TL;DR

Most merchant processing contracts are three-year, auto-renewing agreements with early-termination fees of $295 to $595, monthly minimums, PCI charges, and a pricing tier the salesperson rarely defines in writing. Before you sign, get the pricing model named on paper (interchange-plus, tiered, or flat-rate), pin down the term and renewal language, demand a complete fee schedule, and surface any reserve or rolling chargeback hold. The twelve questions in this guide get those terms on paper before they get into your statements.

What this actually is

A merchant processing contract is the written agreement between a business and its acquiring bank or ISO that sets the pricing model, contract term, equipment obligations, settlement timing, and the conditions under which either party can exit. The Federal Reserve documents the structure of U.S. card payment flows and the role of acquirers in clearing and settlement. Card-brand interchange sits above this contract: the acquirer pays interchange to the issuing bank on every transaction, then passes that cost through to the merchant under whatever pricing model the contract specifies.

The contract is the only document that ties what the salesperson promised to what the processor has to deliver. A rate sheet shows a percentage. The contract defines whether that percentage is interchange-plus, tiered, or flat-rate, whether the markup is fixed or variable, how monthly fees are calculated, what happens at renewal, what the merchant pays if equipment breaks or the agreement is terminated early, and how chargebacks route.

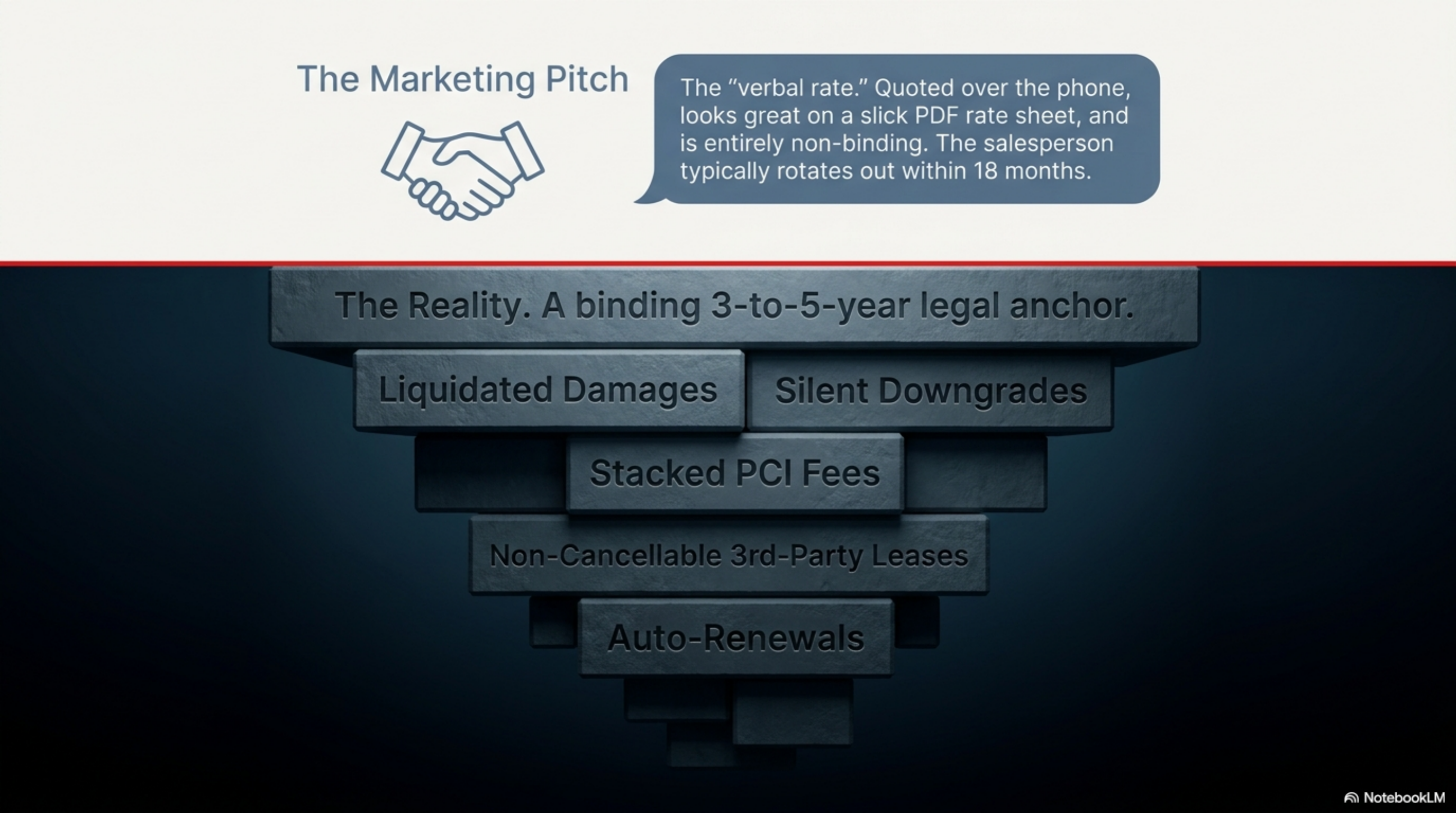

Most operators sign a contract built around a salesperson's verbal pitch. The salesperson rotates out within 18 months. The contract stays for three to five years.

A processor contract is the written agreement that sets pricing model, term length, fees, equipment terms, and termination conditions between a merchant and its acquirer or ISO.

How it works under the hood

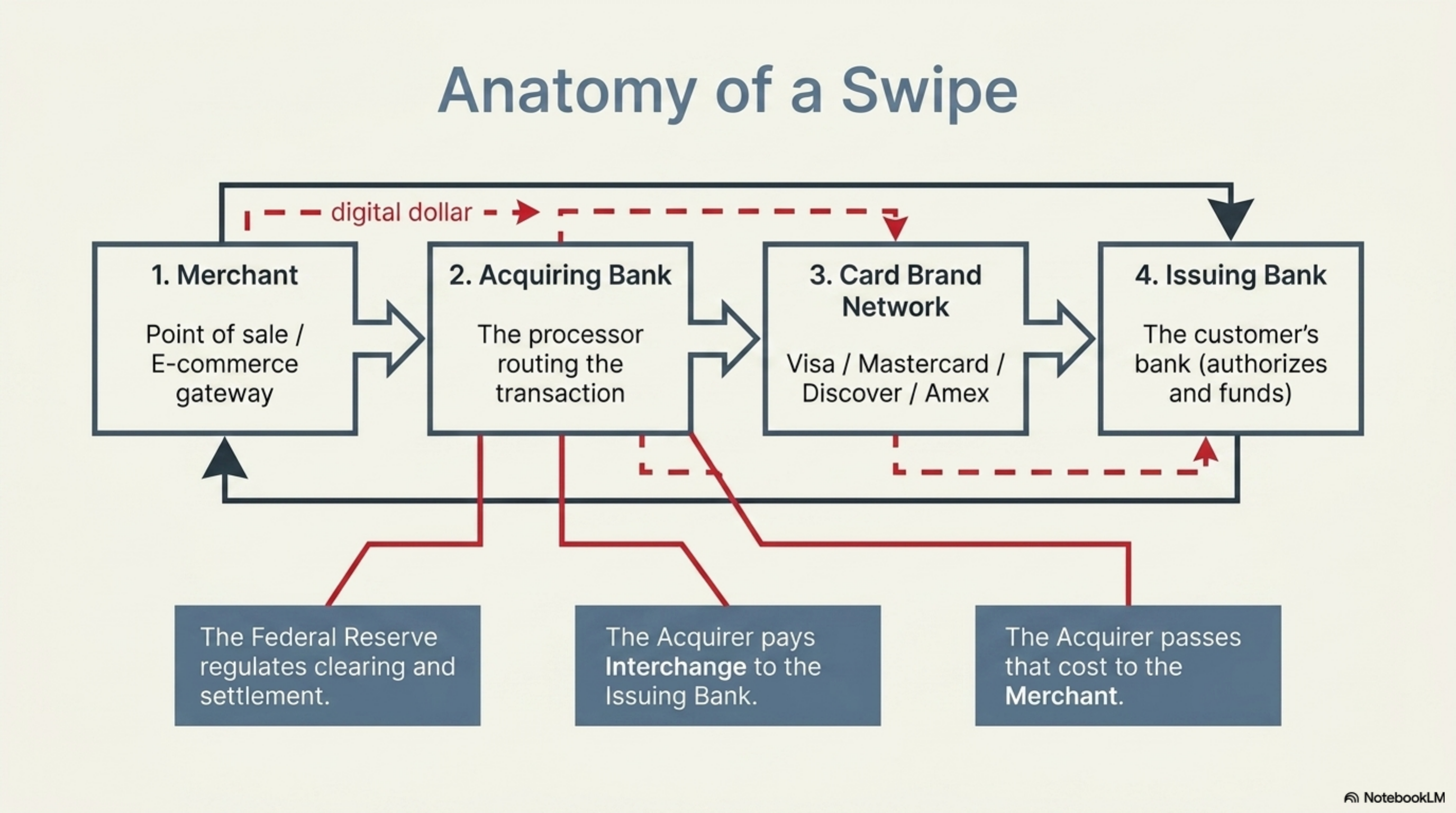

Once signed, a processor contract activates a chain of obligations across four parties on every card sale:

- The merchant submits a transaction through a point-of-sale terminal or gateway, which routes to the acquiring bank.

- The acquirer routes through the card brand network (Visa, Mastercard, Discover, American Express) to the issuing bank.

- The issuing bank authorizes or declines, then settles the transaction value to the acquirer net of interchange.

- The acquirer settles to the merchant's depository account, net of interchange, brand assessments, processor markup, and any contracted incidental fees.

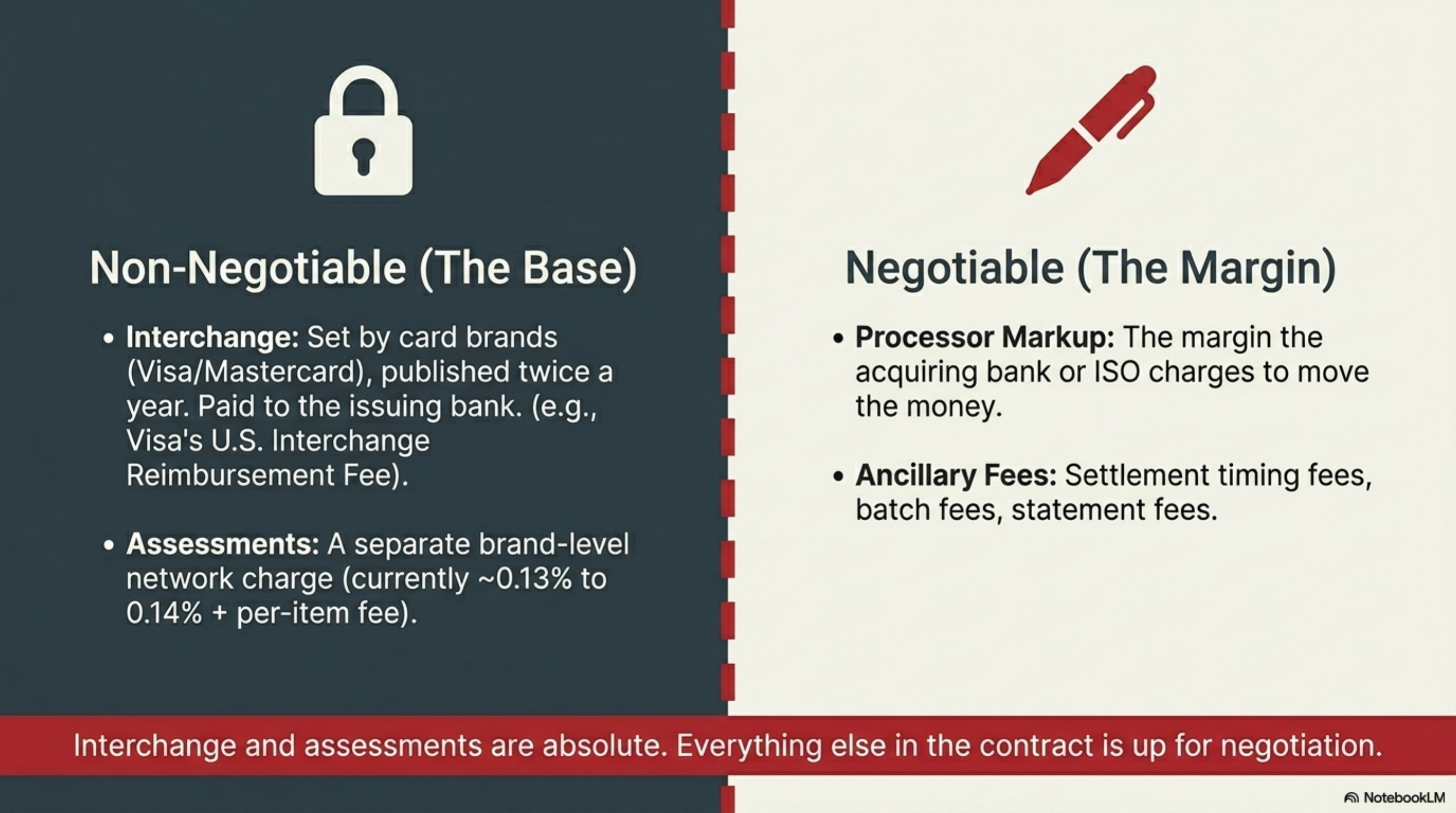

Interchange is set by the card brands and published twice a year. Visa publishes its U.S. Interchange Reimbursement Fee schedule on its small-business site. Mastercard publishes its U.S. Region Interchange Programs and Rates. Assessments are a separate brand-level charge, currently around 0.13 to 0.14 percent for Visa and Mastercard plus a per-item network fee. Neither interchange nor assessments are negotiable. The processor's markup is.

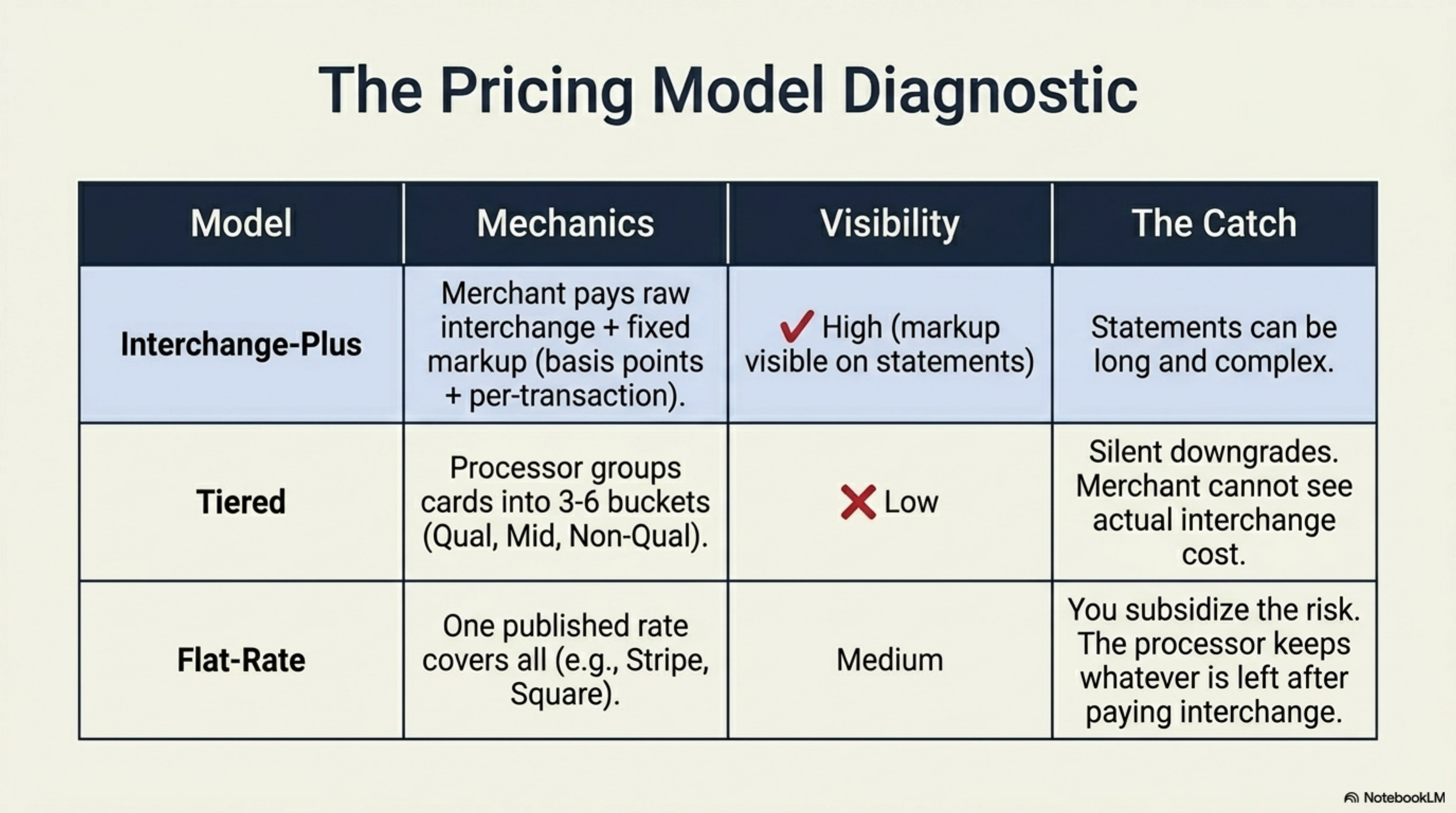

Three pricing models cover almost every U.S. contract:

- Interchange-plus (also called cost-plus or IC-plus): the merchant pays raw interchange plus a fixed markup, expressed as basis points plus a per-transaction fee. The markup line is visible on every monthly statement.

- Tiered (qualified, mid-qualified, non-qualified): the processor groups card types into 3 to 6 buckets and charges a single percentage per bucket. The merchant cannot see which interchange category each transaction landed in. Downgrades from qualified to non-qualified are routine and unaudited.

- Flat-rate (sometimes called blended or simplified): one published rate covers nearly all card types. The markup is whatever is left after the processor pays interchange. Stripe and Square use this model.

Settlement timing is also a contract term. Standard funding is T+1 or T+2 business days. Same-day or next-day funding is available, usually at 0.10 to 0.50 percent extra or a flat per-batch fee. Rolling reserves of 5 to 10 percent of monthly volume are common for high-risk merchant category codes and any account with elevated chargeback ratios.

Renewal language is the trap. Most agreements auto-renew for one or three-year terms unless the merchant submits written notice 60 to 90 days before the end of the current term. Miss the window, and the contract rolls forward at the same pricing with the same early-termination fee attached.

Interchange and assessments are not negotiable. The processor's markup is. Everything else in the contract follows from that one fact.

Where it goes wrong for operators

Five patterns surface in almost every problem contract we read at the $25K to $5M monthly volume range.

Pattern 1: liquidated damages disguised as an early-termination fee. The boilerplate language often calls the exit fee a flat $295 to $595. Read further and the same clause can include "liquidated damages" calculated as the average monthly processing fee times the months remaining in the term. A merchant processing $250,000 a month at a 0.50 percent effective markup leaves $1,250 a month on the table. Twenty-two months left on the contract means $27,500 in damages on top of the flat ETF.

Pattern 2: tiered pricing with silent downgrades. The contract names a qualified rate of 1.79 percent. The merchant runs $300,000 a month. After 90 days, statements show 60 percent of volume at 2.99 percent because the processor classified rewards cards, corporate cards, and any keyed transaction as non-qualified. The net effective rate runs 2.55 percent, not 1.79 percent. On $300K of monthly volume, that gap is $27,360 a year.

Pattern 3: PCI fees stacked across both compliance and non-compliance. The annual PCI compliance fee runs $99 to $199. The monthly PCI non-compliance fee runs $19.95 to $39.95 until the merchant completes a Self-Assessment Questionnaire. Many operators pay both for years because no one walks them through the SAQ.

Pattern 4: equipment leases routed through a third party. A $400 terminal leased at $79 a month for 48 months costs $3,792. The lease is non-cancellable even if the merchant terminates the processing contract. The lease company is often a separate entity (First Corporate Solutions, Northern Leasing, and similar names recur) outside the processor's own terms of service, so canceling processing does nothing to the lease.

Pattern 5: reserves with no release schedule. A 10 percent rolling reserve on $400,000 of monthly volume holds back $40,000 a month. If the contract says the reserve "may be released at the processor's discretion," the merchant has no recourse if the funds sit for 12 to 18 months after termination.

Worked example with real numbers

Operator profile: a direct-to-consumer skincare brand, $180,000 in monthly card volume, $68 average ticket, 2,647 transactions per month, currently on Stripe's flat-rate plan at 2.9 percent plus $0.30 for online card sales.

Current monthly cost on Stripe: $180,000 times 0.029 equals $5,220 in percentage fees. Plus 2,647 times $0.30 equals $794 in per-transaction fees. Total: $6,014 a month, an effective rate of 3.34 percent.

The merchant gets quoted by a regional ISO at "1.49 percent plus $0.15." The salesperson does not specify the pricing model in the pitch. The contract names a qualified rate of 1.49 percent, a mid-qualified surcharge of 0.85 percent, and a non-qualified surcharge of 1.40 percent. That is tiered pricing, not interchange-plus.

The merchant's card mix is roughly 25 percent qualified, 30 percent mid-qualified (rewards cards), 45 percent non-qualified (premium rewards, corporate, and keyed). Effective rate works out to 2.46 percent. Per-transaction cost on $180K with 2,647 transactions: $180,000 times 0.0246 equals $4,428, plus 2,647 times $0.15 equals $397. Total: $4,825 a month. Annual savings versus Stripe: $14,268.

Now price the same volume on a properly built interchange-plus contract at 0.20 percent plus $0.08. Average effective interchange for a CNP skincare card mix runs roughly 2.05 percent, drawing on Nilson Report compilations of Visa and Mastercard schedules. Effective rate: 2.05 plus 0.20 plus assessments (0.14 percent) equals 2.39 percent. Total monthly cost: $180,000 times 0.0239 equals $4,302, plus 2,647 times $0.08 equals $212. Total: $4,514 a month. Annual savings versus Stripe: $18,000. Annual savings versus the tiered ISO offer: $3,732.

Plug your own numbers in: monthly volume times effective interchange (use 2.05 percent for CNP skincare, 1.75 percent for restaurant card-present, 1.85 percent for retail card-present as starting points) plus the processor markup in basis points, then add the per-transaction fee times your monthly transaction count.

Operator playbook

Twelve questions to ask in writing before you initial a processor contract. Get answers attached to the agreement, not in email.

- What is the pricing model, in writing? The contract must name interchange-plus, tiered, or flat-rate. If the salesperson resists naming it, the model is tiered.

- What is the basis-point markup and the per-transaction fee? On interchange-plus, the markup should be expressed as a number such as 0.15 percent plus $0.07. Phrases like "competitive rates" do not bind.

- What is the contract term and the renewal clause? Get the term in months, the auto-renewal length, and the exact notice window (60 days, 90 days). Have the notice address listed in the contract, not on a separate web page.

- What is the early-termination fee, and does it include liquidated damages? If the clause references "lost profits," "average monthly fees," or "remaining term," that is liquidated damages. Strike the clause or cap it at a flat dollar figure.

- List every monthly fee, including PCI, statement, gateway, batch, and minimum. Ask for a sample statement at your projected volume. PCI annual plus PCI non-compliance plus IRS 1099-K reporting fees commonly run $300 to $600 per year.

- Is there an equipment lease, and through whom? Reject any third-party lease longer than 12 months. Buy terminals outright for $150 to $400 or use a free placement program tied to the processing contract only.

- What is the reserve policy, and what is the release schedule? If reserves apply, the release schedule must be in writing with a defined trigger (12 months of clean processing, chargeback ratio below 0.5 percent).

- How are chargebacks priced and disputed? Standard chargeback fee is $15 to $25. Anything higher, or any "non-refundable" language, gets struck.

Most operators on tiered pricing run 60 to 75 basis points above what their card mix actually costs on interchange-plus. The gap is visible on the statement, never in the contract.