Cost of Payment Processing Solutions for Small Professional

Small professional services businesses can expect payment processing costs to range from 1.5% to 3.5% per transaction in 2025-2026, plus monthly fees. This guide details fee structures, hidden costs, and strategies for consultants, lawyers, and therapists.

For small professional services businesses, understanding the cost of payment processing solutions for small professional services businesses 2025-2026 is not just about managing expenses - it's about safeguarding profitability and ensuring operational efficiency. Businesses like consultants, law firms, accountants, and therapists can expect payment processing costs to range from 1.5% to 3.5% per transaction, plus various fixed and variable fees, depending on the provider, transaction type, and volume. This guide provides a detailed breakdown of current and projected payment processing expenses, tailored specifically for the professional services sector, offering clear insights to inform your financial decisions.

Dentist accepting payment on a Square Terminal, illustrating cost of payment processing solutions for small professional services businesses 2025 2026

Dentist accepting payment on a Square Terminal, illustrating cost of payment processing solutions for small professional services businesses 2025 2026

What are the Typical Payment Processing Costs for Small Professional Services Businesses in 2025-2026?

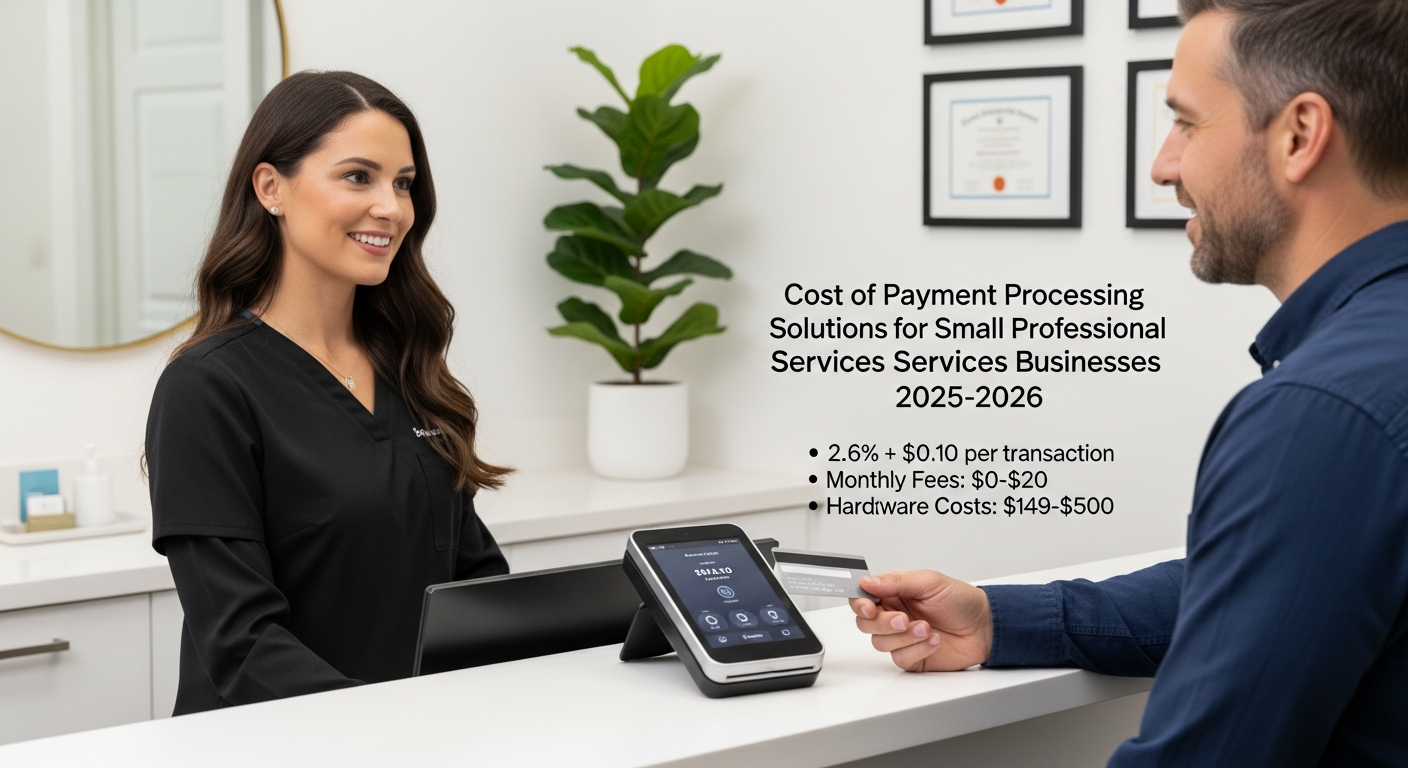

Typical payment processing costs for small professional services businesses in 2025-2026 generally include a combination of per-transaction fees, monthly fees, and various incidental charges. For card-present transactions, expect rates from 1.5% to 2.5%, while card-not-present (online, phone) transactions, common in professional services, often incur higher fees, ranging from 2.5% to 3.5% or more. Monthly fees can vary from $0 to $75, depending on the service tier and included features.

For instance, a small law firm with an average transaction size of $1,500 might face a 2.9% + $0.30 fee for online payments, equating to $43.80 per transaction. A therapist with an average session fee of $150, also processed online, would pay $4.65 per transaction at the same rate. These percentages are crucial for businesses with varying average ticket sizes. Data suggests that professional services often have higher average ticket sizes compared to retail, making percentage-based fees a significant cost factor.

Beyond transaction fees, professional services businesses must budget for PCI compliance fees (typically $10-$30 monthly or annually), chargeback fees ($20-$50 per incident), and potential setup fees (often waived, but can be $50-$200). Early termination fees, though less common with modern processors, can still apply and range from $150 to $500. Understanding the full spectrum of these charges is essential for accurate financial planning.

How Do Different Payment Processing Pricing Models Impact Professional Services Businesses?

Different payment processing pricing models - interchange-plus, tiered, flat-rate, and subscription-based - each have distinct impacts on the bottom line for professional services businesses. Selecting the right model depends heavily on transaction volume, average ticket size, and the predictability of revenue streams.

Interchange-Plus Pricing: This model is generally considered the most transparent and often the most cost-effective for businesses with higher transaction volumes or larger average ticket sizes. It involves a direct pass-through of the interchange fee (set by card networks like Visa and Mastercard) plus a small, fixed markup from the processor (e.g., 0.20% + $0.10). For a consulting firm with high-value, infrequent invoices, this transparency allows for precise cost prediction and often lower overall percentages. This model is particularly beneficial for businesses that process a mix of card types, as it reflects the actual cost of each card. Tiered Pricing: While seemingly simple, tiered pricing can be opaque and often more expensive. Processors categorize transactions into "qualified," "mid-qualified," and "non-qualified" tiers, each with different rates. Transactions that don't meet strict criteria often fall into higher-cost tiers. This model can be unpredictable for professional services, as factors like card type (rewards, corporate), entry method (swiped vs. keyed-in), and transaction amount can push payments into more expensive tiers. It's generally less recommended due to its lack of transparency and potential for inflated costs. Flat-Rate Pricing: Popular with newer businesses and those with lower, consistent transaction volumes, flat-rate pricing offers simplicity with a single percentage and per-transaction fee (e.g., 2.9% + $0.30 for online, 2.7% + $0.05 for in-person). While easy to understand, it can be more expensive for businesses with high average ticket sizes or those processing a significant volume of lower-interchange-cost cards. A small therapy practice with many consistent, lower-value transactions might find this model convenient, but a legal practice with fewer, high-value transactions could pay more than necessary. For a deeper dive into how these structures compare, see our guide on Top Payment Platforms Compared: Pricing Benchmarks, Risk Factors, and Best-Fit Scenarios. Subscription/Membership Pricing: Also known as "cost-plus" or "zero-fee" (though fees are always present), this model involves a fixed monthly fee plus interchange costs, often with very low or zero per-transaction markups. This can be highly advantageous for professional services businesses with substantial monthly processing volumes, as it significantly reduces the percentage-based costs. For example, a firm processing over $10,000 monthly might pay a $50-$100 monthly fee and then only interchange rates, leading to substantial savings compared to flat-rate or tiered models.

What Specific Cost Implications Arise from Accepting Payments for Recurring Services or Retainers?

Accepting payments for recurring services or retainers, common for consultants, accountants, and legal firms, introduces specific cost considerations related to subscription billing and tokenization. While convenient for clients and crucial for predictable revenue, these transactions are typically card-not-present, leading to higher base transaction fees (e.g., 2.9% - 3.5% + $0.30).

Many payment processors offer specialized recurring billing features, which may come with an additional monthly fee (e.g., $10-$50) or be included in higher-tier plans. These features often include card updater services, which automatically update expired or reissued credit card numbers, reducing failed payments and associated administrative costs. While these services add a small cost, they significantly improve payment success rates and client retention, offsetting the expense. For more on optimizing these processes, explore Payment Advisory Solutions: Optimizing Your Merchant Operations.

What are the Hidden Costs and Less Obvious Fees Professional Services Businesses Should Be Aware of?

Beyond the headline transaction rates, professional services businesses must scrutinize statements for a range of hidden or less obvious fees that can significantly inflate processing costs. These include batch fees, statement fees, non-compliance fees, and chargeback-related expenses.

Batch Fees: Some processors charge a small fee (e.g., $0.10 - $0.25) each time you "batch out" or settle your daily transactions. While minor individually, these can add up over time. Statement Fees: A monthly fee (e.g., $5 - $15) for providing a paper or electronic statement, even if you manage your account online. PCI Non-Compliance Fees: If your business fails to meet PCI DSS (Payment Card Industry Data Security Standard) requirements, processors can levy substantial monthly fees (e.g., $20 - $100) until compliance is achieved. This is a critical area for professional services, especially those handling sensitive client data. Chargeback Fees: As mentioned, these are significant. Each chargeback can cost $20-$50, regardless of whether you win the dispute. Minimizing chargebacks through clear service agreements and robust customer communication is paramount. For strategies to mitigate these, refer to our guide on Reduce Merchant Account Fees: Expert Strategies & Pricing Insights for 2026. Address Verification Service (AVS) Fees: A small fee (e.g., $0.01 - $0.10) for verifying the cardholder's address, primarily for card-not-present transactions to prevent fraud. While beneficial, it's an added cost. Gateway Fees: If using a separate payment gateway, there will be monthly fees (e.g., $10-$30) and per-transaction fees (e.g., $0.05-$0.15) for routing transactions. Understanding the distinction between a gateway and a processor is key; see Payment Gateway vs. Processor: 2026 Pricing, Functions & Best Choice.

How Do Payment Processors Integrate with Common Professional Services Software and What are the Cost Implications?

Seamless integration with existing practice management, accounting, and CRM software is a major factor for professional services businesses, impacting efficiency and potentially cost. Many processors offer direct integrations or API access to platforms like QuickBooks Online, Clio (for legal), MyCase (legal), TherapyNotes (therapy), and Salesforce.

Direct integrations often streamline billing, reconciliation, and reporting, reducing manual data entry and errors. Some processors charge additional fees for premium integrations or access to their API, while others include it in their standard packages. For example, a processor might offer a QuickBooks integration for an extra $15/month, or it might be part of a higher-tier subscription plan. The cost savings from increased efficiency and reduced administrative overhead often outweigh these integration fees.

When evaluating processors, professional services firms should prioritize those with robust, well-documented integrations with their core software. This ensures a smooth workflow and avoids the need for costly third-party middleware or custom development. The ability to automatically sync payment data with accounting software, for instance, can save hours of manual reconciliation each month, a significant hidden benefit.

Architect using a Clover Flex terminal for client payment, showing cost of payment processing solutions for small professional services businesses 2025 2026

Architect using a Clover Flex terminal for client payment, showing cost of payment processing solutions for small professional services businesses 2025 2026

What are the Compliance Considerations that Impact Payment Processing Choices and Costs for Professional Services?

Professional services businesses, particularly those in healthcare (e.g., therapists, medical consultants) and legal fields, face unique compliance requirements that directly influence payment processing choices and costs. HIPAA compliance for protected health information (PHI) and adherence to IOLTA (Interest on Lawyers Trust Accounts) regulations for legal trust funds are paramount.

HIPAA Compliance: Healthcare professionals must ensure their payment processor and associated systems are HIPAA compliant, meaning they protect PHI during transactions. This often requires Business Associate Agreements (BAAs) with processors and may necessitate using specific, more secure payment portals or encrypted data transmission methods, which can sometimes incur higher costs or require specialized solutions. Not all general-purpose processors are fully equipped for HIPAA, so due diligence is crucial. IOLTA/Trust Accounts: Law firms must segregate client funds into trust accounts, separate from operating accounts. Payment processors for legal practices need to facilitate this segregation, often with specific reporting features that track funds accurately. While not a direct fee, choosing a processor that understands and supports IOLTA compliance is vital to avoid legal and financial penalties. Some legal-specific payment solutions are designed with these requirements in mind, though they might have slightly different fee structures.

Ensuring PCI DSS compliance is universal for all businesses accepting card payments. Failure to comply can lead to fines and increased processing fees. Many processors offer tools and support to help businesses achieve and maintain PCI compliance, sometimes for an additional fee.

How Will New Payment Technologies Affect Processing Costs for Professional Services in 2025-2026?

The payment landscape is rapidly evolving, and new technologies like real-time payments (RTP), blockchain-based payments, and enhanced virtual cards are poised to affect processing costs for professional services in 2025-2026. These innovations offer both opportunities for cost reduction and potential new fee structures.

Real-Time Payments (RTP) and FedNow: The expansion of RTP networks, including the Federal Reserve's FedNow service, allows for instant, irrevocable fund transfers. For professional services, this means faster access to funds, improving cash flow. While current bank-to-bank RTP fees are often lower than card processing fees (e.g., a few dollars per transaction or even free for some banks), widespread adoption by processors for client payments is still developing. As adoption grows, expect lower-cost alternatives to traditional card payments, particularly for larger B2B transactions or retainer payments. Blockchain and Cryptocurrency: While still niche for mainstream professional services, blockchain-based payments (cryptocurrency) offer the potential for very low transaction fees, bypassing traditional intermediaries. However, volatility, regulatory uncertainty, and the need for specialized wallets currently limit their widespread use. In 2025-2026, expect more processors to offer crypto payment acceptance, likely with conversion fees or higher transaction percentages due to the added complexity and risk.

- Enhanced Virtual Cards: Virtual cards are gaining traction, especially for B2B payments. They offer enhanced security and can sometimes come with lower interchange rates than traditional credit cards, particularly for corporate clients. Professional services accepting these could see slight reductions in per-transaction costs. For more on optimizing online fees, check out Online Payment Processing Fees Comparison -2026: Navigating the Evolving Landscape.

Overall, the trend is towards greater payment method diversity. Professional services businesses should monitor these developments, as embracing lower-cost alternatives like ACH and RTP for appropriate transactions can significantly reduce overall processing expenses.

What are the Best Strategies for Professional Services Businesses to Minimize Payment Processing Costs and Chargebacks?

Minimizing payment processing costs and chargebacks requires a proactive, multi-faceted approach, focusing on optimizing fee structures, leveraging technology, and implementing robust client communication. For professional services, these strategies directly impact profitability and operational efficiency.

Strategies to Minimize Processing Costs:

- Negotiate Rates: Don't hesitate to negotiate with processors, especially if you have a significant processing volume. Present competitor quotes to secure better interchange-plus markups or lower monthly fees. Our guide on Lowering Merchant Account Fees: 2026 Pricing & Cost Reduction Strategies offers detailed negotiation tactics.

- Choose the Right Pricing Model: As discussed, interchange-plus or subscription models are often more cost-effective for professional services with predictable, higher transaction volumes. Re-evaluate your model annually.

- Encourage ACH Payments: For larger invoices, retainers, or recurring payments, encourage clients to pay via ACH (Automated Clearing House). ACH transaction fees are significantly lower, typically $0.20 - $1.50 per transaction, regardless of the amount, compared to percentage-based credit card fees. This is a substantial saving for a $5,000 legal retainer.

- Implement Surcharging (Where Legal): In some states, businesses can legally pass a portion of credit card processing fees to the customer, typically up to 4%. While this can offset costs, it requires clear disclosure and may impact client relationships. Always check local regulations.

- Optimize for Card-Not-Present Transactions: Ensure your online payment gateway uses advanced fraud tools like AVS and CVV verification. These reduce fraud risk and can sometimes qualify transactions for slightly lower interchange rates.

- Regularly Review Statements: Scrutinize your monthly statements for unexpected fees, rate creep, or incorrect charges. Processors can sometimes quietly adjust rates or introduce new fees. For guidance on this, see Payment Processor Fees & Conversion Rates: 2026 Merchant Evaluation.

Strategies to Minimize Chargebacks:

- Clear Service Agreements: Ensure all professional services agreements, contracts, and retainer terms are explicit, detailed, and signed by the client. This provides strong evidence in case of a dispute.

- Transparent Billing Descriptors: Use clear and recognizable billing descriptors on client statements. A generic descriptor can lead to "friendly fraud" where a client doesn't recognize the charge.

- Prompt Communication: Respond quickly to client inquiries and complaints. Often, a chargeback can be prevented by resolving an issue directly with the client before they contact their bank.

- Proof of Service: Maintain meticulous records of services rendered, including dates, times, communications, and deliverables. For example, a therapist should log session attendance, and a consultant should document project milestones.

- Refund Policy: Have a clear and accessible refund policy. Offering a refund can sometimes be less costly than fighting a chargeback.

By implementing these strategies, professional services businesses can significantly reduce their overall payment processing expenditures and protect their revenue streams.

Conclusion: Optimizing Payment Processing for Professional Services in 2025-2026

Navigating the cost of payment processing solutions for small professional services businesses in 2025-2026 requires a nuanced understanding of fee structures, integration capabilities, and compliance requirements. While transaction fees remain a primary concern, hidden costs, the impact of different pricing models, and the unique needs of recurring revenue streams demand careful consideration. By strategically choosing payment partners, leveraging lower-cost payment methods like ACH, and proactively managing potential pitfalls like chargebacks, professional services firms can optimize their payment processing expenses and bolster their financial health. MyPayAdvisor is here to help you analyze your specific needs and find the most cost-effective and compliant payment solutions for your practice. Contact us today for a personalized consultation.

[Image: cost of payment processing solutions for small professional services businesses 2025 2026 practical visual example 1] [Image: cost of payment processing solutions for small professional services businesses 2025 2026 practical visual example 2]

Physiotherapist accepting mobile payment with a Stripe Reader M2, illustrating cost of payment processing solutions for small professional services businesses 2025 2026

Physiotherapist accepting mobile payment with a Stripe Reader M2, illustrating cost of payment processing solutions for small professional services businesses 2025 2026

FAQ

What is the average credit card processing fee for small professional services in 2026?

In 2026, the average credit card processing fee for small professional services typically ranges from 1.5% to 3.5% per transaction, plus a fixed fee (e.g., $0.10-$0.30). Card-not-present transactions, common for online invoicing, generally incur higher rates within this range.

Are ACH payments cheaper than credit card payments for professional services?

Yes, ACH payments are significantly cheaper than credit card payments for professional services. ACH fees typically range from $0.20 to $1.50 per transaction, regardless of the amount, offering substantial savings for larger invoices or recurring retainers compared to percentage-based credit card fees.

How do PCI compliance fees affect professional services businesses?

PCI compliance fees are typically a monthly or annual charge (e.g., $10-$30) levied by payment processors to ensure businesses meet data security standards. Failure to comply can result in much higher non-compliance fees (e.g., $20-$100 per month) and potential fines, making compliance crucial for professional services handling sensitive client data.

What are the main hidden costs in payment processing for professional services?

The main hidden costs for professional services in payment processing include batch fees, statement fees, PCI non-compliance fees, Address Verification Service (AVS) fees, and significant chargeback fees ($20-$50 per incident). These can add up quickly if not properly accounted for.

Should professional services businesses consider subscription-based payment processing models?

Yes, professional services businesses with substantial and consistent monthly processing volumes (e.g., over $10,000) should strongly consider subscription-based payment processing models. These models often involve a fixed monthly fee plus interchange rates, which can lead to significantly lower overall percentage costs compared to flat-rate or tiered models.