TL;DR

Multi-location reconciliation breaks when MID structure, batch close times, and chargeback assignment do not match the way you actually run the business. The common pattern: each store has its own MID, settlements lump into a single bank line, and no one owns the variance between gross sales and net deposit. Map every MID to its batch window and DDA line before you renegotiate anything. Most operators recover 0.15 to 0.40 percent of monthly volume once the map is clean.

What this actually is

Multi-location reconciliation is the daily process of matching card revenue captured at each physical location to the net deposits the processor sends to your bank account. Each location typically operates as a separate Merchant ID (MID) under a chain or corporate hierarchy. The processor bundles the day's authorizations into a settlement file, routes them to the card networks for interchange clearing, deducts interchange and processor fees, and ACHes the net amount to your designated DDA.

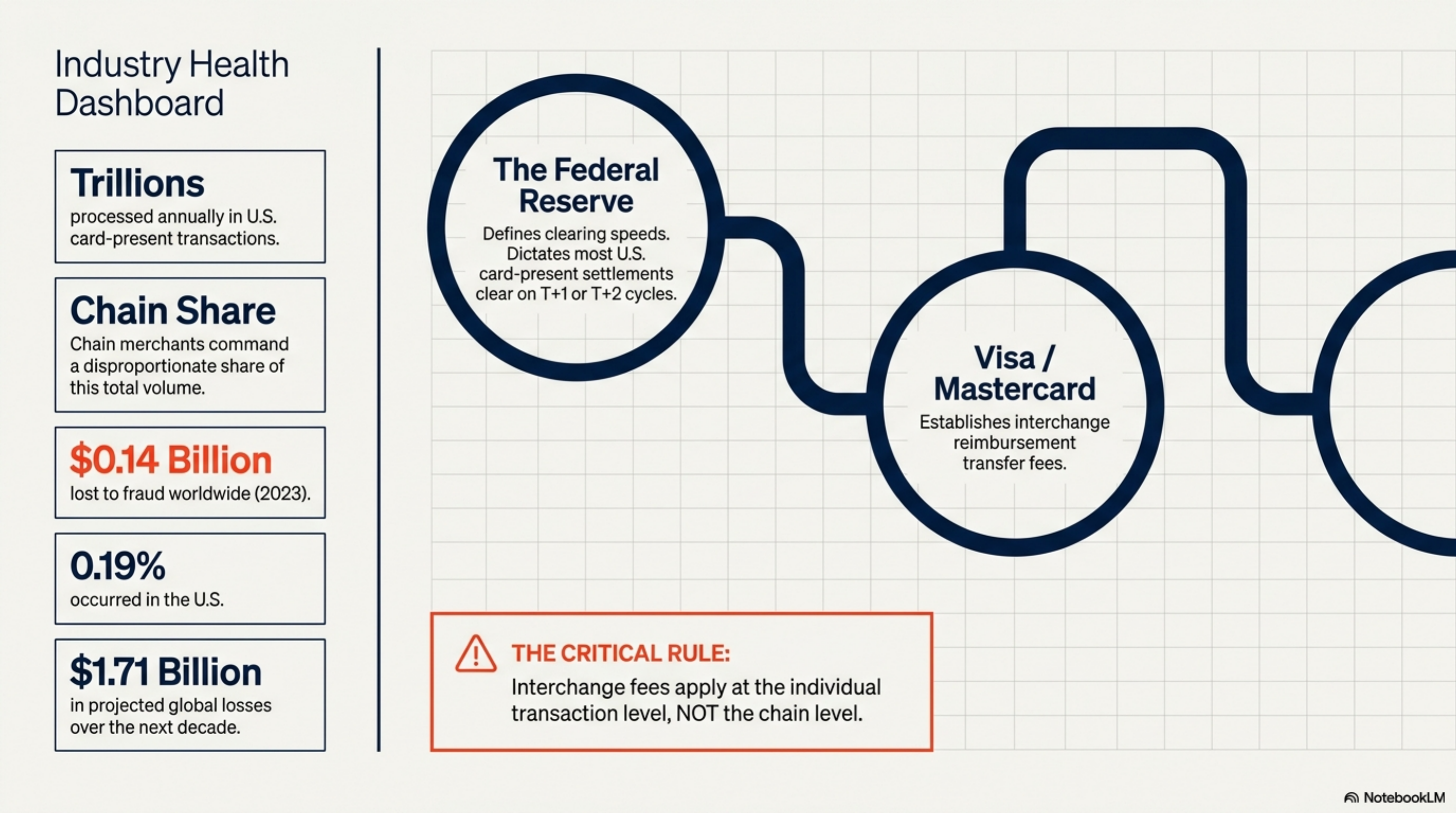

The Federal Reserve's payments research documents that most U.S. card-present settlements clear on a T+1 or T+2 cycle, depending on the acquirer and the merchant's risk profile. Interchange categories themselves are defined by the card networks: Visa publishes its full U.S. interchange reimbursement fee schedules and Mastercard does the same in its interchange rates and criteria. These tables drive the largest single cost line on any statement, and they apply at the transaction level, not the chain level. According to Nilson Report data, U.S. card-present volume runs in the trillions annually, and chain merchants account for a disproportionate share of card-present transactions.

The reconciliation problem grows with location count. Two stores share one POS report and one bank line: easy. Forty stores across three time zones, two POS systems, three MID groups, and a single bank account: that is where money disappears.

Multi-location reconciliation is the daily process of matching each store's card sales to the net deposits a processor sends to the merchant's bank account.

How it works under the hood

A card-present settlement from any of your locations follows the same path every night, but the pieces of that path are owned by different parties and timed differently:

- The terminal captures the authorization at the point of sale.

- The location runs a batch close at the time set on the terminal (often 11pm local, sometimes a global setting that ignores time zones).

- The processor pulls the batch file and queues it for clearing.

- The acquirer routes each transaction to Visa or Mastercard for interchange clearing.

- The network assesses interchange based on card brand, product, MCC, and data quality.

- The acquirer ACHes the net amount to the merchant's DDA on T+1 or T+2.

- Processor fees come out either daily (interchange-plus) or monthly (bill back or tiered).

- Chargebacks, retrieval requests, and adjustments arrive on their own clock, usually 30 to 120 days after the original transaction.

Several pieces of that flow vary by contract, and each one breaks reconciliation when it shifts:

Batch close timing. If the terminal's batch cutoff is set in UTC or the processor's headquarters time zone, a 10pm sale in California can fall into the next business day's batch. Your POS reports the sale on Tuesday; the bank gets it on Thursday.

Funding aggregation. Most acquirers offer two funding modes: gross funding (each MID deposits separately) and net funding (multiple MIDs deposit into a single line with one ACH per day). Net funding is the default for chains. It is also why a $9,400 deposit looks like the right number until you discover that store 7's $2,100 chargeback was deducted from corporate's MID inside that aggregate.

Fee assessment timing. Interchange-plus contracts typically deduct interchange at settlement, so the daily deposit is already net of interchange. Tiered and bill-back contracts deduct interchange daily but charge the markup at month-end, so daily deposits look clean and the monthly statement is the surprise.

If you cannot tell which MID a given ACH belongs to without opening three reports, your funding mode is wrong for your store count. Switch to gross funding before you negotiate rate.

Net funding hides per-store variance. One ACH lands in your bank; twenty-three MIDs settled inside it.

Where it goes wrong for operators

Five patterns recur across the chains we see:

1. Batch close mismatch. Stores in different time zones share a processor-side cutoff. A 10:15pm Pacific sale clears on the next business day. Weekly P&L looks right; the daily one is off by one location's evening rush every night. At a 12-store group running $150K monthly per location, this can swing reported revenue by $3,000 to $6,000 per day.

2. Single deposit, multiple MIDs. The acquirer ACHes one net amount per day. A bookkeeper matches it to one location and writes off the difference as fees. Over a year at $1.8M monthly volume, the unmatched ACH variance can hide $8,000 to $15,000 in misallocated fees nobody investigated.

3. Cross-MID chargeback assignment. A chargeback at store 7 gets deducted from the master MID's settlement. Store 7's P&L looks fine. Corporate's P&L looks like a margin problem. The team chases the wrong root cause for months.

4. Tip adjustments and offline transactions. Restaurants are the worst offenders. Tip adjustments hit after batch close, so the deposit number is always different from the POS gross. Offline transactions (store-and-forward) batch on the day they were captured, not the day they were transmitted, so they appear in the wrong daily report.

5. Daily discount vs. monthly bill back. On a bill-back plan, the daily deposit is gross sales minus interchange only. The markup, fees, and surcharges appear on the monthly statement. Operators who reconcile only to the daily deposit miss the second pass of fees until 30 days later. The gap is usually 0.40 to 0.85 percent of monthly volume.

Tiered and bill-back contracts are designed around month-end settlement of the markup. If your reconciliation is daily-only, you will miss the gap every single day until the statement arrives.

Worked example with real numbers

A 12-location quick-service restaurant group processes $1.8M in monthly card volume across three time zones. Average ticket: $14.20. Card mix: 72 percent credit, 28 percent debit, average debit transaction $11. Current pricing: tiered, effective rate 2.85 percent. The group reconciles weekly using a spreadsheet that matches the daily bank deposit to a POS export.

The math:

- Total monthly card fees: $51,300 (2.85 percent effective)

- Interchange-only baseline for this card mix: roughly 1.65 percent blended = $29,700

- Markup paid: $51,300 minus $29,700 = $21,600 per month, or 1.20 percent effective markup

When the operator pulled all 12 MID-level statements and matched them line by line:

- Three MIDs were running a downgraded interchange category 11 to 14 percent of the time because of a gateway routing issue that stripped AVS data on certain card-not-present rebills the group had recently added for catering.

- Cross-MID chargeback deductions had been hitting MID 01 (the flagship location) for eight months, masking roughly $1,400 per month in charges that belonged to MIDs 04, 07, and 11.

- Two MIDs had been billed a PCI non-compliance fee of $29.95 per month for 14 months, despite the chain passing its SAQ in month 2.

Recovery: roughly 0.35 percent of monthly volume on rerouted interchange, plus $420 per month in misallocated chargebacks moved to the correct stores (a margin reporting fix, not a fee fix), plus $838 in recoverable PCI fees.

At 0.35 percent of $1.8M, that is $6,300 per month in pure markup recovery. Annualized: $75,600. The PCI fees and chargeback reallocation are smaller dollars but unlock honest per-store P&Ls, which is what the operations team actually needed in order to compare stores to each other.

The lesson: the fee math is a side effect of the reconciliation map. You cannot negotiate what you cannot see at the MID level.

A 12-store QSR group at $1.8M monthly volume, 2.85 percent effective rate, found $6,300 per month in markup recovery and $838 in recoverable PCI fees after a one-week MID-level audit. The bookkeeper had been reconciling to a single daily ACH for three years.

Operator playbook

- Pull every MID's statement for the last three months. Not the chain-level summary; the individual MID PDFs. If your processor charges for this, that is the first fee to negotiate away.

- Build a one-row-per-MID map. Columns: legal entity, DBA, location address, batch close time (in local time AND UTC), DDA line, MCC code, pricing plan, contract end date, and 90-day average volume.

- Compare batch close timing to store operating hours. Any location whose batch cutoff falls during operating hours is generating reconciliation noise every day. Ask the processor to align cutoffs to local store time, ideally one to two hours after close.

- Switch from net funding to gross funding if you run more than six locations. Some acquirers charge $0 for this; some charge $5 to $15 per MID per month. The per-MID deposit clarity is worth the line item.

- Pull a 90-day chargeback report at the MID level. Match each case to the MID that processed the original transaction. Any case deducted from a different MID is a misallocation. Request reclassification in writing.

- Audit PCI non-compliance fees on every MID. If the SAQ was filed for the chain, fees on individual MIDs after the compliance date are usually recoverable. Average recovery for a 10-MID group runs $1,200 to $3,500.

- Ask for interchange-plus pricing at the chain level with a single chain-level monthly minimum, not per-MID minimums. Per-MID minimums on a slow store quietly cost $500 to $1,500 per year per slow location.

- Set a fixed monthly reconciliation cadence. Pull all MID statements on day 5 of the following month, match to gross funding deposits, file disputes by day 15. Operators who do this for a quarter find the patterns; operators who do it once find nothing.

PCI compliance fees on compliant MIDs run $25 to $35 per MID per month and persist for years before anyone catches them.