TL;DR

Most U.S. acquirers hold 5 to 10 percent of card volume as a rolling reserve, released 180 days after the originating batch settles. On $500,000 monthly volume at 8 percent, that locks $240,000 of working capital in steady state. The release clock resets every batch, the account pays no interest, and the percentage can be raised at the acquirer's discretion under most master service agreements. Pull your reserve schedule, price the locked capital at your hurdle rate, and renegotiate at renewal.

What this actually is

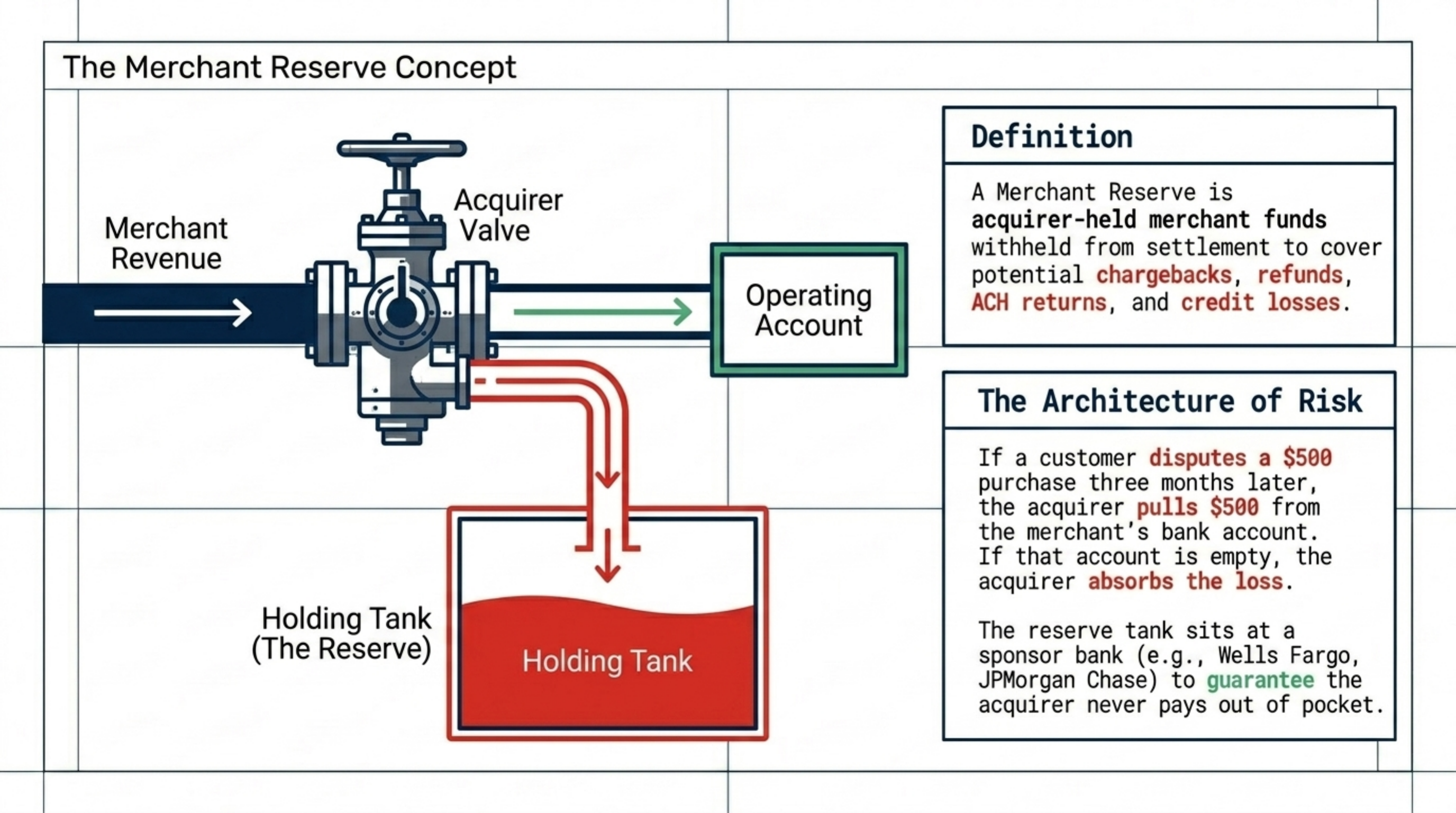

A merchant reserve is funds an acquirer withholds from settlement to cover potential chargebacks, refunds, ACH returns, and credit losses. The acquirer carries the credit risk on every card transaction. If a customer disputes a $500 purchase three months later, the acquirer pulls $500 from the merchant's bank account. If that account is empty or closed, the acquirer absorbs the loss. The reserve is the buffer that funds those clawbacks before they hit the merchant's operating cash.

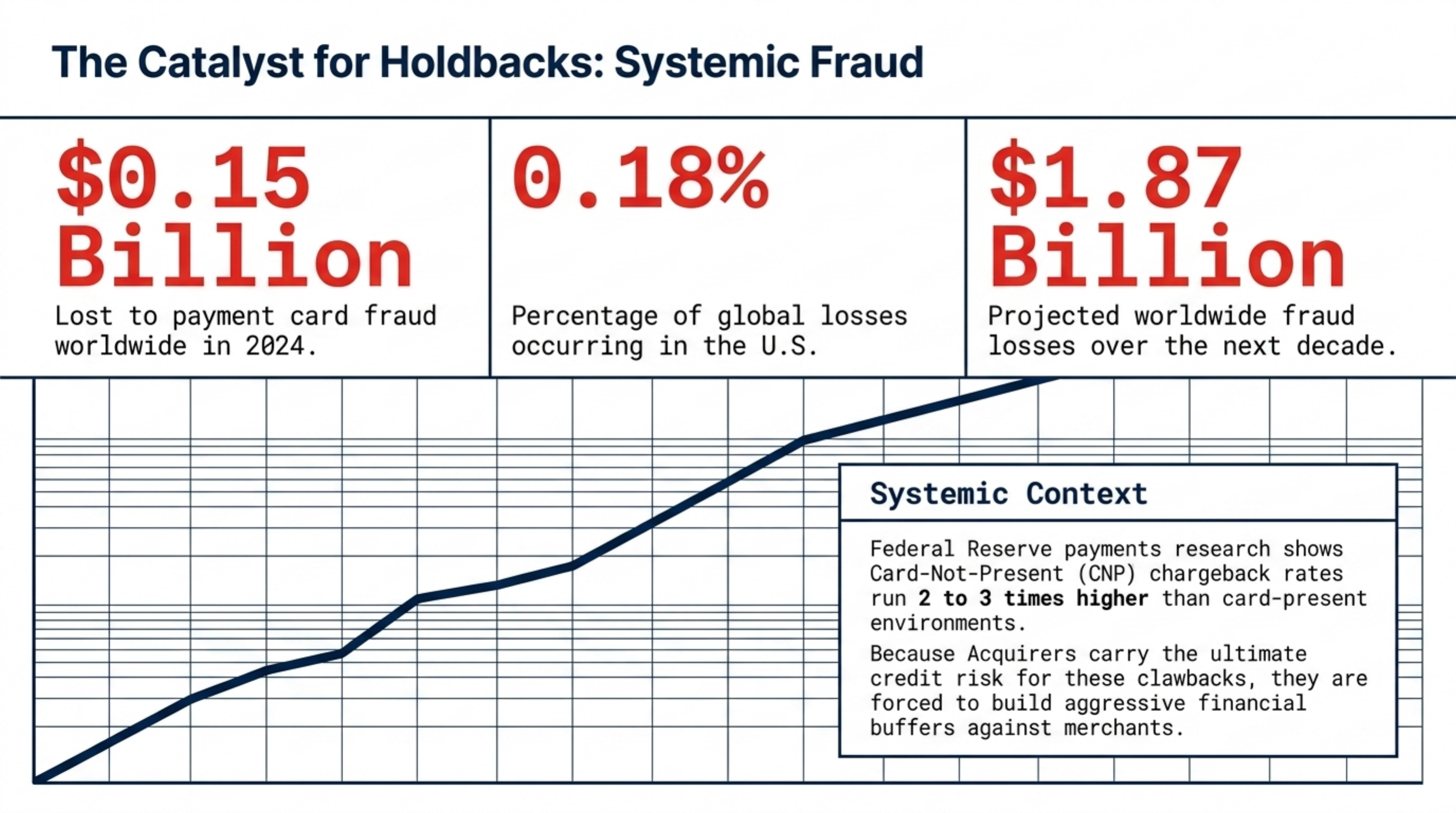

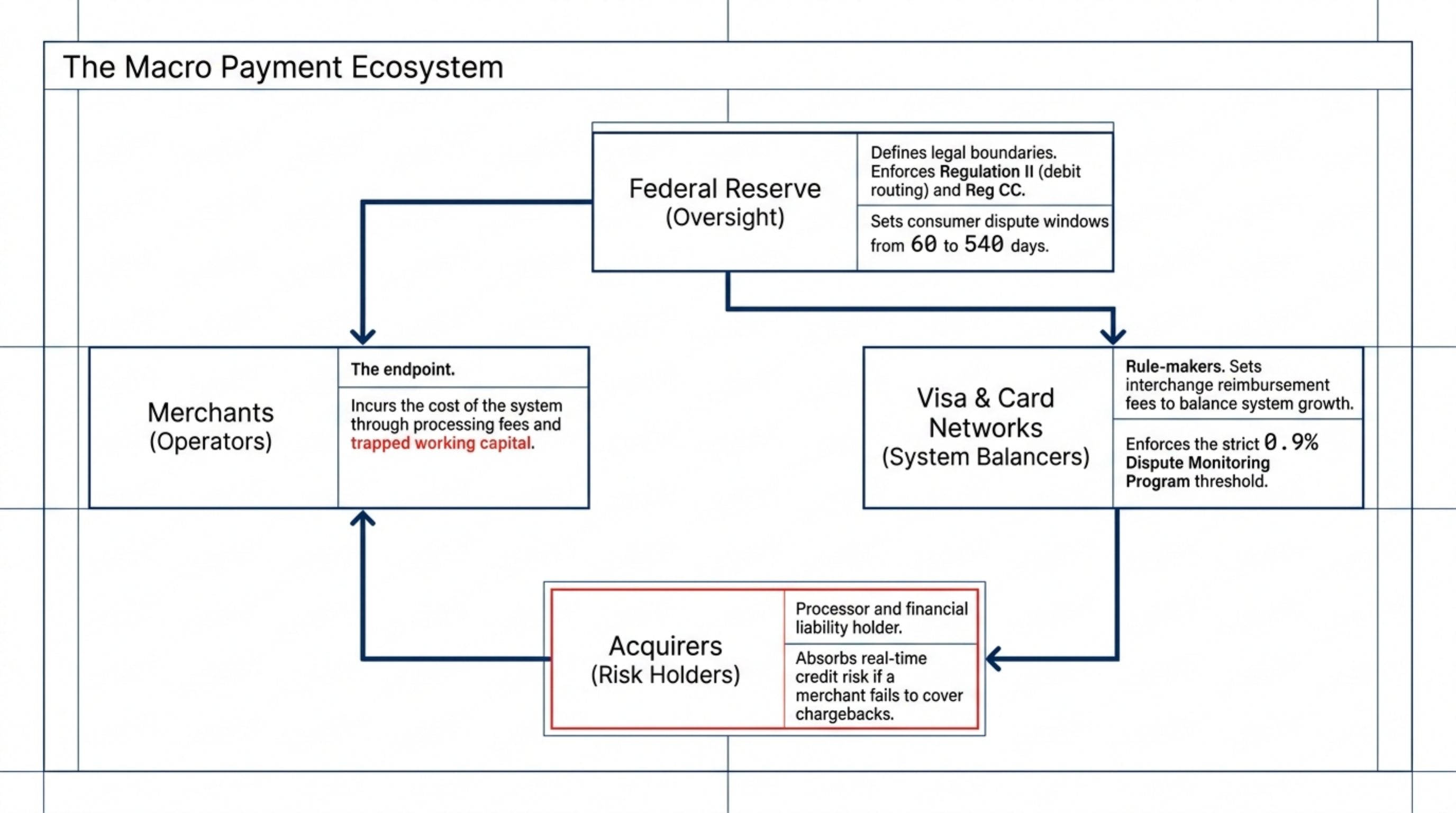

Federal Reserve payment system research shows that card-not-present chargeback rates run 2 to 3 times higher than card-present, which is why CNP merchants see reserves more often. Visa's published Dispute Monitoring Program threshold is a 0.9 percent dispute ratio, and Mastercard's Excessive Chargeback Merchant program sits at 1.5 percent. Once a merchant trips either threshold, reserve requirements escalate. The card brands do not set the reserve directly; the acquirer responds to the risk signal by adjusting the holdback.

Three reserve structures dominate U.S. processing contracts. Rolling reserve withholds a percentage of each batch for a fixed period, most commonly 180 days. Upfront reserve captures a lump sum at boarding and pays it down over months. Minimum reserve maintains a floor balance at all times, regardless of volume. Most high-risk acquirers default to rolling. Standard-risk acquirers may waive the reserve entirely above a volume threshold and a clean processing history.

Reserves are governed by the master service agreement between merchant and acquirer, not by Visa or Mastercard operating rules. Federal Reserve regulations define cardholder dispute timelines, but the reserve itself sits in the private contract.

A reserve is acquirer-held merchant funds withheld from settlement to cover chargebacks and refund risk, typically released 180 days after the originating batch.

How it works under the hood

Reserve mechanics follow a predictable settlement flow. With a 10 percent rolling reserve and a 180-day release, here is the sequence on a single $100 transaction:

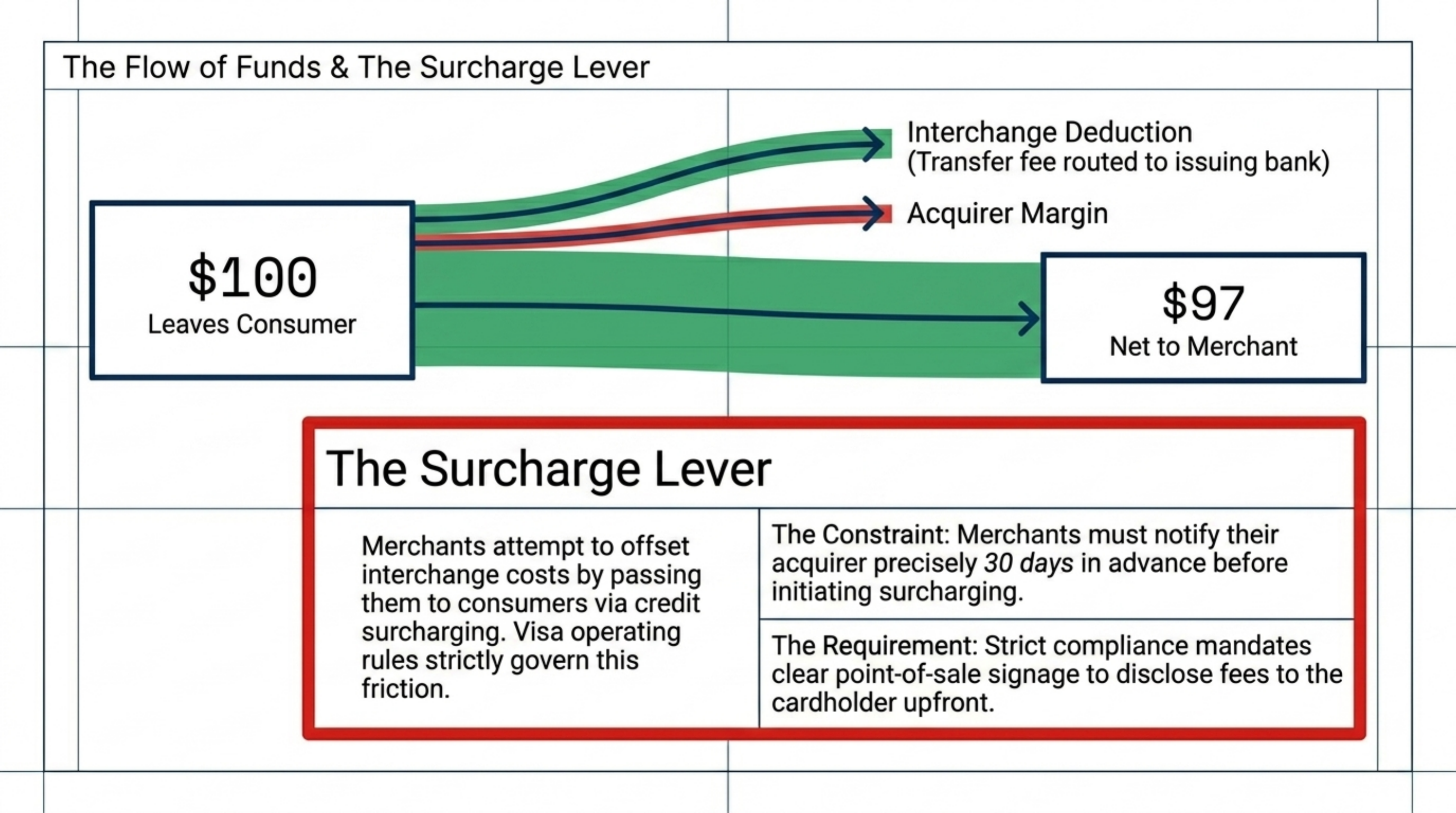

- Customer pays $100 on day zero. The card brand routes interchange and assessments to the acquirer.

- The acquirer nets the $100 against interchange, network fees, and processor markup. Net to merchant before reserve is roughly $97 on a standard consumer credit mix.

- The acquirer routes 10 percent of gross ($10) to the reserve sub-account. The merchant receives $87 in next-day settlement.

- The $10 sits in a segregated, non-interest-bearing account at the acquirer's sponsor bank. Common sponsors include Wells Fargo, JPMorgan Chase, and BMO Harris.

- On day 180, the $10 from day zero's batch releases to the merchant's operating account, batched into normal settlement.

- Every subsequent batch starts its own 180-day clock. The reserve account grows for the first 6 months and then reaches a flat steady state.

The 180-day clock starts at batch close, not at the original card authorization. Pre-orders or subscription billings booked weeks before fulfillment sit in pending status for the full 180 days plus the booking lag. Recurring billing operators often underestimate the lag.

The math at steady state is the formula that operators rarely run before signing. Steady-state held balance equals reserve percentage multiplied by monthly volume multiplied by the hold period in months. At 10 percent, $500,000 monthly, and a 6-month hold, the steady-state held balance is $300,000. That balance sits in the acquirer's account for the life of the contract.

Several layers of contract language shape how the reserve behaves in practice. The percentage is sometimes called the holdback rate on statements. The release period is occasionally written as 180 days from date of original settlement or 180 days from batch close (the two phrasings can produce a 24 to 48 hour difference per batch). The trigger language defines what causes an increase, and most acquirers include the phrase at acquirer's sole discretion as a backstop.

Card networks do not mandate reserves. Visa and Mastercard publish risk-monitoring thresholds that influence acquirer behavior, but the acquirer chooses the response. Federal Reserve consumer-protection regulations define how long a cardholder can dispute (60 days for most billing errors, up to 540 days for certain claims). Acquirers calibrate the 180-day reserve to that dispute window, with a margin.

"The steady-state reserve at 10 percent and 180 days equals 60 percent of one month of volume. Most operators learn this after signing."

Where it goes wrong for operators

Five patterns surface most often when operators audit reserve performance.

First, the clock resets every batch. New merchants assume 180 days means month seven brings the full balance back. It does not. Each daily batch carries its own release date. At steady state, a new batch enters the reserve account every day and a 180-day-old batch releases. The held balance never shrinks unless monthly volume drops. Operators read 180 days and budget for a one-time, six-month working capital hit. The hit is permanent for the life of the contract.

Second, reserve increases get triggered by chargeback ratio movements. Standard master service agreements include a clause permitting the acquirer to raise the percentage if the merchant's chargeback ratio crosses a threshold. The threshold is rarely defined in the contract itself. Visa's published Dispute Monitoring Program threshold is 0.9 percent, but acquirers typically act at 0.5 to 0.75 percent. On a 5 percent reserve, one bad month can push the rate to 15 percent. At $1 million monthly volume, that adds $200,000 to the held balance within 60 days.

A reserve increase clause written as "at acquirer's sole discretion" has no ceiling. Operators have seen reserves jump from 5 percent to 25 percent in a single month after a chargeback ratio breach, with no contractual recourse and no notice period.

Third, no interest is paid. Reserve funds sit in non-interest-bearing accounts at the sponsor bank. With the federal funds rate above 4 percent through 2026, the foregone yield on $300,000 of trapped capital exceeds $13,500 per year. The acquirer earns float income on every dollar of reserve. Nilson Report tracks aggregate card industry chargeback and loss data that acquirers use to set the baseline reserve rates that produce that float income.

Fourth, the termination tail reserve. When a merchant terminates the contract, the reserve does not release immediately. Standard clauses hold the balance for the original 180-day period plus an additional 30 to 90 days of dispute window. Merchants who switch processors expect to receive the reserve in week one. They receive it 9 to 12 months later, in two or three tranches.

Fifth, the reserve does not transfer. Switching acquirers does not move the reserve to the new processor. The old acquirer holds the tail. The new acquirer typically requires its own reserve from day one. For roughly 6 months, the merchant funds two reserves concurrently. Operators who model their switching cost on processing fees alone miss the working capital double-up, which often equals one full month of revenue.

Each pattern is contractual, not regulatory. The master service agreement is the only document that controls them. Reading it before signing is the cheapest negotiation lever a merchant has.

Worked example with real numbers

Operator profile. Vertical: direct-to-consumer subscription box with recurring billing. Monthly card volume: $800,000. Average ticket: $89. Current contract: 8 percent rolling reserve, 180-day release, no stepdown. Cost of capital (hurdle rate): 12 percent annual.

The math.

Monthly reserve contribution equals 8 percent of $800,000, or $64,000 per month.

At steady state (month seven onward), the reserve account holds 6 months of contributions. That equals $64,000 multiplied by 6, or $384,000 continuously trapped.

Annual carrying cost at the 12 percent hurdle equals $384,000 multiplied by 12 percent, or $46,080 per year. That is the operator's true cost of the reserve, separate from the processing fees on the statement.

Foregone interest, compared to a money-market account at 4.5 percent, equals $384,000 multiplied by 4.5 percent, or $17,280 per year. The acquirer collects that yield and the operator does not.

Total annual reserve cost equals $46,080 plus $17,280, or $63,360. Over a 36-month contract, the cumulative cost is roughly $190,000 of trapped value, before a single chargeback hits.

The same merchant renegotiated at month 12 after a clean dispute year (0.3 percent ratio). The acquirer stepped the reserve down from 8 percent to 4 percent. Steady-state balance fell from $384,000 to $192,000. Annual carrying cost dropped to $23,040 plus $8,640 of foregone yield, a total of $31,680. The renegotiation freed $192,000 of working capital and saved $31,680 per year. The conversation took two phone calls and a competing quote from a second acquirer.

These numbers scale linearly. A $200K monthly merchant at the same 8 percent reserve sees a steady-state balance of $96,000 and an annual cost around $15,840. A $2 million monthly merchant sees $960,000 trapped and an annual cost above $158,000. The percentage matters; the dollar exposure scales with volume.

If the operator switches to a processor that waives the reserve entirely (typically only achievable above $500K monthly volume with 18 months of clean processing and a dispute ratio under 0.4 percent), the released $384,000 funds inventory, marketing, or debt paydown. The capital was always the operator's. The contract just borrowed it.

Operator playbook

Eight actions to take this week.

- Pull your last 12 months of statements and find the line item labeled reserve, holdback, merchant reserve, or risk reserve. Calculate your current held balance and confirm it matches the percentage in the contract.

- Calculate the steady-state cost. Multiply held balance by your cost of capital and add foregone money-market yield at current Treasury rates. That dollar figure is the true cost of the reserve to your business, separate from processing fees on the statement.

- Pull your master service agreement and find the reserve clause. Look for percentage, release period, increase triggers, termination tail, and whether the acquirer pays interest. Any term written as "at sole discretion" is a negotiation lever at renewal.

- Request a written reserve schedule from your account manager. The schedule should show each batch's contribution date and release date. If they cannot produce it within 10 business days, escalate to risk operations and put the request in email so you have a paper trail.

- Ask three questions in writing. What chargeback ratio triggers a reserve increase? Will you put a stepdown schedule in writing tied to clean processing months? What is the tail reserve period after termination? Save the email responses for the renewal conversation.

- At renewal, negotiate a stepdown. A reasonable structure: starting reserve at boarding, 50 percent reduction at month 12 contingent on dispute ratio under 0.5 percent, further 50 percent reduction at month 24. Acquirers regularly accept this on accounts above $250,000 monthly volume.

- Shop the account at month 12. Get three competing quotes from acquirers in your vertical. The quote that offers the lowest reserve (or no reserve) becomes leverage. A competing acquirer will often waive the reserve to win the account, and the incumbent will match to keep it.

- Track chargeback ratio weekly. The single best protection against reserve increases is staying under 0.5 percent disputed transactions. Card brand thresholds are 0.9 and 1.5 percent for Visa and Mastercard, but acquirers act at half those numbers. Monitor the ratio in your processor portal and respond to disputes within 48 hours to keep representment rates high.

The reserve is the most expensive line item that never appears as a fee. Treating it as working capital, not a fee, changes the negotiation.