TL;DR

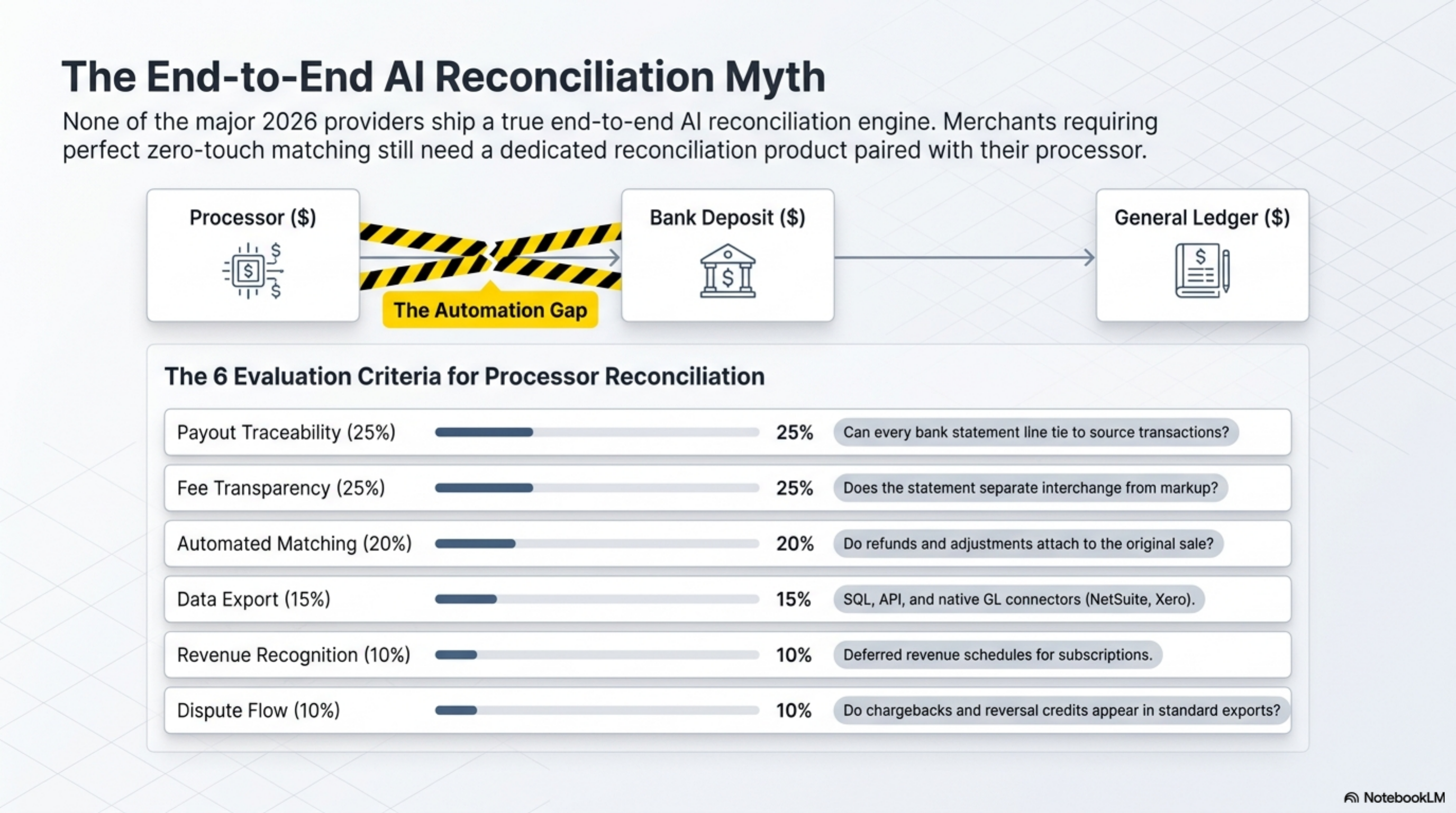

For online and subscription businesses over $100K monthly, Stripe ships the most automation between sales, fees, refunds, and bank deposits. Sigma SQL queries and the Revenue Recognition module remove most manual matching. Helcim is the runner-up for sub-$500K interchange-plus merchants who want statements that tie to the penny. Square wins one segment only: single-location retail and food service that runs everything through one POS. None of the providers compared here ship a true end-to-end AI reconciliation engine.

How we ranked

Reconciliation is the process of matching every transaction across the processor, the bank deposit, and the general ledger. We weighted six criteria:

- Payout traceability (25%): can every line on the bank statement be tied to source transactions?

- Fee transparency (25%): does the statement separate interchange, assessments, scheme fees, and processor markup?

- Automated matching (20%): do refunds, disputes, and adjustments attach automatically to the original sale?

- Data export (15%): SQL, API, CSV, and native connectors to QuickBooks, Xero, NetSuite, Sage Intacct.

- Revenue recognition (10%): deferred revenue schedules for subscriptions and prepayments.

- Dispute flow (10%): do chargeback reason codes, reversal credits, and representment outcomes appear in the same export as charges?

Pricing was pulled from each provider's public pricing page. Markup math was verified against the Visa interchange schedule and Mastercard interchange rates. Volume bands reference U.S. card processing patterns published in the Federal Reserve payments studies.

At a glance

Six providers, headline pricing per their public pricing pages, contract posture, and where each one fits in a reconciliation stack:

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online; 2.7% + $0.05 in person | Month-to-month | 2 business days | SaaS, marketplaces, online | Sigma usage costs scale with query volume |

| Square | 2.6% + $0.10 in person; 2.9% + $0.30 online | Month-to-month | Next day | Single-location retail and food | Weak on B2B card-not-present |

| Helcim | IC + 0.40% + $0.08 in person; IC + 0.50% + $0.25 online | Month-to-month | 2 business days | Mid-market $50K to $750K monthly | No built-in revenue recognition |

| Stax | $99/mo + IC + $0.08 in person | Month-to-month | 2 business days | $50K+ monthly subscription pricing | Platform fee only pays off above ~$30K monthly |

| Clover | $14.95 to $54.95/mo + 2.3 to 2.6% + $0.10 | Hardware lease often 36 to 48 months | Next day | In-store SMB with POS hardware | Hardware lock-in via reseller contract |

| PayPal | 3.49% + $0.49 standard; 2.59% + $0.49 advanced card | Month-to-month | Next day | Consumer checkout add-on | No interchange transparency |

Stripe

Stripe's reconciliation stack is the most complete on this list. Every charge, refund, dispute, and adjustment flows into a single object model exposed through the Balance Transactions API and the Sigma SQL warehouse. Sigma costs $0.02 per query against your own transaction data, which is workable until you hit a few thousand scheduled queries per month. Revenue Recognition adds deferred revenue, amortization, and contract change tracking for $99 per month on ARR under $1 million, then scales by volume per stripe.com/pricing.

On the processing side: 2.9 percent plus $0.30 online, 2.7 percent plus $0.05 in person, with custom interchange-plus available for volumes over roughly $80,000 monthly. There is no monthly platform fee on the standard plan.

Native integrations cover QuickBooks Online, Xero, NetSuite, and Sage Intacct. The Stripe Tax product handles sales tax against the same ledger so tax accruals do not drift from gross sales.

Best for: SaaS, marketplaces, and any business where the finance team writes SQL or works with an accountant who does. Avoid if you have a single in-store till; you are paying for capability you will not use.

Square

Square's reconciliation is straightforward because the product is vertically integrated. Sales, refunds, tips, taxes, and fees all post to the same Dashboard ledger. The standard payout reports tie each daily deposit to the underlying batch. Pricing per squareup.com/us/en/pricing: 2.6 percent plus $0.10 in person, 2.9 percent plus $0.30 online, 3.5 percent plus $0.15 keyed.

Where Square wins: a single-location retailer or restaurant where the POS is the system of record. The accounting flow to QuickBooks Online is one click and the daily payout matches a single bank deposit.

Where it falls short: B2B card-not-present, level 2 and level 3 data, multi-entity reporting, deferred revenue, and any scenario where the merchant runs more than one platform. Square does not pass interchange through transparently; on volume above $250K monthly the flat-rate markup typically sits 0.50 to 0.80 percent above an interchange-plus contract on the same card mix per the Visa interchange schedule.

Best for: single-location merchants under $250K monthly. Reconsider above $500K monthly volume.

Helcim

Helcim publishes interchange-plus pricing on a public rate card and applies automatic volume discounts as merchant volume grows. The published rates: interchange plus 0.40 percent and $0.08 in person, interchange plus 0.50 percent and $0.25 online per helcim.com/pricing. There is no monthly platform fee.

The merchant statement breaks out interchange, assessments, and the Helcim markup as separate line items. That is the structural baseline for accurate reconciliation: every cent on the bank deposit ties back to a category on the statement. The Helcim API exposes the same data programmatically, and native QuickBooks Online and Xero connectors cover the standard SMB workflow.

Helcim does not ship a Revenue Recognition module; subscription merchants doing deferred revenue work keep that logic in their billing system.

Best for: mid-market merchants between $50K and $750K monthly volume who want the cleanest possible statement. Avoid if you need built-in revenue recognition or a dedicated implementation team for a multi-entity rollout.

Stax

Stax (formerly Fattmerchant) charges $99 per month plus interchange pass-through plus $0.08 per in-person transaction or $0.18 per online transaction per staxpayments.com/pricing. The subscription model means the processor markup does not scale with volume; the per-transaction surcharge is fixed. That makes reconciliation arithmetic simple: bank deposit equals gross sales minus interchange minus the per-transaction surcharge.

The OmniCommerce dashboard consolidates in-person, online, and invoicing into one view. Reporting exports include interchange and assessment fees broken out per transaction. Native QuickBooks Online and accounting connectors are included in the platform fee.

Where the math works: $50K to $500K monthly volume. Below $30K monthly, the $99 platform fee adds 0.20 percent or more to the effective rate and erases the interchange-plus advantage. Above $500K monthly, an interchange-plus contract from a direct ISO will usually undercut Stax on the per-transaction surcharge.

Best for: subscription, professional services, and B2B merchants in the $50K to $500K monthly range that want predictable platform costs. Avoid if you process under $25K monthly.

Clover

Clover is sold by hundreds of resellers including Fiserv, banks, and ISOs. The published plan pricing on clover.com/pos-systems ranges $14.95 to $54.95 per month plus 2.3 to 2.6 percent and $0.10 in person and 3.5 percent plus $0.10 keyed. The actual processing contract sits behind the reseller, and the rates the merchant signs vary widely between resellers.

Reconciliation at the POS layer is fine: daily deposits, sales by item, employee, and location. The weakness is on the contract side. Clover hardware is often financed or leased on a 36 to 48 month term, and ending the processing relationship early triggers an early termination fee plus orphaned hardware.

For pure POS reconciliation, Clover ships the standard reports. It does not match invoices to ACH credits and does not handle deferred revenue. Best for: in-store SMB comfortable with the App Market and hardware lock-in.

PayPal

PayPal's reconciliation tooling is built around its own ledger. Every transaction posts to the PayPal balance, then transfers to the linked bank on the merchant's schedule. The reports separate gross, fees, taxes, refunds, and disputes per transaction. Pricing per paypal.com/us/business/paypal-business-fees: 3.49 percent plus $0.49 standard card payments, 2.59 percent plus $0.49 advanced card, 2.29 percent plus $0.09 in person.

The headline rate makes PayPal one of the most expensive options for B2B average tickets above $100. On a $250 invoice, the standard 3.49 percent plus $0.49 fee comes to $9.21, or 3.68 percent effective.

Native QuickBooks Online sync is available. PayPal does not pass interchange through transparently and does not break out interchange, assessment, and markup on the merchant statement. That makes line-by-line fee verification impossible.

Best for: consumer checkout add-on alongside a primary card processor. Avoid as the primary processor for B2B or high average ticket card-not-present.

Verdict

For SaaS and online merchants over $100K monthly: Stripe. The Balance Transactions API and Sigma SQL make every fee, refund, and dispute queryable in a single object model, and Revenue Recognition handles deferred revenue at $99 per month under $1M ARR per stripe.com/pricing.

For mid-market merchants between $50K and $750K monthly who want a published interchange-plus statement: Helcim. The statement breaks out interchange, assessments, and markup as separate lines per helcim.com/pricing and there is no platform fee.

For single-location retail and food service running everything through one POS: Square. Daily deposits match a single batch and the QuickBooks Online sync is a single click. Above $250K monthly, the flat-rate markup costs more than it saves in tooling.

None of these are end-to-end AI reconciliation tools. They are payment processors with reconciliation features built in. Merchants who need true AI matching pair one of them with a dedicated reconciliation product.