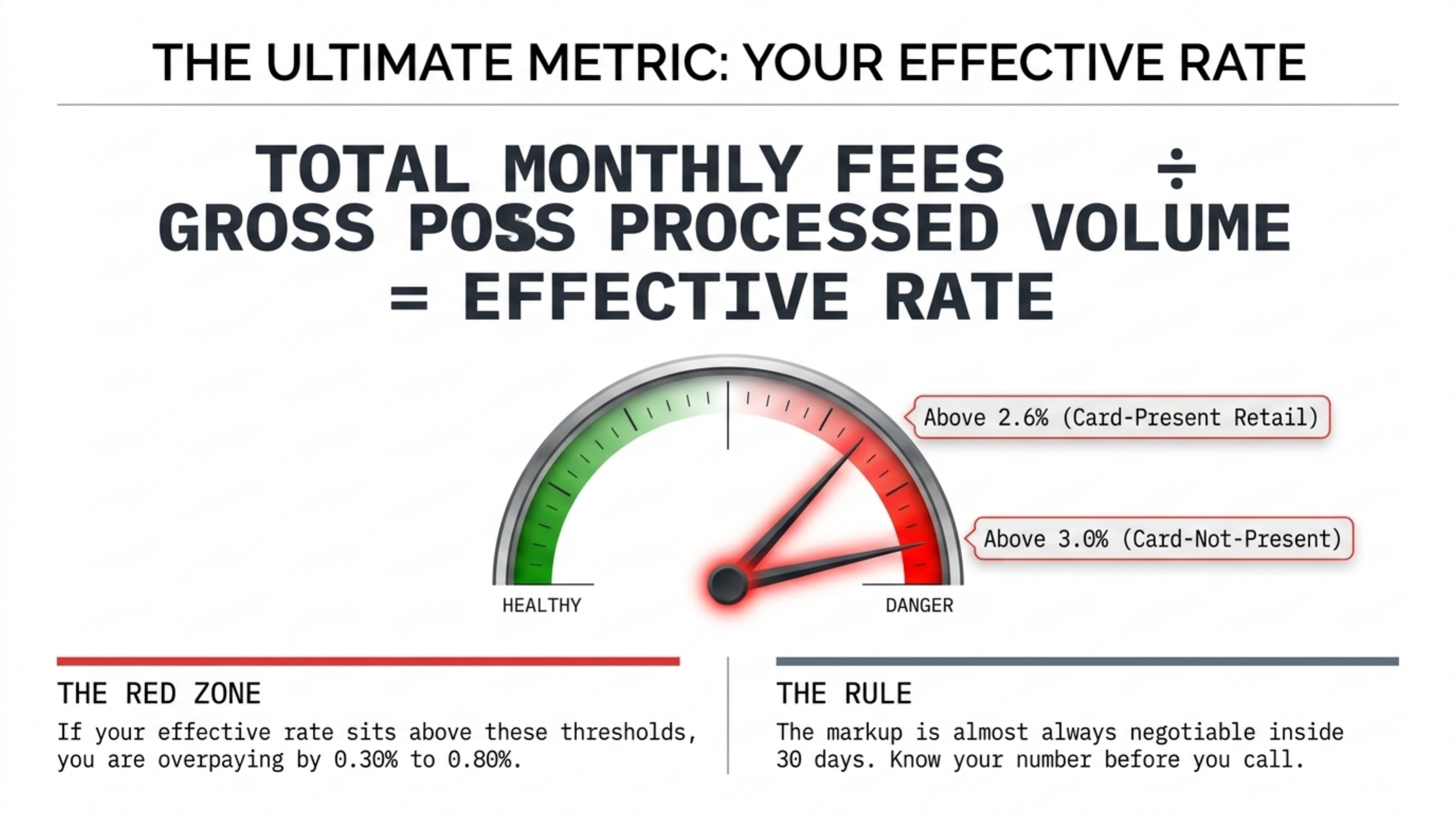

TL;DR

Your merchant statement has three real cost buckets: interchange paid to the card-issuing bank, assessments paid to Visa and Mastercard, and the processor's markup. Everything else is packaging. Calculate your effective rate by dividing total fees by gross processed volume. If it sits above 2.6 percent on card-present retail or above 3.0 percent on card-not-present, you are overpaying by 0.30 to 0.80 percent, and the markup is almost always negotiable inside 30 days.

What this actually is

A merchant statement is the monthly invoice from your payment processor that itemizes every fee charged against your card volume for the prior cycle. It is not one fee. It is a stack of three separate cost layers bolted together: interchange (set by Visa, Mastercard, Discover, and American Express and paid to the bank that issued the customer's card), assessments (paid to the card brands themselves), and processor markup (the only line your processor actually controls). The Federal Reserve's payments system data tracks the structure of these fees across the industry, and both Visa's US Interchange Reimbursement Fee schedule (PDF) and Mastercard's published interchange criteria publish their rates openly.

Most statements run 6 to 20 pages, and the page count is not correlated with clarity. A 6-page Stripe statement can hide markup just as well as a 20-page First Data statement, because both bundle interchange, assessments, and markup into combined line items. The job of reading a statement is to unbundle those three layers and confirm that interchange and assessments match the published rates, then isolate what the processor actually charged on top.

A merchant statement is the monthly invoice that itemizes interchange, card-brand assessments, and processor markup against your gross card volume.

How it works under the hood

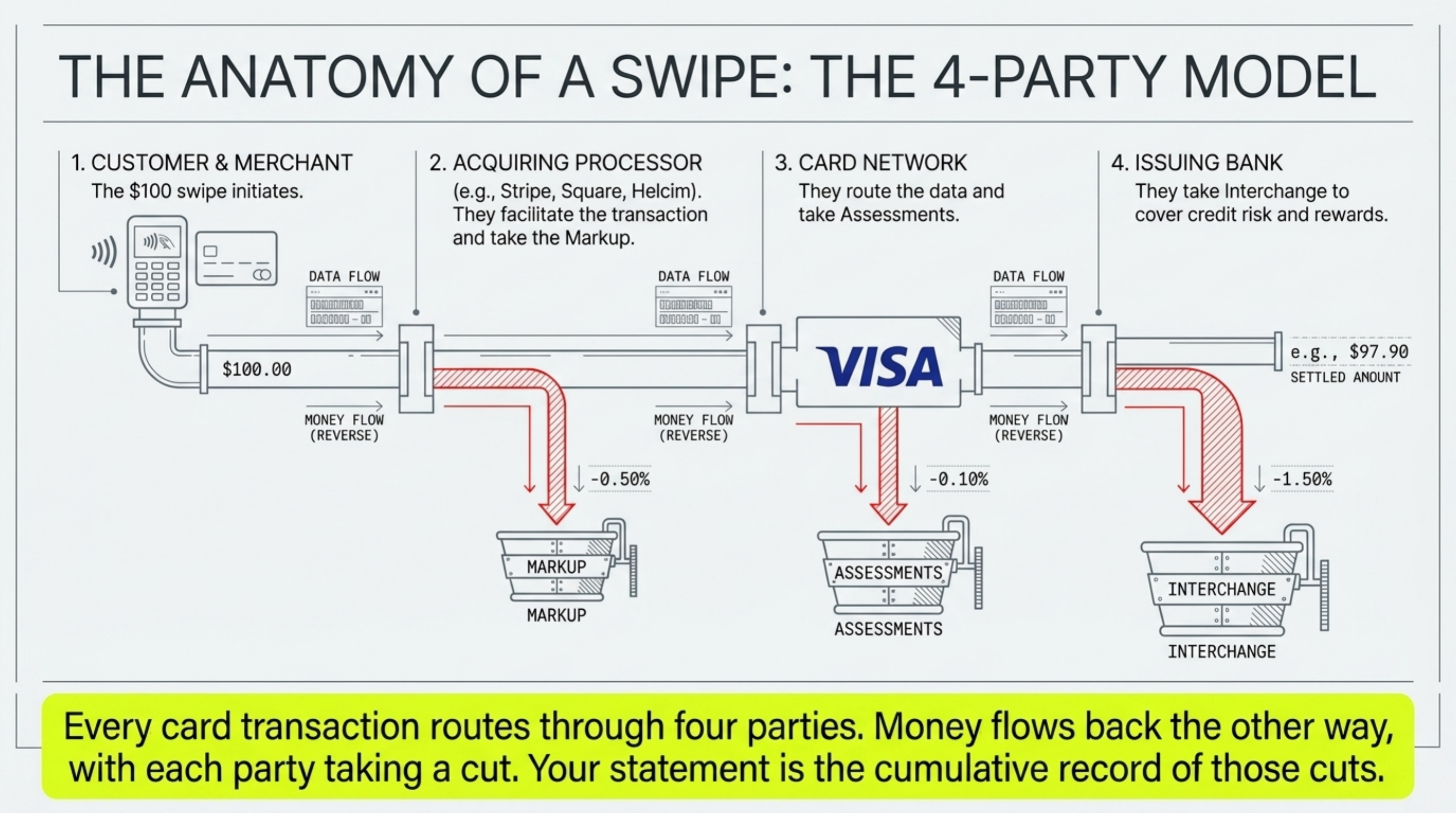

Every card transaction routes through four parties: the merchant, the acquiring processor, the card network (Visa, Mastercard, Discover, Amex), and the issuing bank. Money flows back the other way, with each party taking a cut. Your statement is the cumulative record of those cuts for the month.

The fee stack works in this order:

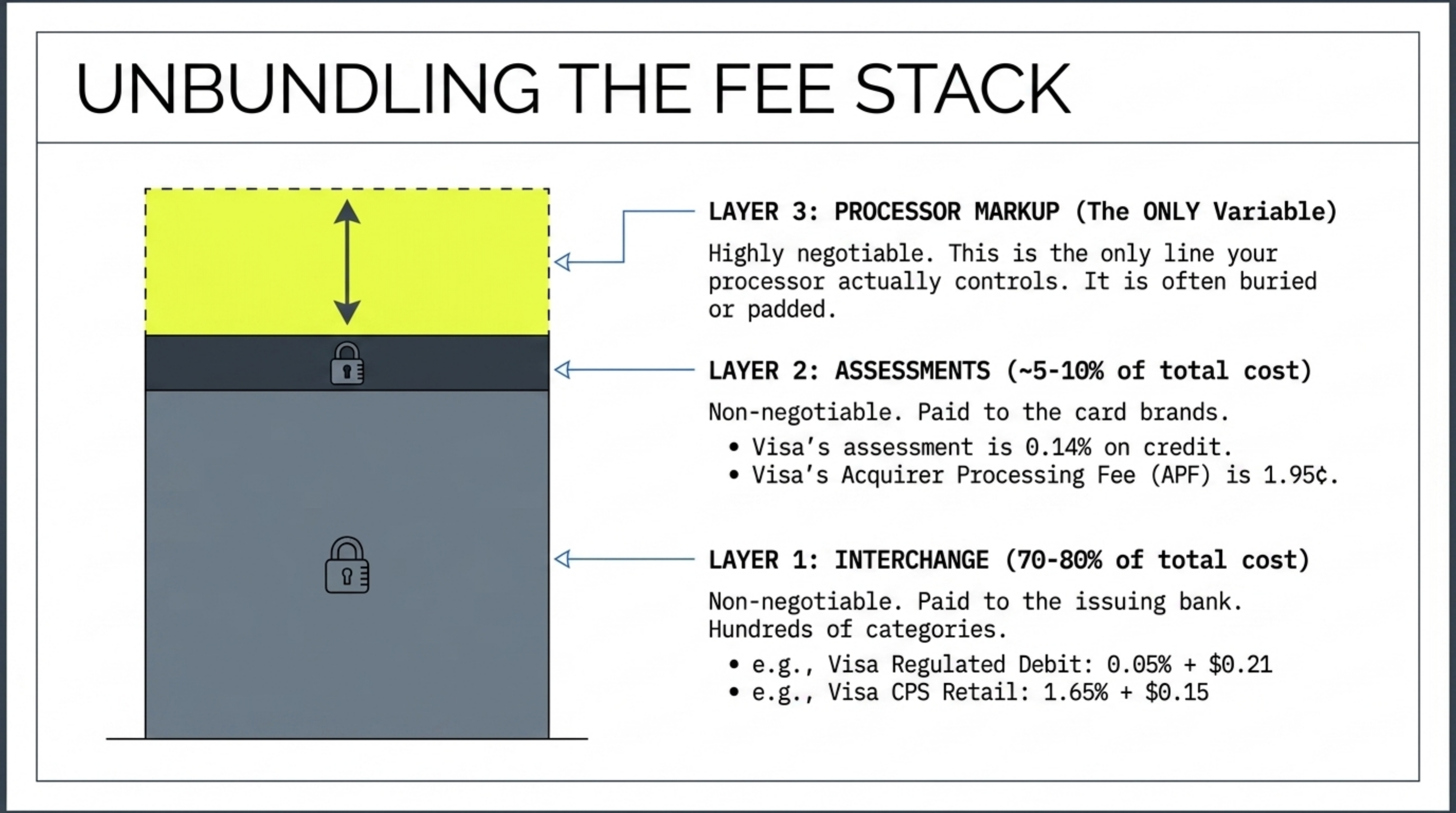

- Interchange. The largest component, typically 70 to 80 percent of total cost. Set by the card networks, paid to the issuing bank. The Visa US Interchange Reimbursement Fee schedule lists hundreds of category-specific rates; a card-present Visa Signature credit card runs 1.65 percent plus 10 cents under the EIRF category, while CPS Retail Debit (regulated) runs 0.05 percent plus 22 cents.

- Assessments. Paid to the card brands. Visa's assessment is 0.14 percent on credit and 0.13 percent on debit per the Visa fee schedule; Mastercard's published criteria set 0.1375 percent on transactions under $1,000 and 0.01 percent on transactions over $1,000. On top of assessments, both networks add per-transaction fees: Visa's Acquirer Processing Fee (APF) is 1.95 cents on credit and 2.0 cents on debit; Mastercard's Network Access and Brand Usage (NABU) fee is 1.95 cents (both documented in the Visa schedule and on the Mastercard interchange page).

- Processor markup. The only variable. On an interchange-plus contract, this is disclosed: for example, 0.25 percent plus 10 cents above interchange. On tiered or flat-rate pricing, it is buried inside the bucket rate. Stripe's published flat rate of 2.9 percent plus 30 cents per online transaction is one example; Square's published 2.6 percent plus 10 cents for in-person card-present is another. Both bundle interchange, assessments, and markup into a single number.

- Per-occurrence fees. Monthly statement fee, PCI compliance fee, batch fee, chargeback fee, gateway fee, monthly minimum.

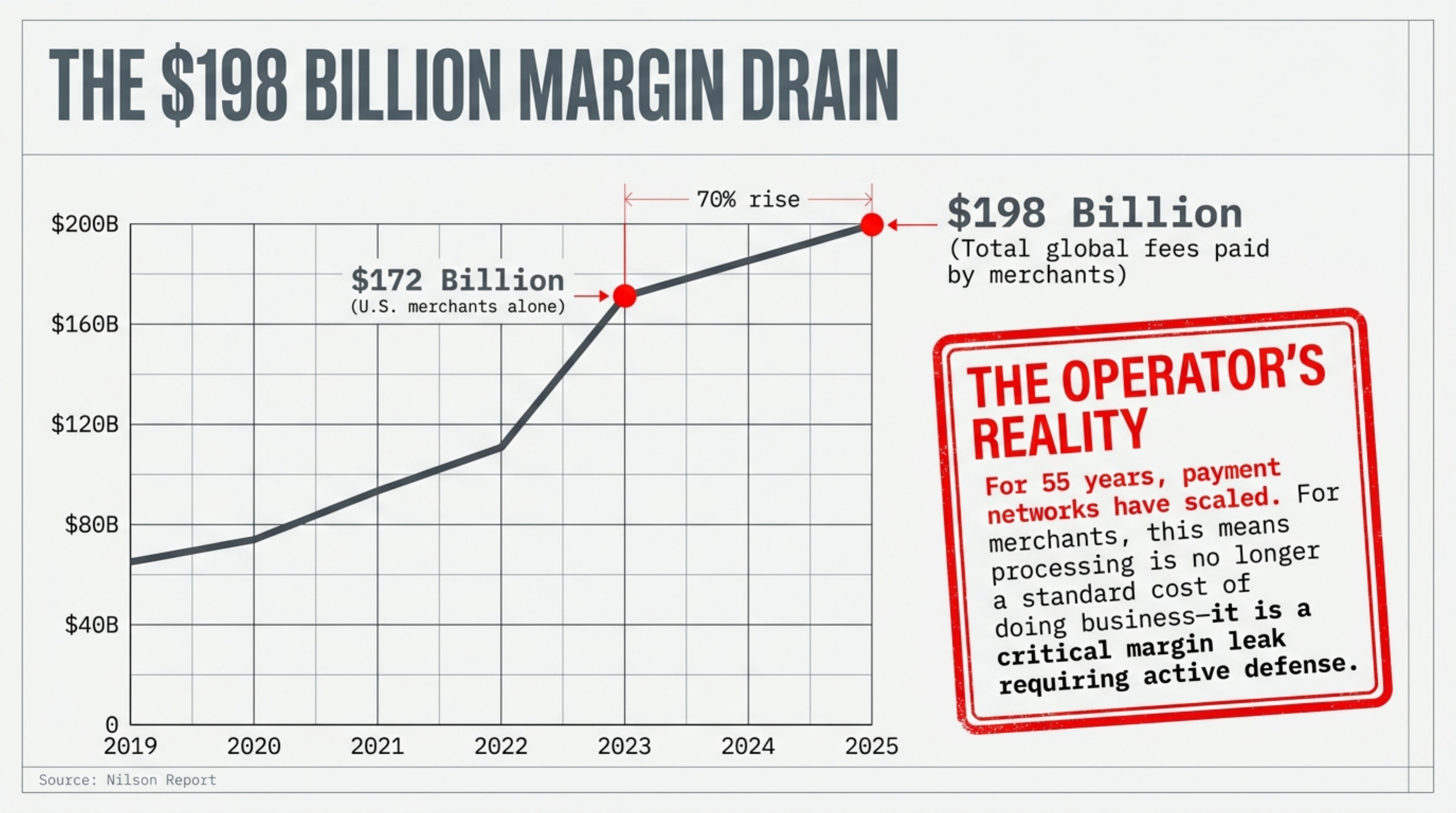

According to the Nilson Report, U.S. merchants paid roughly $172 billion in card processing fees in 2023. The bulk of that flowed through this same four-party model.

Where it goes wrong for operators

Five patterns drain merchant margin month after month, and almost all of them are invisible unless you know where to look.

1. Tiered pricing rebucketing. A tiered plan promises a qualified rate of, say, 1.69 percent. In practice, 30 to 60 percent of volume gets routed to mid-qualified (2.45 percent) or non-qualified (3.25 percent) tiers based on opaque criteria like card type, AVS mismatch, or batch timing. On $200K monthly volume, that downgrade alone costs $1,200 to $2,400 per month.

2. Padded assessments. Visa's published assessment is 0.14 percent per the Visa fee schedule. Some processors charge 0.15 or 0.16 percent and pocket the difference. On $500K monthly volume, 2 basis points of padding equals $100 per month, or $6,000 over a 60-month term.

3. PCI non-compliance fees. If you do not complete the annual PCI self-assessment questionnaire (SAQ A through SAQ D depending on processing environment), you get hit with a $19.95 to $39.95 monthly non-compliance fee on top of the standard $5 to $15 PCI compliance fee. Transparent processors like Helcim publish a zero PCI fee policy as a differentiator, while legacy processor schedules typically list both a monthly compliance fee and a separate non-compliance penalty in their published merchant disclosures. The processor has no incentive to remind you before your SAQ deadline lapses.

4. Junk fees with marketing names. "Regulatory product fee," "network integrity fee," "merchant club fee," "IRS reporting fee." These are pure processor revenue dressed up as compliance. A typical statement carries 3 to 5 of them, ranging from $5 to $25 each, and none appear on transparent pricing pages like Stripe's or Square's.

5. Average ticket and volume cap clauses. Your application listed an average ticket of $85. You start running $400 tickets. The processor flags it and downgrades transactions to non-qualified or imposes a surcharge. This clause sits in section 11 of most contracts and almost no merchant reads it.

Worked example with real numbers

Vertical: independent specialty coffee retailer, 3 locations. Monthly volume: $185,000. Average ticket: $14.20. Transaction count: 13,028. Card mix: 78 percent credit, 22 percent debit. Current pricing: tiered (1.79% qualified / 2.39% mid / 3.05% non-qual) plus 12 cents per transaction. Statement effective rate, calculated below.

Pull the totals page first. Gross sales: $185,000. Total fees charged: $5,217. Effective rate: 5,217 divided by 185,000 equals 2.82 percent. That is the number to beat.

Now unbundle. On the fee detail page:

- Qualified volume ($72,150 at 1.79% + 12¢): $1,291.49 + $608.40 (per-transaction) on 5,070 txns = $1,899.89

- Mid-qualified volume ($63,900 at 2.39% + 12¢): $1,527.21 + $540.12 on 4,501 txns = $2,067.33

- Non-qualified volume ($48,950 at 3.05% + 12¢): $1,492.98 + $416.04 on 3,467 txns = $1,909.02

- Monthly statement fee: $15

- PCI compliance fee: $19.95

- Regulatory product fee: $9.95

- Batch fee (30 batches at $0.25): $7.50

That sums roughly to $5,928 on paper, but the statement shows $5,217. The gap is because volume distribution and downgrades on this statement skewed slightly differently. Either way, the effective rate is 2.82 percent.

The lesson: on low-ticket businesses, per-transaction fees do more damage than the discount rate. On high-ticket businesses, the discount rate matters more. Read your statement with your average ticket in mind.

A second scenario: B2B distributor with high tickets

Now contrast the coffee shop with a different vertical. Industrial parts distributor, business-to-business, card-not-present. Monthly volume: $420,000. Average ticket: $1,850. Transaction count: 227. Card mix: 92 percent commercial credit, 8 percent corporate. Current pricing: flat-rate at Stripe's standard published rate of 2.9 percent plus 30 cents.

Monthly math under flat-rate: $420,000 x 2.9 percent = $12,180, plus 227 transactions x $0.30 = $68.10. Total: $12,248. Effective rate: 2.92 percent. Painful on B2B, where commercial card interchange itself often runs 2.20 to 2.65 percent before any markup per the Visa commercial card categories.

Move this merchant to interchange-plus at 0.20 percent + 10 cents and add Level 2/Level 3 data submission, where the processor passes tax amount, invoice number, and line-item detail to the card networks to qualify transactions for lower commercial interchange categories. Interchange drops from a blended 2.45 percent to 2.05 percent, saving 40 basis points immediately. New math: $420,000 x 2.05 percent interchange = $8,610, plus $420,000 x 0.14 percent assessments = $588, plus $420,000 x 0.20 percent markup = $840, plus 227 x $0.10 = $22.70, plus $35 in monthly fees. Total: $10,096. Effective rate: 2.40 percent. Annual savings: $25,824.

The pattern: B2B operators on flat-rate pricing leave more money on the table than any other vertical, because flat-rate plans charge consumer-card rates on transactions that should qualify for commercial interchange with Level 2/Level 3 data. If your B2B statement shows a flat 2.9 percent or higher and no Level 2 line items, you are overpaying by 0.40 to 0.80 percent.

Operator playbook

Take the last three months of statements and run this sequence. Block 45 minutes. You will surface enough markup to fund the call to your processor.

- Calculate the effective rate. Total fees divided by gross volume. Do this for each of the last three months. If it varies by more than 0.20 percent month to month, you are on tiered pricing and getting downgraded.

- Pull every line item into three buckets. Interchange, assessments, processor markup. Most processors label them. If yours does not, that is a request you make in writing: "send me an interchange-categorized statement for the last 90 days."

- Verify assessments against published rates. Visa assessment should be 0.14 percent per the Visa fee schedule. Mastercard should be 0.1375 percent under $1,000 per the Mastercard interchange page. Network access fees (Visa APF and Mastercard NABU) should be 1.95 to 2.0 cents per transaction. Anything higher is pad, and pad is refundable.

- Identify and list every junk fee. Statement fee, PCI fee, regulatory product fee, IRS reporting fee, merchant club fee, annual fee, gateway fee. Add them up. On a typical statement, junk fees total $35 to $90 per month. Most are negotiable to zero.

- Pull the contract. Find the early termination fee clause, the auto-renewal clause, and the rate-change clause. Note all three. Most contracts allow the processor to raise rates with 30 days' notice; that is your hook for renegotiation.

- Get three competitive quotes on interchange-plus. Request quotes from a Stax-style subscription processor, a direct acquirer like Chase or Fiserv, and a payment consultant. Specify monthly volume, average ticket, and card mix. Ignore anyone who refuses to quote interchange-plus.

- Negotiate your current processor against the quotes. Email your rep: "I have three competitive offers at interchange + 0.25%. Match by end of month or I'm switching." Roughly 60 percent of merchants get a match or near-match. The processor would rather cut markup than lose the merchant ID.

- Re-run the effective rate after 30 days. Same calculation. If it dropped by 0.25 percent or more, the negotiation worked. If not, file termination paperwork and move.

Glossary of statement line items

Use this as a decoder when you sit down with your first statement audit.

- Discount rate. The percentage charged against gross volume. On tiered pricing, you will see multiple discount rates (qualified, mid-qualified, non-qualified). On interchange-plus, the discount rate is the processor's markup above true interchange.

- Per-item / per-authorization fee. A flat cent amount charged on every transaction or authorization attempt, typically 5 to 30 cents. Authorization fees apply even on declines.

- Interchange line items. Labels like "CPS Retail," "EIRF," "Visa Signature Preferred," or "MC Merit III" reference specific interchange categories from the published Visa and Mastercard schedules. Each represents a different card type and transaction environment.

- Visa Assessment Fee / Mastercard Assessment Fee. Card-brand fees of 0.14 percent and 0.1375 percent (under $1,000), respectively. Padding above these published rates is recoverable.

- Network Access / APF / NABU. Per-transaction fees from the card networks of 1.95 to 2.0 cents. NABU is the Mastercard version; APF (Acquirer Processing Fee) is Visa's.

- PCI Compliance Fee. A monthly $5 to $15 fee for the processor's PCI compliance program.

- PCI Non-Compliance Fee. An additional $19.95 to $39.95 monthly fee charged if your annual SAQ is incomplete or expired.

- Monthly Minimum. A contractual minimum in fees per month. If your actual fees are below the floor, you pay the gap.

- Batch Fee. A $0.10 to $0.25 fee for each settlement batch submitted, usually one per business day per terminal.

- Chargeback Fee. A $15 to $30 fee charged each time a customer disputes a transaction, regardless of whether you win the dispute.

- Retrieval Request Fee. A $5 to $15 fee when a card issuer requests transaction documentation, often a precursor to a chargeback.

- Statement Fee. A monthly $0 to $15 fee for producing the statement itself. Negotiable to zero in most cases.

- Regulatory Product Fee / IRS Reporting Fee. Marketing names for processor revenue. There is no actual regulatory requirement for these fees.

- Early Termination Fee. A penalty for canceling the contract before the term ends, typically $295 to $500 plus liquidated damages calculated against expected residual.