TL;DR

For most U.S. ecommerce operators in the $25K to $750K monthly card-not-present range, Helcim wins on effective rate because interchange-plus pricing removes the 0.40 to 0.55 percent flat-rate margin that Stripe and PayPal keep when interchange drops. Stripe wins under $25K monthly and for global or developer-heavy stacks. Stax wins above roughly $80K monthly with predictable transaction count. PayPal stays a checkout-button add-on, not a primary processor. Square fits small omnichannel sellers. Worldpay earns its custom contract above $1M monthly and rarely below.

How we ranked

Five weighted criteria. First, effective rate at $250K monthly card-not-present volume modeled on a typical U.S. mix of regulated debit, rewards credit, and corporate cards. Second, contract length and early termination fee, since 36-month deals with $295 ETFs trap merchants when better pricing arrives. Third, settlement speed, with same-day or next-day standard and any held-funds reserve flagged. Fourth, Level 2 and Level 3 data support, which can cut interchange on commercial cards by 0.50 to 1.00 percent based on the qualifying rate sets published in the Visa interchange schedule and the Mastercard interchange tables. Fifth, hardware and platform lock-in, including proprietary gateways that block portability. We pulled headline pricing from each processor's public page as of May 2026 and cross-checked against published interchange categories. Volume tier guidance reflects long-run patterns reported by the Federal Reserve payments studies.

At a glance

Headline rates are from the processor's public pricing page as of May 2026. Effective rates at $250K monthly will differ based on your card mix.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online | None | 2 days | Under $25K, marketplaces, SaaS | 0.40 to 0.55% markup above IC+ |

| Helcim | IC + 0.50% + $0.25 | None | 2 days | $25K to $750K ecommerce | Business-hours support only |

| Stax | $99/mo + IC + $0.18 | Month-to-month processing | 2 days | $80K to $500K, predictable count | $99 fixed cost at low volume |

| PayPal | 3.49% + $0.49 standard | None | 1 day | Wallet button add-on | 21-day reserve on new accounts |

| Square | 2.9% + $0.30 online | None | 1 day | Small omnichannel sellers | Held-funds reserve risk |

| Payment Depot | $79 to $199/mo + IC | Month-to-month | 2 days | $50K to $250K membership pricing | Hardware and gateway billed separately |

| Worldpay | Custom IC+ (contact sales) | 36 months typical | 1 day | $1M+ monthly, B2B mix | ETF tied to projected revenue |

Stripe

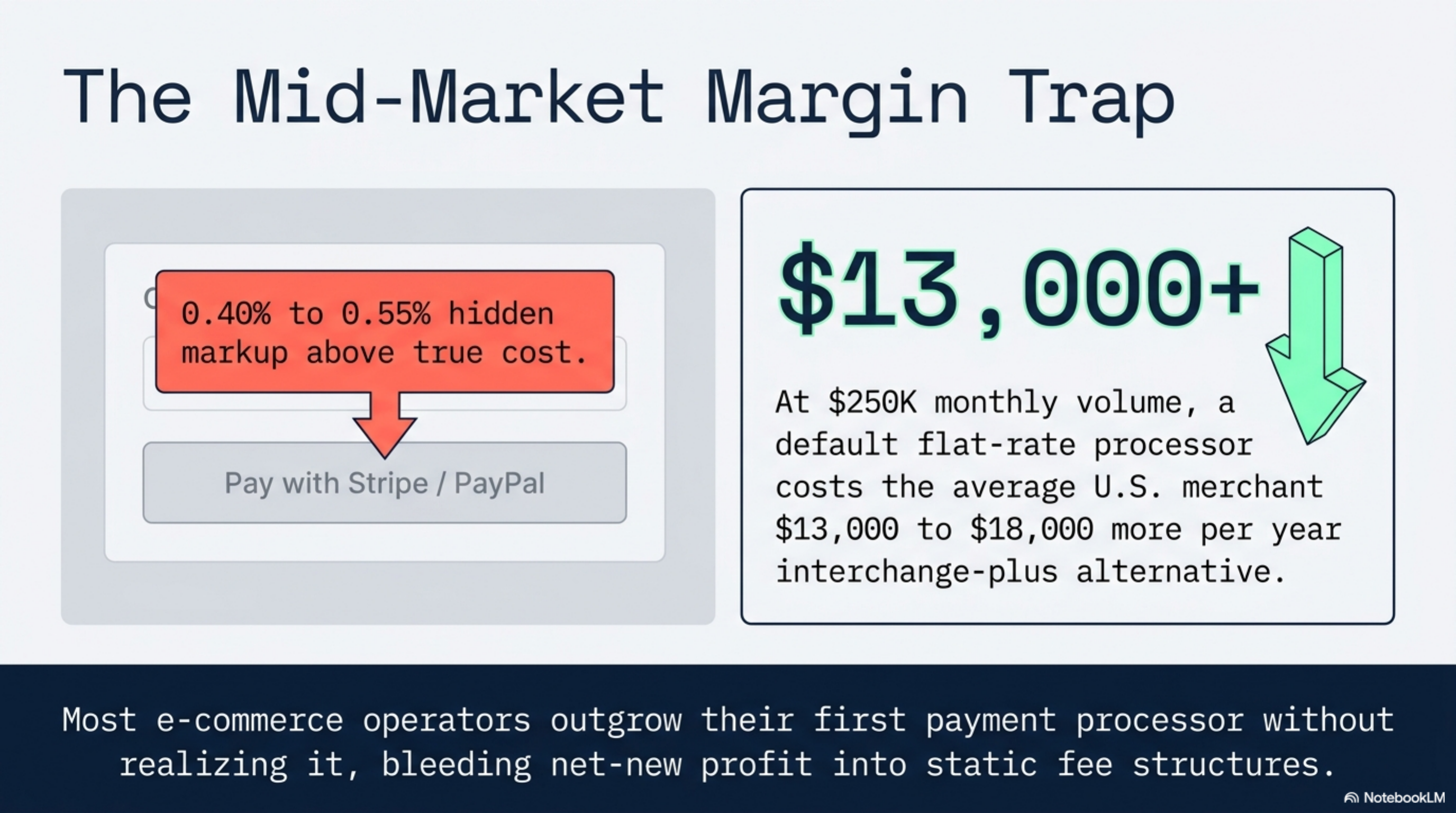

Stripe charges 2.9 percent plus $0.30 on its standard online rate, per its published pricing. At $250K monthly card-not-present volume with a typical U.S. card mix, that effective rate lands roughly 0.40 to 0.55 percent above interchange-plus, which works out to $12,000 to $16,500 per year in markup over a true cost-plus processor. There is no monthly fee, no contract, and accounts approve same day. The Stripe Connect, Billing, and Issuing stack is the strongest in this set for marketplaces, SaaS, and embedded payment platforms. Cross-border presentment in 135 currencies is real and works without third-party plugins. The trade-off shows up on rate. Stripe will not negotiate flat pricing under $80K monthly. Above that volume, ask for Interchange Plus on a custom plan; the public page is not the only menu. Best for: merchants under $25K monthly, marketplaces, SaaS billing, international stacks. Watch out for: a 1.5 percent currency conversion fee, an extra 0.5 percent on manually keyed transactions, and a $15 chargeback fee.

Helcim

Helcim publishes a single card-not-present rate of interchange plus 0.50 percent plus $0.25 per transaction, with automatic volume discounts that step the percentage down as monthly volume grows. See the Helcim pricing page. No monthly fee, no contract, no ETF. On a $250K monthly card-not-present book with the same typical card mix, the effective rate often runs 2.30 to 2.45 percent depending on rewards-card density and AVS qualification. That is roughly 0.45 to 0.60 percent below Stripe at the same volume, or $13,500 to $18,000 per year saved. Helcim processes for U.S. merchants and supports ACH, recurring billing, hosted checkout, and a developer API. The merchant dashboard surfaces interchange-line detail by transaction, which is the disclosure flat-rate processors do not give. Best for: U.S. ecommerce $25K to $750K monthly that wants real interchange-plus without sales calls. Watch out for: support is business hours only with no 24/7 phone line, and the dashboard requires a touch more accounting familiarity than a Stripe report.

A merchant doing $250K monthly on Stripe pays roughly 2.78 percent effective after the $0.30 fixed fees. The same volume on Helcim's interchange-plus tier typically lands near 2.35 percent. The annual gap is $12,900, before any volume discount kicks in.

Stax

Stax charges $99 per month and passes interchange straight through with $0.18 per card-not-present transaction, per its public pricing. The subscription model becomes attractive once monthly volume passes roughly $80K, because the $99 fixed cost spreads thin and the percentage markup goes to zero. At $250K monthly with 8,000 card-not-present transactions, you pay $99 plus $1,440 in per-transaction fees, plus raw interchange. That works out to roughly 2.10 to 2.25 percent effective, below Helcim at the same volume by 10 to 20 basis points. Stax includes a virtual terminal, hosted invoicing, and a payments API. Best for: ecommerce $80K to $500K monthly with predictable transaction count and average ticket above $40. Watch out for: the $99 fee is real overhead at low volumes, and the published plan often comes with a 36-month service agreement on financed hardware even though the processing side is month-to-month. Read the hardware addendum line by line before signing.

PayPal

PayPal's standard online rate is 3.49 percent plus $0.49 for PayPal-branded checkout, and 2.59 percent plus $0.49 for Advanced Card processing on the same account, per its business fee page. At $250K monthly, the standard rate is the most expensive in this comparison by 0.50 to 0.90 percent versus flat-rate alternatives, and roughly 1.10 to 1.40 percent versus interchange-plus. The reason most ecommerce sites still install PayPal is the consumer-side trust signal at checkout. PayPal Wallet adoption captures a meaningful share of buyers who would otherwise abandon, particularly on first-time purchases above $100. Treat PayPal as a wallet button on top of a primary processor, not as the primary processor itself. The 21-day held-funds reserve still applies to new high-risk accounts at PayPal's discretion. Best for: a secondary checkout button alongside Helcim, Stripe, or Stax. Watch out for: dispute outcomes that favor the buyer at rates above card-network averages, as documented in Federal Reserve consumer payments research.

Running PayPal Standard as your primary card-not-present rail on a $250K monthly book costs roughly $25,000 to $30,000 per year more than interchange-plus with the same card mix. Use PayPal as a wallet, not a processor.

Square

Square's online rate is 2.9 percent plus $0.30, identical headline pricing to Stripe, per its published rates. In-person is 2.6 percent plus $0.10, and keyed runs 3.5 percent plus $0.15 for the manually entered card path. Square's edge is the free POS and the omnichannel inventory sync between online and storefront, not the price. For an ecommerce-only merchant, there is no rate advantage versus Stripe and you lose Stripe's developer tooling. For an omnichannel seller with a single physical location and a $20K to $60K monthly online book, Square consolidates hardware, online checkout, payroll, and gift cards under one account, which has real ops value. Best for: small omnichannel sellers up to $60K monthly online volume with a retail front. Watch out for: instant deposit costs 1.75 percent per transfer, and the held-funds reserve practice is well documented in consumer dispute filings collected by federal regulators.

Payment Depot

Payment Depot sells wholesale interchange-plus on a monthly membership ranging from $79 to $199, plus interchange and $0.05 to $0.15 per transaction depending on tier, per its membership pricing page. Now operated under the Stax Payments umbrella, the brand still sells separately and the membership pricing competes directly with Stax above $50K monthly. The transaction cap on the lowest tier is typically $25K monthly, and you size up the membership as volume grows. Effective rates at $250K monthly land in roughly the 2.15 to 2.30 percent range, comparable to Stax with slightly different break-points by average ticket. Best for: merchants who prefer flat membership pricing and want a smaller U.S.-based support footprint. Watch out for: hardware financing and gateway fees are billed separately from the membership. The membership covers the processing markup, not every line item on the statement, so request the full schedule in writing before signing.

Worldpay

Worldpay (a FIS company) sells custom interchange-plus contracts and does not publish a flat retail rate on its corporate site. For ecommerce merchants under $1M monthly, the sales cycle runs 7 to 14 days and the contract is typically 36 months with an early termination fee tied to projected lost revenue. Worldpay's value shows up at enterprise volume where Level 3 data support, dynamic descriptors, multi-currency settlement, and BIN-level routing strategies cut interchange by 30 to 80 basis points on commercial card spend. According to the Nilson Report ranking of U.S. merchant acquirers, Worldpay processes more U.S. card volume than any acquirer except Chase, and that scale buys interchange concessions on the back end. Best for: ecommerce above $1M monthly with international or B2B card-not-present mix. Watch out for: below that volume threshold, the contract terms and ETF rarely justify the modest rate savings over a published interchange-plus offering.

Verdict

For most U.S. ecommerce operators in the $25K to $750K monthly range, Helcim wins on effective rate, contract terms, and statement transparency. The interchange-plus structure means your rate moves with the network's published wholesale rates, not with a flat margin that the processor keeps when interchange falls. Stripe wins under $25K monthly, when global coverage matters, or when the engineering team needs the Stripe API surface. Stax wins above roughly $80K monthly with predictable transaction count, where the $99 subscription amortizes below Helcim's percentage. PayPal stays a wallet button; do not let it run as your primary card-not-present processor. Worldpay earns its custom contract above $1M monthly and rarely below. Square fits small omnichannel sellers under $60K monthly online. The annual savings between flat-rate and interchange-plus at $250K monthly typically clear $13,000 per year, so a rate audit usually pays for itself in month one.

Before switching, pull your last three monthly statements, calculate effective rate (total fees divided by total volume), and request a written rate sheet from any new processor that itemizes interchange pass-through, processor markup, per-transaction fee, monthly fee, gateway fee, and PCI fee separately.