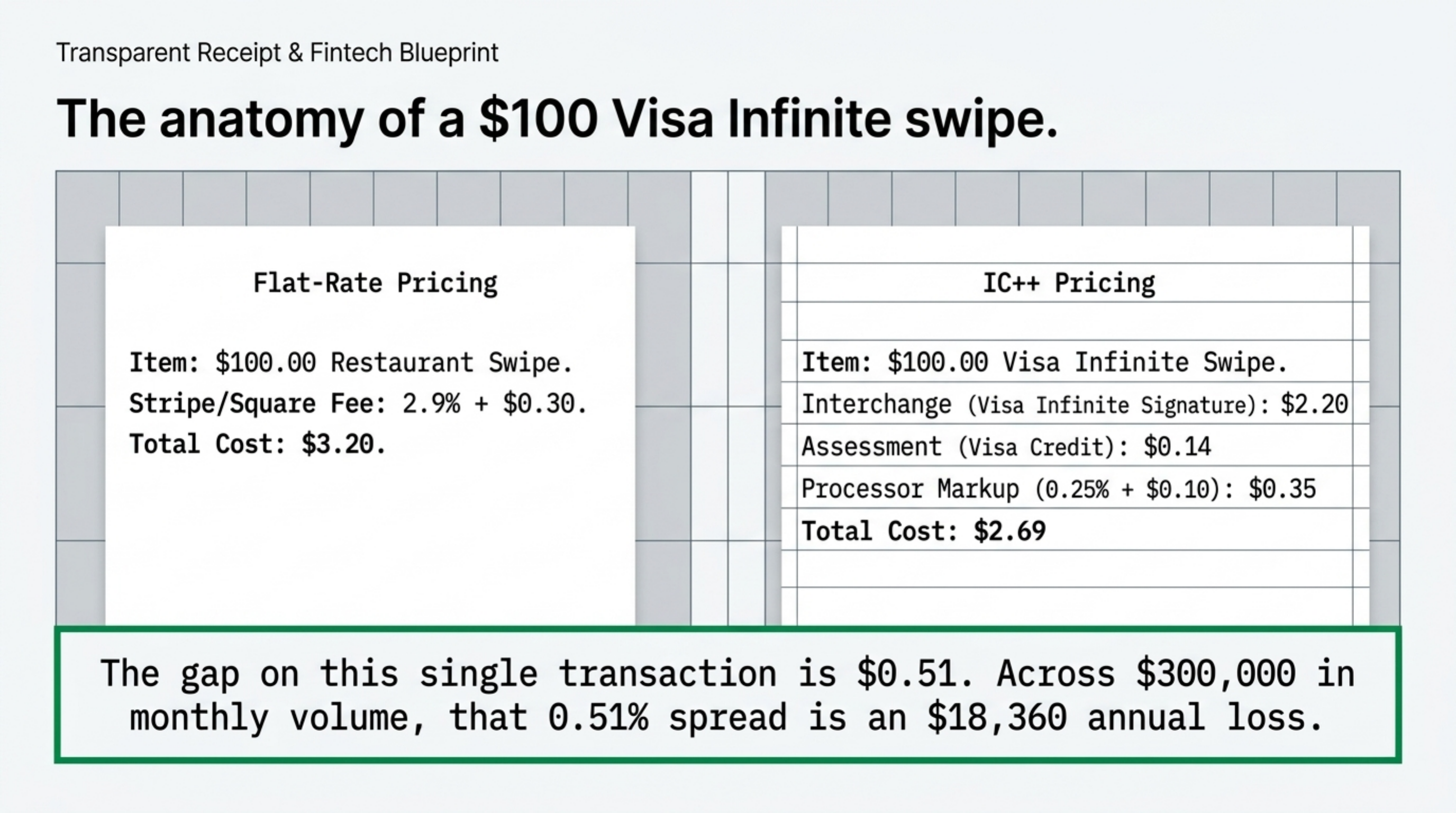

The math on that single $100 Visa Infinite swipe under IC++: interchange of $2.20, assessment of $0.14, and processor markup at 0.25 percent plus $0.10 working out to $0.35. Total fees: $2.69, effective rate 2.69 percent. The same $100 transaction on a Stripe flat-rate plan costs $3.20 (2.9 percent plus $0.30). The gap is $0.51 per transaction, or 0.51 percent of volume. Across $300,000 in monthly card volume, that gap works out to $1,530 a month, or $18,360 a year.

The structural reason IC++ usually wins above $50,000 monthly volume is that flat-rate processors price for the most expensive card their merchants typically run. Stripe's 2.9 percent has to cover Visa Infinite, Amex, and rewards Mastercards while still leaving margin. On IC++, regulated debit cards (capped at $0.21 plus 0.05 percent under the Durbin Amendment) cost the merchant just over 0.20 percent all-in. The same debit card on Stripe still costs 2.9 percent plus $0.30.

A regulated debit swipe costs roughly 0.20 percent under IC++. On Stripe, it costs 2.9 percent. The 2.70 percent gap is the flat-rate tax.

Card mix matters more than headline rate. A pizza chain with 40 percent regulated debit, 30 percent basic credit, and 30 percent rewards credit saves dramatically more on IC++ than a luxury hotel with 80 percent premium rewards and Amex.

Where it goes wrong for operators

The headline "interchange plus 0.20 percent" makes IC++ sound simple. The actual statement rarely is. Five patterns where the effective cost diverges from the quote:

- Padded basis points hidden in the markup line. A processor quoting "interchange plus 15 basis points" can bill 25 to 35 basis points by adding "non-qualified" or "downgrade" surcharges to specific card types. If your statement shows a non-qualified bucket with mid-qualified or non-qualified rates, the processor is using tiered pricing dressed up as IC++.

- Marked-up assessments disguised as pass-through. Some processors charge 0.18 or 0.20 percent for the assessment line and call it pass-through. Visa credit assessments are fixed at 0.14 percent. Anything above that is hidden markup. The same applies to Mastercard at 0.1375 percent.

- Stacked monthly fees that swallow markup savings. A processor quoting "interchange plus 0.15 percent" can add $99 monthly platform fees, $25 monthly minimums, $15 statement fees, and a $295 annual PCI fee. At $50,000 monthly volume, that fixed-fee stack works out to about 28 basis points of extra cost.

- Per-transaction fees stacked under the per-transaction line. The quoted $0.10 per transaction sometimes breaks down as $0.05 authorization plus $0.02 capture plus $0.03 batch settlement. Same number on paper, different line items, different ways to add fees later.

- Cross-border and currency conversion surcharges. International cards trigger a 0.40 to 0.80 percent surcharge that some processors split between assessment and markup so it is harder to spot. E-commerce merchants with international traffic should require the cross-border line to be itemized separately.

A merchant at $200,000 monthly volume on a quoted "interchange plus 0.18 percent plus $0.08" can pay an effective rate of 2.65 percent when interchange runs about 1.85 percent, assessments hit 0.14 percent, and the markup line balloons to 0.66 percent after junk fees and stacked per-transaction charges. The same merchant on a clean IC++ contract pays 2.25 percent. That 0.40 percent gap is $800 a month, or $9,600 a year, on a contract the merchant thought was already competitive.

Most IC++ statements run 0.20 to 0.40 percent above the contracted markup once junk fees and stacked per-transaction charges hit the merchant's account.

Worked example with real numbers

Operator profile: a regional coffee roaster operating three retail locations and a small wholesale e-commerce channel. Monthly card volume sits at $185,000. Average ticket is $14. The owner currently runs all card processing through Square at 2.6 percent plus $0.10 in-person and 2.9 percent plus $0.30 online.

Current Square cost: $185,000 multiplied by 2.6 percent is $4,810. Add 13,214 transactions at $0.10, which is $1,321. Total monthly fees: $6,131. Effective rate: 3.31 percent.

Card mix from the Square breakdown: 35 percent Visa credit at blended interchange around 1.65 percent, 25 percent Mastercard credit at 1.60 percent, 30 percent regulated Visa debit at roughly $0.22 per transaction (per the Durbin Amendment cap), and 10 percent American Express at 2.30 percent.

Blended interchange across this card mix lands at roughly 1.45 percent. Add 0.13 percent blended assessments across all four networks. Add a competitive IC++ markup at $185,000 volume: 0.25 percent plus $0.08.

IC++ cost build-up: interchange of $2,683, assessments of $241, markup percentage of $463, and markup per-transaction of $1,057. Total monthly fees: $4,444. Effective rate: 2.40 percent.

Square is the right answer for a brand-new shop doing $15,000 a month. At $185,000, the flat-rate tax shows up as a $20,000 annual line item.

A note on the card-mix breakdown: regulated debit is the biggest swing factor. Under the Durbin Amendment regulations published by the Federal Reserve, debit cards issued by banks with $10 billion or more in assets carry capped interchange at $0.21 plus 0.05 percent of the transaction. A coffee shop running 30 percent regulated debit at a $14 average ticket pays roughly $0.22 in interchange per debit transaction. On Square, the same transaction costs $0.46.

Operator playbook

The five-day work plan to get from quoted rate to signed contract on a clean IC++ deal:

- Pull your last three months of merchant statements. Add the gross processing fees across all three months. Divide by gross card volume. That is your effective rate. Most flat-rate merchants land between 2.7 percent and 3.4 percent.

- Get a card-type breakdown from your current processor. Most will provide it if asked. The mix of regulated debit, basic credit, rewards credit, premium credit, and Amex determines how much IC++ will actually save you.

- Request three IC++ quotes from independent processors. Specify IC++ format with the assessment line shown as pass-through. Any processor in the industry can quote it. Ignore the marketing copy.

- Ask each quoting processor to reprice your last full month line by line. They should give you an itemized breakdown: interchange, assessments, markup percentage, markup per-transaction, and all monthly fees. If they refuse, drop them.

- Read the contract before signing. The four clauses that bite: automatic renewal (often three years), early termination fee ($295 to $495 is industry standard), equipment leases (a $99-a-month terminal lease can cost $7,000 over five years), and PCI compliance fees ($99 to $295 annually). Push back on each.

- Confirm the assessment line is passed through at 0.14 percent for Visa credit and 0.1375 percent for Mastercard credit, per the network's published rates. Anything above that is markup the processor is hiding.

- Negotiate a 24-month maximum contract with no early termination fee. Industry default is 36 months with an ETF. Tell every quoting processor you require month-to-month or 24-month terms. The competitive ones agree.

- Reconcile every statement for the first three months after signing. Junk fees, monthly platform fees, and "additional services" charges often appear in month two. Catch them early and the processor will usually refund by referencing the quoted contract. After month three, that window closes.