TL;DR

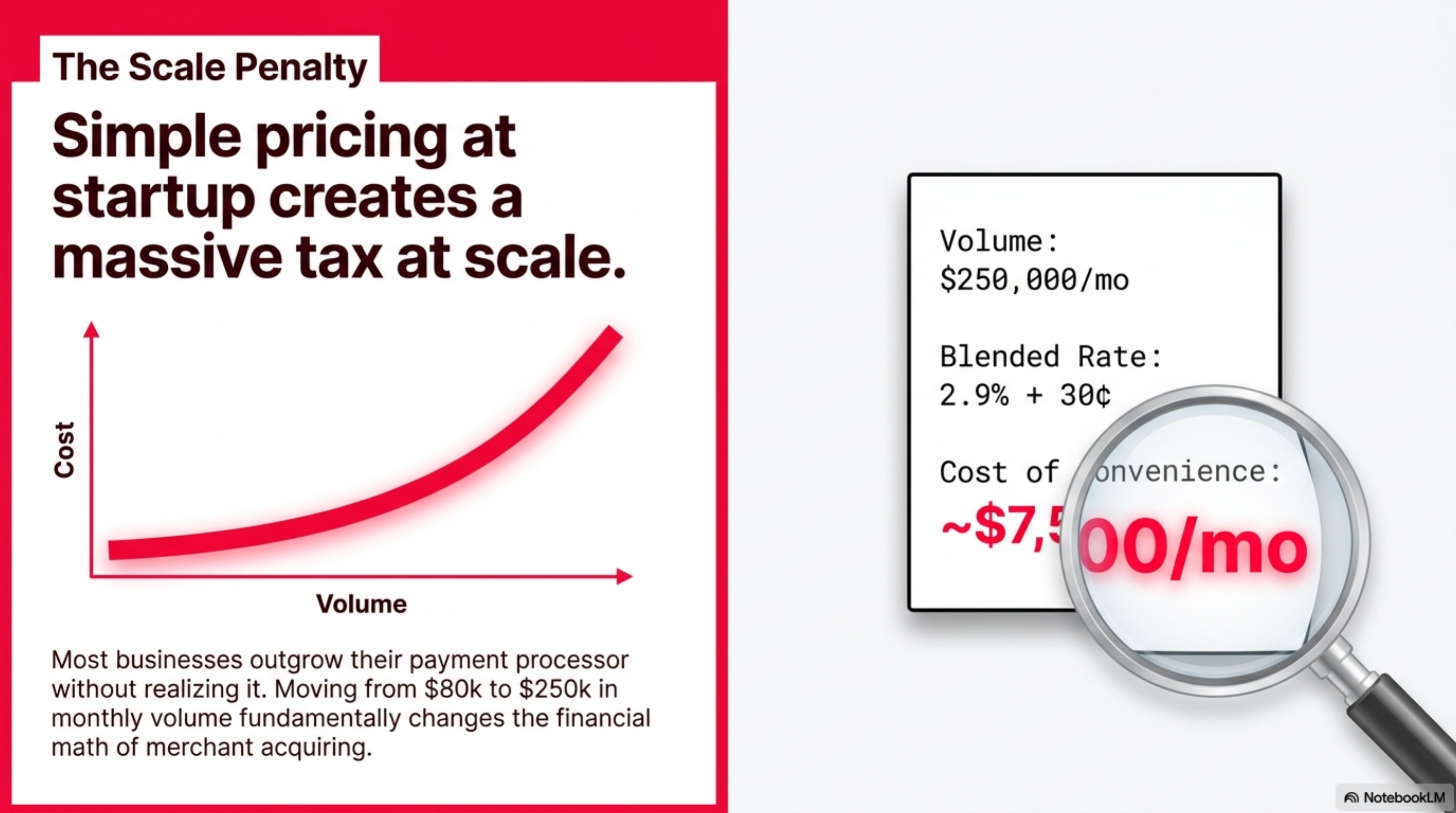

Stripe lists 2.9 percent plus 30 cents online with no monthly fee, same-day setup, and a published rate card (stripe.com/pricing). Worldpay quotes interchange-plus only, with a multi-week onboarding and a named account manager (worldpay.com). For merchants under roughly $80,000 in monthly card volume, Stripe costs less and ships faster. Above $250,000 monthly with a stable card mix, a Worldpay interchange-plus contract typically beats Stripe's effective rate by 0.40 to 0.70 percent, before hardware and PCI fees.

How we ranked

This comparison weights criteria that move real money on a merchant's monthly statement, not feature checklists.

- Effective rate at $250K monthly volume (40%): total processing cost divided by total volume, calculated on a mix of 65 percent consumer credit, 20 percent debit, 15 percent business or rewards.

- Contract length and ETF (15%): month-to-month with no early termination beats a three-year deal with a $495 ETF.

- Settlement speed (10%): T+2 is the U.S. baseline per Federal Reserve payments data; same-day or next-day funding earns a bump.

- Level 2 and Level 3 data support (15%): B2B merchants on purchasing cards see 0.50 to 1.00 percent in interchange savings when the processor submits full Level 3 data per Visa interchange criteria.

- Hardware and platform lock-in (10%): proprietary terminals or gateway fees that strand the merchant on switch lose points.

- Dispute and chargeback SLA (10%): response window, evidence portal, representment workflow.

At a glance

Pricing pulled from each provider's public rate card, or where no public rate exists, the published structure. Effective rate assumes a $250,000 monthly mix of 65 percent consumer credit, 20 percent debit, 15 percent business cards.

| Provider | Headline pricing | Contract | Settlement | Best for | Watch out for |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 online, 2.7% + $0.05 in-person | Month-to-month | T+2 | SaaS, marketplaces, under $80K/mo | No volume discount on published rate |

| Worldpay | Interchange-plus (custom) | 1 to 3 years typical | T+1 to T+2 | $250K+ monthly, B2B, enterprise | ETFs, PCI fee, monthly minimum |

| Helcim | IC + 0.40% + $0.08 in-person, IC + 0.50% + $0.25 online | Month-to-month | T+2 | $25K to $200K/mo SMB | No 24/7 phone support |

| Stax | $99/mo + IC + $0.08 in-person, $0.18 online | Month-to-month | T+2 | $50K to $500K/mo | Subscription only pays off above ~$25K/mo |

Stripe

Stripe publishes its rate card: 2.9 percent plus 30 cents on online card transactions, 2.7 percent plus 5 cents in-person, and 3.4 percent plus 30 cents on manually keyed cards (stripe.com/pricing). There is no monthly platform fee on the Integrated plan, no setup fee, and no PCI compliance charge. U.S. settlement runs on T+2 by default.

The pricing structure is a flat blended rate. Stripe absorbs interchange variability on its side. That makes a low-volume founder's life simple, and it makes a high-volume merchant subsidize the rewards cards in their card mix. A merchant running $250,000 in monthly online card volume on a typical B2C mix pays roughly 3.0 to 3.1 percent effective rate including the per-transaction component. The same merchant on a clean interchange-plus deal at IC + 0.20 percent would pay closer to 2.30 to 2.50 percent.

Stripe also charges 0.5 percent on stored card data, 1 percent on cross-border currency conversion, 0.4 percent on instant payouts, and platform-specific fees on Connect. None of these appear on the headline 2.9 percent line. A SaaS firm running $250K monthly with 30 percent international card volume pays roughly 3.2 to 3.3 percent all-in.

Custom interchange-plus pricing is available on direct request, generally above approximately $80,000 in monthly card volume. Stripe does not publish those rates.

Who it fits: SaaS subscriptions, digital goods, marketplaces, anything that needs a developer-first API. Best for merchants under $80,000 monthly until custom pricing becomes worth the conversation.

Who should avoid it: B2B sellers running corporate card volume, merchants with ticket sizes above $500, and anyone above $80K monthly who has not yet asked for a custom rate.

Worldpay

Worldpay does not publish a public rate card. Pricing is interchange-plus, quoted per merchant after underwriting, with onboarding typically taking 7 to 14 days (worldpay.com). Following the 2025 Global Payments acquisition, Worldpay sits inside the largest U.S. acquirer-processor stack alongside TSYS and Heartland.

Real-world IC+ quotes for mid-market merchants land in the 0.20 to 0.45 percent over interchange range, with per-transaction fees of 5 to 10 cents. A $250,000-per-month merchant with a typical card mix pays an effective rate of roughly 2.30 to 2.60 percent on Worldpay versus 3.0 to 3.1 percent on Stripe flat-rate. The delta is 0.40 to 0.70 percent, or $1,000 to $1,750 per month in savings before fixed fees.

For B2B merchants accepting purchasing cards, Worldpay's full Level 3 data submission can pull commercial card interchange down by 0.50 to 1.00 percent versus a Stripe flat-rate that processes the same card at the same blended 2.9 percent, per Mastercard interchange criteria. On a $50,000 B2B invoice, that delta is $250 to $500 saved per transaction.

The catch sits in the contract. Three-year terms with $295 to $495 early termination fees are standard. PCI compliance fees of $99 to $199 per year and monthly minimums of $25 are common. Gateway and hardware fees vary by sales rep.

Who it fits: brick-and-mortar retailers, restaurants, B2B sellers above $250,000 monthly, anyone with a stable card mix willing to sign a contract for the savings.

Who should avoid it: startups, founders without statement-reading help, anyone who needs published pricing for board reporting.

Helcim

Helcim publishes interchange-plus on the public site: IC + 0.40 percent + 8 cents in-person, IC + 0.50 percent + 25 cents online, with automatic volume tiers that lower the markup as monthly volume rises (helcim.com/pricing). No monthly fee, no PCI fee, no setup fee, no contract.

For a $100,000-per-month online merchant, the effective rate runs roughly 2.15 to 2.35 percent depending on card mix, well under Stripe's flat 2.9 percent and inside the range a Worldpay rep will quote, but without a contract or ETF. Helcim's automatic volume discounts kick in at $25,000 and again at $50,000 monthly, dropping the percentage markup by roughly 0.05 percent at each tier. The discount is published and applies without renegotiation.

Helcim caps out before enterprise complexity: there is no dedicated implementation team, no integrated surcharging program, and phone support is business-hours only.

Who it fits: $25,000 to $200,000 monthly merchants who want interchange-plus transparency without a multi-year commitment. Strong for e-commerce SMBs and professional services.

Who should avoid it: high-risk verticals, very high ticket B2B requiring Level 3 specialist setup, merchants needing 24/7 phone support.

Stax

Stax sells a subscription model: $99 per month plus interchange plus 8 cents per in-person transaction or 18 cents online, with no per-transaction percentage markup on the processor side (staxpayments.com/pricing).

The math only works above roughly $25,000 to $30,000 in monthly card volume. At $250,000 monthly, the subscription is amortized at about 0.04 percent of volume, putting the effective rate at roughly 2.10 to 2.30 percent including interchange and per-transaction fees, competitive with Worldpay and slightly under Helcim's tiered markup.

Who it fits: $50,000 to $500,000 monthly merchants with a stable card mix who want predictable monthly cost and zero percentage markup.

Who should avoid it: seasonal merchants whose volume drops below $25,000 in slow months, and businesses with high keyed-in volume where the ticket size is low.

Verdict

Stripe wins the Stripe vs Worldpay matchup for merchants under $80,000 in monthly card volume, online-first businesses, and any operator who needs developer documentation and same-day setup. The flat 2.9 percent plus 30 cents is rarely the lowest possible rate, but it ships fast and avoids contract friction.

Worldpay wins above $250,000 monthly when a stable card mix and willingness to sign a 1 to 3 year contract translate into 0.40 to 0.70 percent in interchange-plus savings. That delta is $1,000 to $1,750 per month at $250K volume, $5,000 to $8,750 at $1M volume, per the Visa and Mastercard interchange schedules cited above.

Between $80,000 and $250,000 monthly, the smarter move is usually neither. Helcim's published interchange-plus or Stax's subscription model often beats both on effective rate without the Worldpay contract length or the Stripe blended markup. For B2B sellers running corporate card volume, neither flat-rate Stripe nor a generic Worldpay quote is correct without Level 3 data submission confirmed in writing.